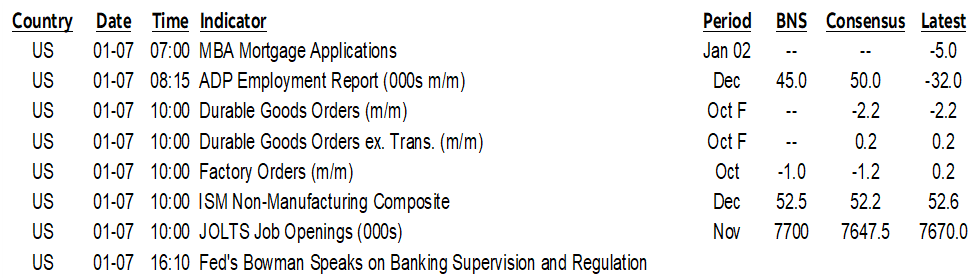

ON DECK FOR WEDNESDAY, JANUARY 7TH

KEY POINTS:

- Classic mild risk-off sentiment awaits US data

- US ADP, ISM-services, JOLTS, factory orders on tap

- Soft Eurozone core CPI drew little attention

- Aussie surprises lower

- Why the US seized 30–50 million barrels of Venezuelan oil

- Venezuela’s uneconomical oil development

- Costing Greenland

Equities have a slight softening bias as bond prices richen. We used to think of that as a classic risk-off play. Oil prices are volatile but a touch lower and so is gold. The dollar is little changed against most crosses unless we’re counting slight weakness by a few EMs.

Light overnight developments offered up a handful of releases that got little attention. Several US data releases are on tap but they’re time wasters before payrolls. Comments follow on Venezuelan oil and how to value Greenland.

WHY THE US IS SEIZING VENEZUELAN OIL

Oil markets should be careful with interpretations of Trump’s social media post last evening that Venezuela will send 30–50 million barrels of oil to the US (here). He said the oil “will be sold at its market price, and that money will be controlled by me…to benefit the people of Venezuela and the United States.”

Pieces like this one from the FT got it right for subscribers with access. An unintended consequence to the US oil blockade against Venezuela is that oil inventories are bulging in Venezuela and they’re running out of storage space. As that becomes more binding, production will have to shut down and Venezuela’s oil industry would seize up. Revenues would collapse, turmoil would ensue. Lifting 30–50 million barrels from Venezuelan storage is a temporary measure, assuming Venezuela fully complies. It maintains the optics of the blockade but pokes a large hole in it out of necessity. The issues around seizing another country’s oil riches to the benefit of the US and exactly what purpose the President will put the estimated US$3B of revenues from the sale are important but secondary to avoiding the full-on implosion of Venezuelan production and a severe crisis stemming from the blockade.

VENEZUELA’S OIL PRODUCTION IS UNECONOMICAL TO RUN

One of the best pieces on Venezuela that I’ve read in the past day or so is from our delightfully skeptical friends at The Economist (subscribers here). It’s nothing new to folks well-versed in the country’s oil sector and global breakeven comparisons but offers important balance to manna-from-heaven narratives I’ve seen. Scroll ahead to the part about breakevens where it flags “the breakeven price for the main Venezuelan projects exceeds US$80, well above the US$50 or so a barrel fetches in the market.” High-cost heavy crude sold with further costly development of the industry’s capacity at high breakevens and sold at a loss in a global market that is already oversupplied makes no sense before even getting into shareholder appetite for probably hundreds of billions of investments that would be required over many years ahead.

GREENLAND—NAME YOUR PRICE

So, assuming you pay for it rather than invading it which is a whole other kettle of fish, how exactly do you value Greenland? It’s an island that is essentially a giant snowcone with no infrastructure to reach scattered reserves of rare earths and energy that would be very costly to extract. If the world continues to warm and ice keeps melting, then looking past the associated downsides like what happens to coastal cities could provide greater access to cheaper shipping lanes through the Arctic. Then there are the supposed advantages to US national security by thwarting creeping influence by China and Russia.

Easy-peasy. We’ll get our M&A teams right on it. I’m sure there’s an Excel spreadsheet that has the answer.

Some attempts at valuing Greenland have been made, like this one. They take a variety of approaches and it’s a worthwhile effort, but in the end, it’s a totally arbitrary exercise that lands anywhere between US$200B and nearly US$3T. And it could be more. Denmark may be sitting pretty on this one, denying any interest which is often the first response by merger targets, while having not sought any bids and letting them come to it in a potential bidding war with China’s deep pockets which would sharply raise tensions with the US. Rationality is often tossed out the window in normal M&As, let alone under these circumstances and with these actors.

OVERNIGHT RELEASES

And here is the ho-hum part of the morning note. There were a few light releases overnight:

