ON DECK FOR MONDAY, JANUARY 5TH

KEY POINTS:

- Oil shakes off Venezuela’s near-term effects, for now

- Venezuela’s implications: Shoot first, think later…

- …as oil pundits get ahead of themselves…

- ...while many broader implications could also include US Treasuries

- US ISM-manufacturing: the manufacturing sector is reeling

- US vehicle sales expected to be little changed

- Canadian vehicle sales may be updated today/tomorrow

Welcome to the first full trading week of the new year. Front and center are evaluating the consequences and implications of America’s assault on Venezuela (see below). There are two key market/economy questions everyone should be asking themselves about the illegal US action in Venezuela and they concern implications for oil production elsewhere across the Americas and possible implications for US Treasury revenues on a signal toward siphoning off Venezuela’s revenues.

Modest data risk focuses upon US ISM-manufacturing and N.A. vehicle sales. Canada might release vehicle sales today or tomorrow. For now, global equity and sovereign bond prices are gaining a touch, the dollar is slightly firmer except against the yen after more hawkish talk from the BoJ’s Ueda, and oil is flat while gold is up by under a hundred bucks.

VENEZUELA’S IMPLICATIONS...

Before turning to the implications of America’s illegal invasion of Venezuela and its forced removal of a foreign head of state, let’s be clear on one thing—there are no crocodile tears to be shed for Nicolás Maduro. He was an illegitimate leader and a brutal dictator who pursued actions that enriched himself and his cronies while impoverishing the nation. Good riddance. And no, Venezuela, you can demand as much, but you won’t get him back.

And yet it’s not quite so simple as leaving it at that. There is a high sense of uncertainty along an unknown path going forward. Here are some tentative views.

...STARTING WITH THE OIL PUNDITS GETTING AHEAD OF THEMSELVES...

A clear intent is to control Venezuela's over 300 billion barrels of oil reserves that amounts to about 17% of the world’s total reserves. Trump himself was very transparent about this motive in his Saturday press conference and I don’t buy side motives as argued shortly. It’s a hostile takeover in the global energy sector, the only difference being that guns were used instead of shareholder tactics. The US needs a lot of oil as it turns away from clean energy sources and ramps up electricity generation including to feed highly subsidized data centers albeit with manufacturing in accelerated decline during Trump 2.0. The US administration is acting in the interests of US Big Oil in Venezuela after the country nationalized the sector and US companies were chased out years ago. The US wants a piece of the revenues and wants lower oil prices.

But the oil pundits may be getting way ahead of themselves with a lot of the comments I’ve seen in reaction to the developments. Greater caution is required before leaping to their conclusions that this will unleash a torrent of new supply on world markets with effects that allegedly include snowing under Canada’s oil industry.

