ON DECK FOR FRIDAY, JANUARY 30TH

KEY POINTS:

- Markets unsure about the Fed’s coming policy mixture

- Trump picks Warsh as Fed Chair, Senate confirmation may be rocky

- Warsh said a lot to get the job. Now let’s see what he’s really about

- Warsh is likely to drive curve steepening on policy rate and balance sheet views

- Progress toward averting a US government shutdown

- Trump’s latest tariff threat against Canada is empty, avoidable and rather rich

- Canada’s economy likely grew in November, December uncertain

- Eurozone posts faster than expected growth, softer inflation

- Mexico’s economy beat expectations

- BanRep’s potential whiplash

- Fed-speak won’t be just about Warsh

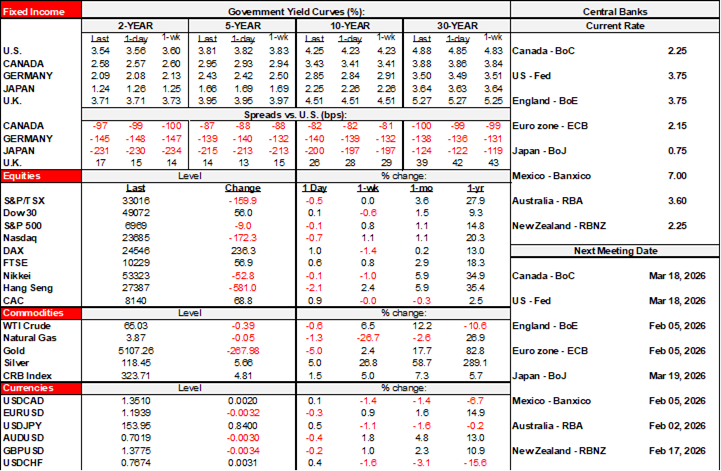

If Kevin Warsh is being chosen to lead the Fed because Trump views him as a dove, then markets have something to say about it this morning. Markets are sorting through his views that are a mixture of dovish and hawkish in favour of curve steepening (see below). The USD is broadly stronger, the Treasury yield curve is steeper and driven by a mild longer-end sell-off and a mild front-end rally, US equity futures are mildly lower and gold is getting smoked with a 5% drop back down to US$5,100 with silver down 12%.

Other developments are barely worth acknowledging in terms of market influences. There appears to have been progress toward a funding deal to keep the US government open; I suppose we should cheer that something so blindingly unwise as another shutdown should be averted.

Apple earnings were impressive in yesterday’s after-market but superseded by Warsh’s impact. Key in the earnings season is the ongoing heavy commitment to AI cap-ex (chart 1).

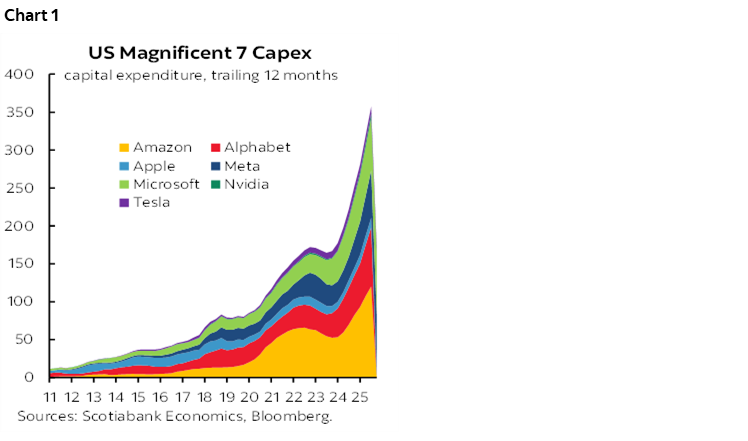

German and Spanish inflation landed softly in January readings. Eurozone GDP growth was a tick above expectations at 0.3% q/q SA with each of Germany, Italy and Spain beating consensus while France matched. Chart 2.

Mexico’s economy outperformed with GDP up 0.8% q/q SA in Q4 (0.6% consensus). South Korean factories are soaring with output up 1.7% m/m in December, more than tripling expectations. Tokyo CPI was softer than expected (1.5% y/y, 1.7% consensus) with core ex-food at 2.0% (2.2% consensus) which contributed to a rally in shorter-dated JGBs alongside weak retail sales and industrial output.

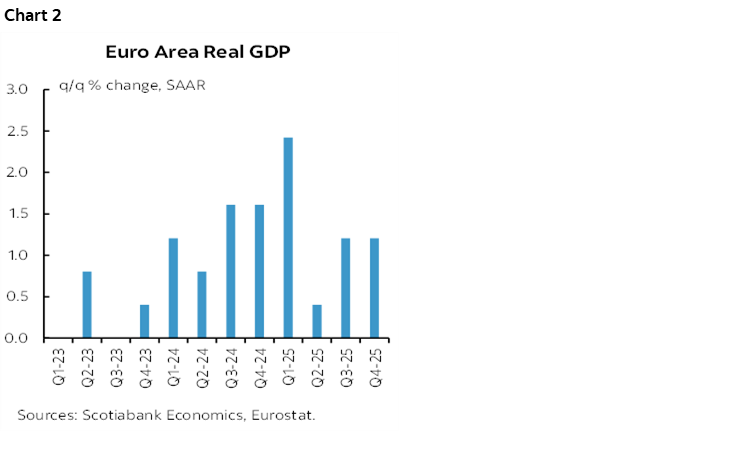

Today’s calendar brings out Canadian GDP for November and the flash estimate for December (8:30amET) amid current tracking of a soft Q4 for GDP growth (chart 3). US producer prices for December may garner little attention (8:30amET), and BanRep is expected to hike with consensus sitting at +50bps (1pmET). There will be other Fed-speak including Bostic (8:30amET), Musalem (1:30pmET), Miran (3pmET) and Bowman (5pmET).