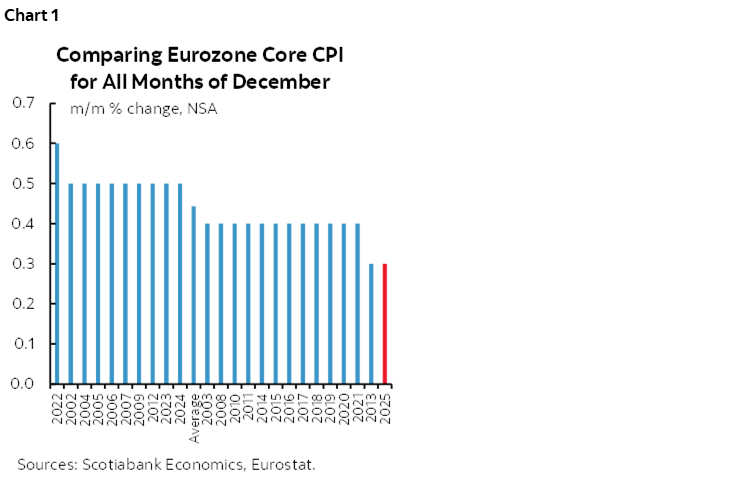

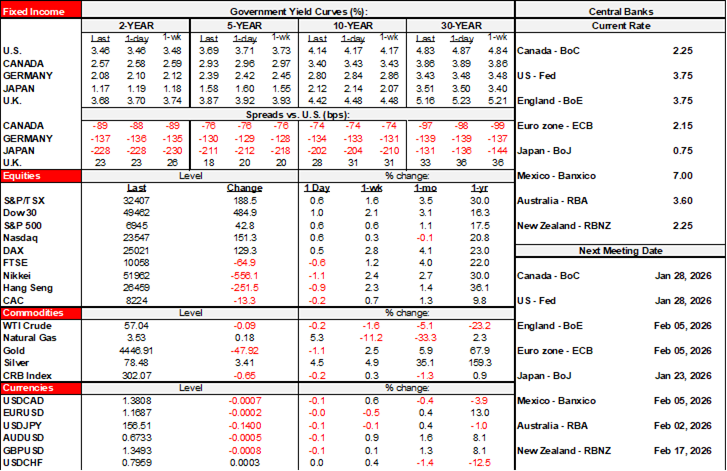

- Eurozone core CPI slipped to 2.3% y/y in December, down a tick from the prior month but still range bound with 2.3–2.4% readings since May. The Euro ignored it. EGBs were rallying before the release and ignored it. Monthly seasonally unadjusted core CPI was the weakest on record comparing like months of December (chart 1).

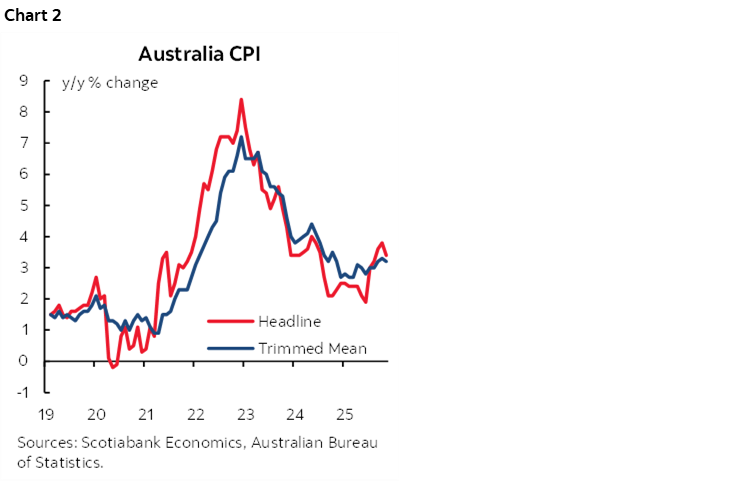

- Australian CPI landed softer than expected at 3.4% y/y (3.8% prior, 3.6% consensus). Trimmed mean core CPI edged a tick lower to 3.2%, in line with expectations. The A$ shook it off. Australia’s 2-year yield rallied by a couple of points. Chart 2.

- German retail sales fell -0.6% m/m in November against expectations for a small gain, but that was because the prior month’s dip was revised up six-tenths to a 0.3% gain.

US DATA TEASERS

Several US releases will pass the time as we all wait Friday’s nonfarm payrolls.

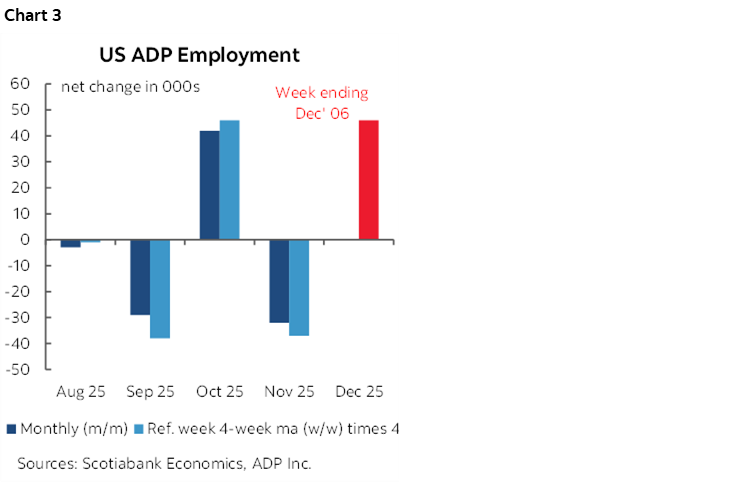

- ADP (8:15amET): A gain of around 45k is expected for December. This would be consistent with the four-week moving average of the weekly gauge (chart 3) but with revision risk and risk stemming from the fact they skipped the reference week’s release so as not to scoop the purpose of their monthly gauge.

- ISM-services (10amET): Modest growth with a reading still around 52 and hence slightly in above-50 expansion mode is expected. The prices gauge has continued to rise at a rapid pace and serves as a leading indicator of inflationary pressures.

- JOLTS (10amET): If the broad correlations between JOLTS and Indeed job postings hold then we should get a vacancies reading around 7.7 million that would be little changed from the prior month.

- Factory orders (10amET): October’s shutdown-lagged reading is expected to drop by less than the 2.2% decline in durable goods orders as nondurable orders post a gain.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.