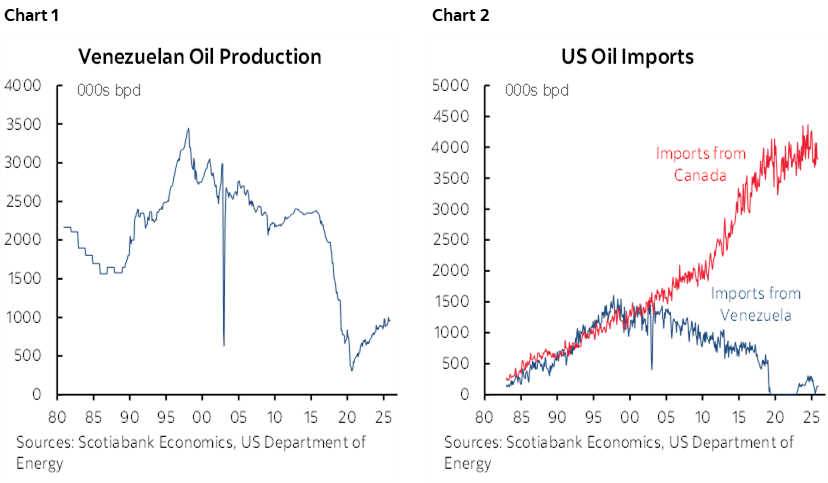

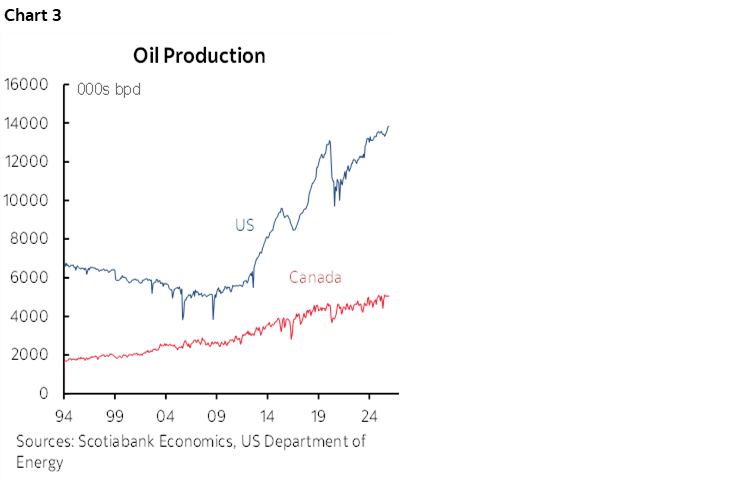

First the facts. Venezuela’s oil production went into freefall through total mismanagement of the resource (chart 1). The country was producing about 3½ million barrels per day at its peak in 1998 and presently produces about 1 million bpd. Most of that production goes to China which has driven a mild recovery in Venezuelan oil production since the pandemic. As chart 2 shows, Venezuela’s oil exports to the US went into long-term decline from a peak of about 1.6 million bpd in 1997 to next to nothing today.

There may be long-term implications of this action for oil produced within the US and for US oil imports from Canada and Mexico and other countries. Let’s face it, one of the best things that happened to North America’s energy sector at least for a short time was the collapse of Venezuela’s oil exports to the US even though US assets in Venezuela suffered. Some of Venezuela’s “friends” and defenders across Latin America may have acted as such toward the country because their own energy sectors profited from Venezuela’s dysfunction. These “friends” never really wanted Venezuela to succeed.

US oil imports from Venezuela began drying up after 2000. US oil and Canadian exports picked up the slack and met incremental US demand for energy beyond merely filling in the space vacated by Venezuelan exports. US domestic energy investment and jobs benefited. So did Canada’s. So did others. Up until the year 2000, Canada and Venezuela exported equal amounts of oil to the US (chart 2 again). Since then, Venezuela went into long-term decline while Canada’s exports surged. If—and it’s a big ‘if’ with a lot of uncertainty over time—US access to Venezuela’s massive oil reserves should be restored and drive major investments, then it could be a bad development for the US and Canadian oil industries (and others). Venezuela may eventually achieve much greater heights for oil production than its past peak. The threat could be especially challenging to Canada given that its heavy oil is a more direct competitor to Venezuelan heavy oil that often serves different purposes than light sweet crude. One test of this will be to monitor WTI-WCS spreads over time; the heavy oil discount that always exists because of higher processing costs may widen.

Or so goes the thesis everyone immediately embraced on Saturday morning when we woke up and learned of the US invasion. Reality could be very different.

For one thing, invest in Venezuela’s energy sector? It’s energy and broader infrastructure lay in shambles. Political uncertainty is off the charts. American hubris thinks it can restore order and run the country with a compliant local administration. Hello Libya. How’s it going, Afghanistan. What are you up to these days, Iraq. Vietnam was a smashing success, wasn’t it. America will never learn that sheer military might is not enough to achieve long-term success.

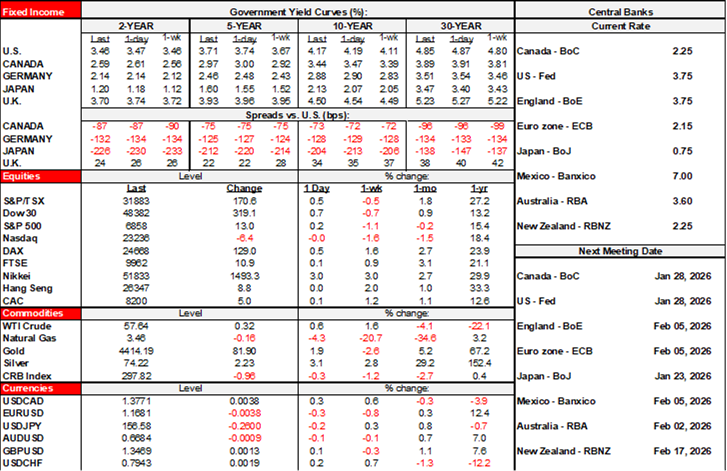

Second, the world has profoundly changed since Venezuelan oil production went into freefall starting about a quarter-century ago. Developments since then could well mean that Venezuela’s production isn’t needed as much as it once was, if at all. A key development has been that after declining from about 1985 to 2008, US oil production began massively expanding. It went from just over 5 million bpd to about 14 million today for a near tripling (chart 3). Canadian oil production also surged from about 2½ million bpd around the time of the GFC to about double that today as also shown on the chart. US oil crowded out import growth from everyone else, including Mexico’s soft long-term trend, while limiting Canada’s penetration of US demand.