Also watch for progress on averting a US partial government shutdown.

WARSH AS CHAIR—MORE DOVISH ON RATES & REGS, WATCH OUT ON THE BALANCE SHEET

Trump confirmed the choice in this social media post this morning. The signs were already lining up on multiple counts last night. He met with Trump at the White House yesterday. Trump said yesterday that “A lot of people think that this is somebody that could’ve been there a few years ago.” Recall Warsh lost to Powell in 2017 and Trump has since publicly lamented not choosing Warsh. Reports indicated that Trump’s advisers were informed of the choice last evening. Polymarket bets instantly pushed to 95% odds that it would be Warsh who gets the job.

Warsh’s confirmation in the Senate is probable, but not totally assured. Senate Majority Leader Thune said last evening “probably not” in response to whether the Senate can approve Warsh without support from Senator Tillis. Tillis has said he won’t approve anyone until Trump stops his probe into Powell’s role in approving renovations.

An added caution is that as powerful as the Chair is, Warsh must command a divided Committee with a disparate array of views across its members. One man cannot sail the ship alone, perhaps especially one man who has been so strikingly critical of the rest of them. Mr. Warsh will need to prove in short order that he can lead a consensus amid high risk of splintering the Fed into even greater factions that may not serve the economy and markets well.

Why are markets reacting this way? One reason may be that they were on the fence in their positioning around alternative candidates and the others may have been perceived to be more dovish.

Another is Warsh’s stance against QE and I’ve long shared the same concern since the GFC. The Fed got addicted to it in serial fashion. There are many other tools in its toolkit to address market dysfunction. Serial QE distorted capital allocation and contributed to fiscal largesse. Serial QE may have artificially inflated valuations with stability considerations. It’s only supposed to be a tool used in truly exigent circumstances that, once settled, should have the Fed getting out of the way.

And so markets may be pricing a combination of more rapid balance sheet run-off and/or lower probability that the Fed will ride to the rescue with QE in future shocks. Good. But do you have the steely nerve to pull it off, Mr. Warsh? To end America’s addiction to support from the Fed’s balance sheet through good times and bad? To court potential stability issues and abrupt corrections in risk appetite if your views are not carefully executed?

A trade-off in managing such risks is that markets should view him as more open to greater easing. He’s not sounding like the hawk of old. His WSJ op-ed last November emphasized AI as “a significant disinflationary force” that should drive the Fed to “discard its forecast of stagflation in the next couple of years.” That sounded like lower rates to prime the economy with the belief other forces will tamp down inflation. He also said the “Fed’s bloated balance sheet….can be reduced significantly” and that “largesse can be redeployed in the form of lower interest rates to support households and small and medium-size businesses.” I’m not clear on his connection here. Further, his tone on financial regs sounds open to deregulation and distancing the US from “global regulatory convergence” through frameworks such as Basel capital rules. Depending on the form of implementation and timing across various tools, this snubbing of global standards could carry profound knock-on implications outside of the US. That may be good for global growth, with commensurately higher risks.

Yet markets will view Warsh with healthy scepticism. Is he a chameleon who sacrifices Fed independence to the interests of the Trump administration? Look at his pivot on tariffs away from longstanding support for free trade. He has heaped praise on Trump as the race to lead the Fed heated up. He pivoted toward more dovish views during the race.

Time will tell. A lot of folks say a lot of things to get the top job and walk away mischievously grinning in disbelief that the

TRUMP THREATENS CANADA’S AEROSPACE SECTOR

Trump’s latest assault on Canada came through this social media post last evening. He threated a 50% tariff on all aircraft sold by Canada into the US and decertifying all aircraft made in Canada. It’s a shot at Bombardier because of alleged Canadian foot dragging on approving Gulfstream jets.

First, this could be another empty threat he backs down from, given the pattern to date.

But to my very limited understanding of this issue, it’s not that Transport Canada Civil Aviation is blocking them, it's that it has its own validation process. Newer Gulf Streams like the G700 and 800 have not yet finished their process. Gulfstream jets do indeed fly in Canada and their jets have not been decertified in Canada.

Then again, don't get me started on how the US subsidizes Boeing on a totally uneven playing field.

These guys track Boeing's detailed subsidies. Direct subsidies total US$15.6B plus loans and bailouts they figure are another US$75B. And most of that is just since 2015, not going way back to Boeing's inception. The entire global aerospace business is replete with heavy government involvement including through subsidies. The Americans do it, so do the Europeans, so do the Brazilians.

As for exposures, total exports of all aircraft and parts from Canada to the world came to C$30.2 billion in 2025 over the first eleven months for which we have trade data. That's 4.3% of total exports from Canada to the world. That’s not nothing, but the macro impact would be limited.

We’ll see how this evolves, but I would think there is an easy path forward to avoid escalation. Canada has a right to independently review its own policies.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.