ON DECK FOR TUESDAY, JANUARY 6TH

KEY POINTS:

- Markets are treading water until Friday’s payrolls

- Soft Eurozone inflation drives mild EGB outperformance

- Q4 auto sales rise in Canada, fall in the US

- Miller escalates brash threats against Greenland

- It’s high time for Polymarket’s wild west to invite regulatory action

- A coming Canadian by-election will change nothing

Barring significant off-calendar developments, calendar-based developments should put even the most unexcitable reader to sleep today.

Markets are catching their breath between invasions—including Venezuela over the weekend, and Stephen Miller’s brash (to be polite…), escalating threats against Greenland (here, or on Bloomberg type NSN T8FPQCTVI5MO). Ultimately the key is what American voters think of American foreign policy on November 7th in addition to domestic policies and whether Mr. Trump respects the results.

In the meantime, markets await Friday’s nonfarm payrolls as the week’s marquee development. Small gyrations in European bonds are being motivated by small surprises in Eurozone and UK inflation readings. Equities are highly mixed with flat to slight downside across N.A. futures. Light data late yesterday showcased consumer strength in the US and Canada.

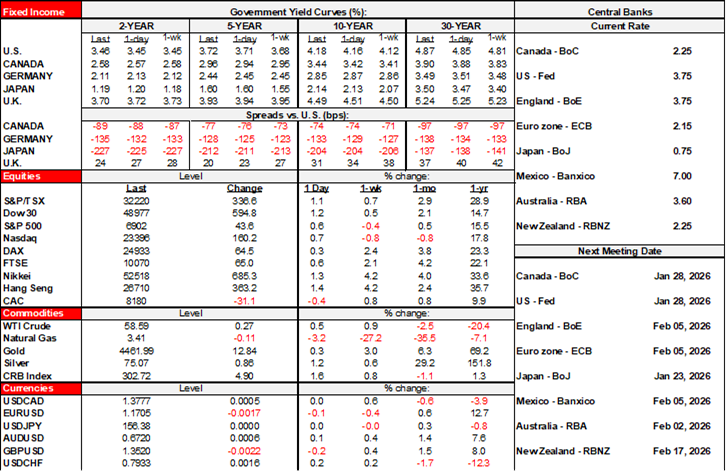

EUROPEAN INFLATION READINGS SPARK SMALL MOVEMENTS IN BONDS

Inflation reports are motivating very slight outperformance by EGBs. After Spain’s CPI reading for December landed on the screws last week with a slight uptick in core, Germany and France did not seem to follow suit overnight. It doesn’t much matter, however, as the ECB is very clear about being in a prolonged holding pattern.

- France’s CPI was weaker than expected at +0.1% m/m NSA as the year-over-year rate dipped a tenth to 0.7%.

- German states revealed inflation figures that tracked well below consensus expectations for the national print that arrives at 8amET. The individual states reported readings between 0% m/m and 0.2% while consensus expected the national reading to be up by 0.3% m/m (0.4% on an EU-harmonized basis).

- UK food inflation climbed in December according to the British Retail Consortium. They were up by 3.3% y/y for the first acceleration since August. The group’s estimate of non-food prices was weak enough to hold back total shop price inflation to 0.7% y/y.

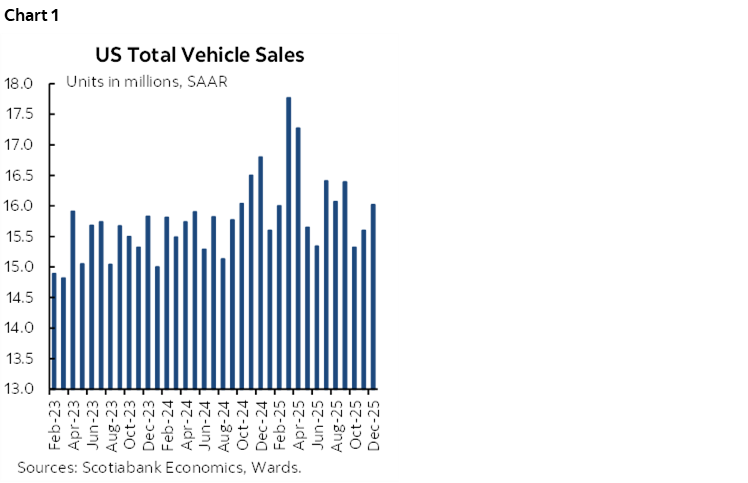

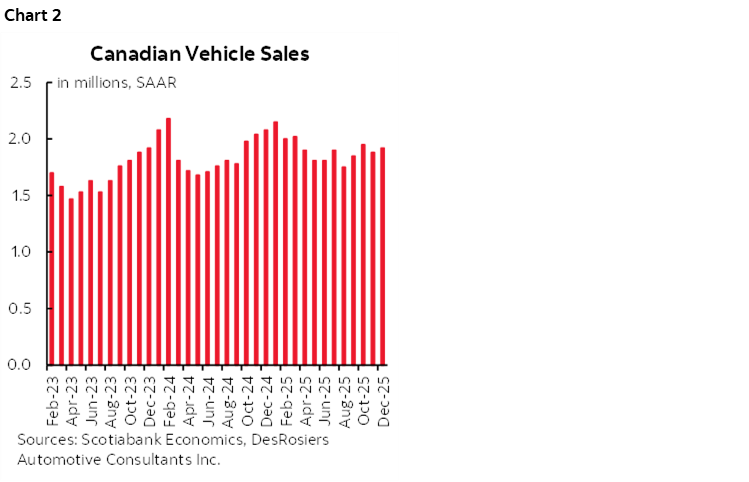

Q4 AUTO SALES RISE IN CANADA, FALL IN THE US

Auto sales in the US and Canada went in separate directions in Q4.

US vehicle sales slightly surpassed expectations but they suggest a drag on Q4 consumer spending on big-ticket durables relative to Q3. They will add to estimates for December’s retail sales figures due out next week and suggest that the expiration of EV credits in September has been shaken off (chart 1). Sales landed at 16.02 million at a seasonally adjusted and annualized rate versus what had been industry guidance for 15.8, for a gain of 2.7% m/m SA over the prior month’s 15.6 reading. Q4 over Q3 was down by 14.8% q/q SAAR which more than reverses the 5% q/q SAAR gain in Q3.

Canadian vehicle sales were up by close to 2% m/m SA in December (here). Q4/Q3 looks like about a 16% q/q SAAR gain which fits the picture of soaring job growth. Auto sales are holding up rather well (chart 2). The figures suggest resilient Canadian consumer spending on big-ticket items like autos.

OTHER STUFF

A Canadian by-election is coming after Liberal MP Chrystia Freeland announced she would resign her University-Rosedale seat “in the coming weeks” (here). Her riding is traditionally a rather centre-left stomping ground which likely means little threat to the Carney administration’s status as being one-seat shy of a majority versus a status quo outcome.

Richmond Fed President Barkin (nonvoting 2026) speaks on the outlook (8amET).

There is a lot of coverage of suspicious trading activity in the lead up to the US invasion of Venezuela including possible tipping (here) and trading (here) on a totally unregulated platform with anonymous accounts that settles in USDC, a stablecoin. Proving who did it is next to impossible given reports of multiple leaks to energy companies, media, and across members of the Trump administration. It’s stunning to me that such a platform’s tactics are apparently allowed to operate beyond the reach of regulators and the SEC. For the sake of market confidence it’s high time regulators clamped down on these platforms.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.