Third, the world oil market is already in surplus. The WTI oil price has dropped by almost $20/barrel since mid-2024. What do you think unleashing 3 billion barrels of reserves in Venezuela would do to world oil prices relative to production breakevens? US Big Oil isn’t that dumb. Trump wants lower oil prices which fits into his demand for lower inflation and lower interest rates, although lower oil prices could unleash warmer core inflation by raising purchasing power of consumers. He should be careful what he asks for in that collapsing oil prices through over development could collapse his country’s own oil sector with broad ramifications for jobs and related industries like the investors who finance the sector. Shoot first, think later, if at all… Expect oil industry c-suites to be much more measured than Trump.

Fourth, US and Canadian oil infrastructure already has a strong hold on the US market.

Nevertheless, the prudent thing for Canada to do would be to act with a greater sense of urgency in terms of building capacity to export oil to Asia (arguably ditto for Mexico). America’s hostile takeover of Venezuelan oil may either extract larger concessions from its main buyer (China) and/or divert Venezuela’s exports to the US and away from Asia (namely China) where it presently goes, thereby crowding out opportunity for Canadian oil in the US and opening up opportunity to export to Asia. American oil is no doubt thinking the same way and in some respects its energy capacity toward Asia is well ahead of Canada’s (eg. LNG). Further, the US will clearly favour its own companies investing in Venezuela at the expense of energy companies from Canada and elsewhere.

...WHILE THERE COULD BE IMPLICATIONS FOR US DEFICITS...

Could there be implications for US government finances? We don't know the next steps and how developments will unfold over time. Trump claims that the US will run the country on an interim basis until “a safe, proper and judicious” handover can occur and that “it won’t cost us anything because a lot of money is coming out of the ground.” That implies the US will divert Venezuela’s oil revenues for its own purposes. The Trump administration has demonstrated a desire to enter extractive relationships with other countries and investors that secure profits for the US administration. Could Venezuela be an extension of this practice? What limits may be placed upon this diversion of revenues and for how long? Will the US divert oil revenues to its own Treasury beyond merely paying for its military incursion?

If so, then we’ve fully wound the clock back to the days of European mercantilism which would be consistent with the whole tariffs framework, only this time we’re not talking about European powers pillaging foreign gold and precious treasures as oil is the new gold to the US administration’s outdated romanticizing of the role played by oil in a fundamentally changed American economy. US policies toward energy are changing, but it’s still the case that the US economy needs less and less oil to drive a dollar of GDP today than it did decades ago and I can’t see that fundamentally changing.

...AS UNCERTAINTY WILL REMAIN VERY HIGH IN VENEZUELA...

How this will be executed is highly uncertain and it is stunning to see the US “run” an independent sovereign nation. What is America’s exit strategy, especially if troops on the ground are the next possible step as Trump suggests, and if there is one? Could this lead to regime change including elections? Don’t hold your breath. Trump has dismissed opposition leader Machado as lacking the respect to lead Venezuela and ruled her out as an option. He has said that Venezuela’s VP—a strident socialist and Maduro ally—is expected to work with the US administration, though at least publicly the VP has sent mixed signals. Will the US actions spur the complete breakdown of any order within Venezuela? Will the same regime remain intact with the VP or another leader? Will its behaviour change? Could either the same regime or a new one pursue more of a policy of appeasement and cooperation with the US that allows greater US investment and control? Or does the worst still lie ahead for Venezuelans?

…AS US MOTIVES REACH BEYOND OIL...

As for side motives beyond oil, it’s a well-worn playbook of US administrations that are down in the polls heading into midterm and Presidential elections to divert attention through actions in foreign theaters. We can’t ignore the strong possibility of this motive in that it may all merely be performative in nature, done for Hollywood’s cameras, and done for Trump’s MAGA base some of whom like to see displays of foreign aggression while others recoil in horror at the thought of another forever war or multiple such wars. Further, if this were about human rights and freedoms, then there are plenty of other dictatorships elsewhere that could have motivated US involvement but that have nothing the US wants so can the virtue-signalling bravado.

Further, the narcoterrorism case is disputed by many observers. The US built a case for this action over several months. Many dispute the alleged connection between Maduro and the so-called ‘Cartel of the Suns’ in terms of alleged narco-terrorism motives for the US invasion. Who knows the truth, but frankly, while I think there is something there, you can still count me as deeply skeptical after watching the Trump administration blatantly lie about Canada’s falsely alleged massive fentanyl exports to the US. Panama’s Noriega was a very different case—see comparisons like here—and the US has a history of fabricating excuses for invasions as folks who recall ‘weapons of mass destruction’ can attest.

...AND COULD INFLAME BROADER GEOPOLITICAL TENSIONS...

Is geopolitical risk on the cusp of intensifying? Who is next? Iran? Quite possibly, given US alignment with Israel and broader US policy toward the Middle East. North Korea? That’s unlikely, as the US needs nothing from North Korea and it’s a nuclear power. An unevenly applied foreign policy is at stake. Invading Venezuela conceivably clears the way for China and Russia to legitimize removal of undesired regimes. Think Taiwan, for one, as China points to US hypocrisy should it oppose. Taiwan is putting on a brave face with its interpretation of the consequences this morning but it should be more concerned. China needs Venezuelan oil and has invested billions in the country and could conceivably escalate tensions in Taiwan to get the US to back off Venezuela. So far, Trump has said Venezuela’s exports will remain intact, which he likely said to avoid a price spike this morning. There may even be less of a likelihood of peace in Ukraine if that was ever achievable in the first place (probably not).

And then there are Trump’s repeated threats against Colombia and Greenland over the weekend. Threats against Greenland are likely mere hubris as the EU and allies would likely rise to the defence of Denmark’s interests, but the fact we even have to say this is a sign of how unreliable the US has become toward its allies to the benefit of what were once its foes.

...WITH UNCERTAIN REACTIONS BY OTHER WORLD POWERS...

The Trump administration’s goal of dominance across the Americas and western hemisphere is likely exaggerated to begin with, but how foreign powers like China and Russia respond in the region could be key given their direct interests in South America in a geopolitical sense and in terms of resources. As one example, it’s not 1962 all over again, but I’m pretty sure Russia would have something to say about any US actions against Cuba as Trump has intimated.

Other countries—namely ones like China, Russia etc—could impose sanctions upon American individuals and companies by applying the same principles of opposition to an illegal invasion that were applied by the west.

...WHILE RISKING A MIGRANT CRISIS...

There may be a migrant and humanitarian crisis should a complete breakdown of order ensue. Strong arm dictators keep their victims in place. Venezuela borders on Colombia, Brazil, and Guyana. Colombia is already amassing troops on its border and it has an awful lot more experience in jungle warfare than the US. The overall effects could be significantly destabilizing across the region especially if the US commits to a troop presence.

...RAISING RISKS AND ATTRACTIVENESS OF SUPPLYING DRUGS TO THE US…

US actions against Venezuela may dent the drug trade, but are very unlikely to kill it. With higher risks go higher prices and hence higher rewards to meeting US demand for drugs. The industry is adept at moving around and adapting. The US needs complementary policies aimed at addressing its drug problem including fentanyl that Venezuela wasn’t much involved in supplying if at all. Extreme wealth and income inequality and associated social problems in America are among the drivers of demand for drugs and some of the most fatal ones—like fentanyl—can be made anywhere.

...AND POSING ANOTHER CHALLENGE TO AMERICAN DEMOCRACY

This is another step to solidify power in the executive branch and neuter Congress which has traditionally been involved in approving foreign military excursions. Congress wasn’t involved or notified whatsoever. Disharmony will only intensify in Washington.

LIGHT US DATA ON TAP

The US will update December readings for ISM-manufacturing (10amET) and vehicle sales (e.o.d.). ISM-manufacturing has been in sub-50 contraction territory since March. New orders have fallen in nine of eleven months this year. Prices paid are still soaring. With the exception of a handful of months, US manufacturing employment has been falling since 2023. This is not bringing home manufacturing.

Vehicle sales are expected to hold little changed at around 15¾ million at a seasonally adjusted and annualized rate.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.