ON DECK FOR THURSDAY, JANUARY 29TH

KEY POINTS:

- Gold crosses $5,500, oil up 2%+ as Iran risk returns

- BoC: Likes and dislikes

- FOMC: Likes and dislikes

- Light overnight developments

- Apple earnings, light data on tap

Congratulations. You survived. I’m speaking in reference to the week’s main events that were concentrated upon yesterday and including the Fed, the BoC and tech earnings in the after market.

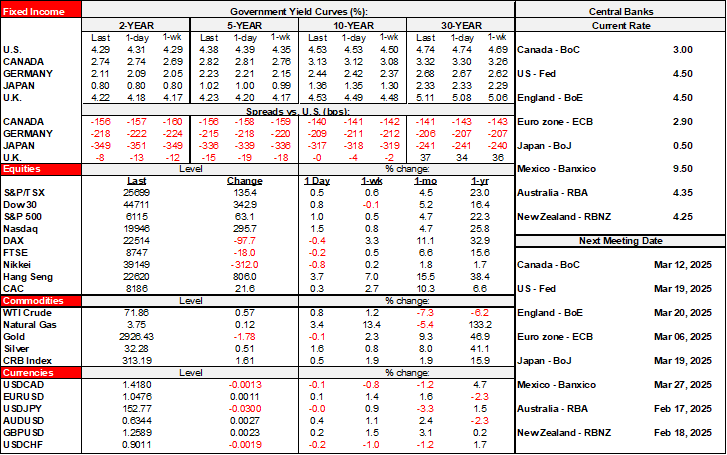

Stocks are keeping it together with US futures flat, TSX futures up a smidge, and European cash markets mostly higher except for Germany. Gold just keeps charging ahead and is crossing US$5,500/oz this morning. Oil futures are up by about 2% as Trump rattles sabers over Iran with social media posts last evening. Sovereign bonds are mostly just treading water. The dollar is little changed.

So on we go. On to the next things on the docket, namely next week’s US payrolls. Onto the slow grind toward trade negotiations. In the more immediate context the risk of another partial government shutdown in the US is creeping too close for comfort given the weekend expiration of funding.

Overnight and early morning developments were light. Markets are taking last evening’s tech earnings in stride. Dow announced 4,500 job cuts this morning to add to 30,000 from UPS and 16,000 from Amazon this month, among smaller layoffs elsewhere. Two central banks held as expected (Riksbank, Brazil). SARB delivers a decision shortly after publication that has consensus divided between a cut and a hold. MSCI’s warning on how Indonesia may be downgraded to frontier market status drove a plunge in local stocks and depreciation of the rupiah with some spillover to neighbouring markets. GDP figures disappointed in Sweden (0.2% q/q, 0.5% consensus) and the Philippines (0.6% q/q, 0.9% consensus with mild negative revision).

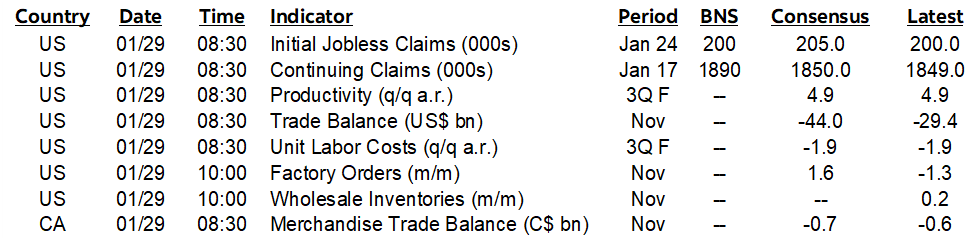

On tap for today are relatively light developments until the after-market when Apple releases earnings (EPS consensus US$2.68). Trade figures will be released by Canada and the US (8:30amET). Canada updates SEPH payrolls for way back in November and they don’t matter anyway (8:30amET). There will also be US Q3 productivity and labour cost revisions but they’re likely to be minor on the heels of minor GDP revisions (8:30amET). US weekly claims (8:30amET) and factor orders in November (10amET) round out the releases.

BOC—WHAT I LIKED, WHAT I DIDN’T

There were likes and dislikes in what the BoC delivered yesterday (recap here).

The big like on what I heard from the BoC is the circumspection toward the future direction and timing of the policy rate path. Sell side doves only heard a dovish bias, but that’s not what Macklem conveyed. Macklem said this in the presser:

“The clear consensus was that it's very difficult to predict either the direction or timing of the next move in our policy interest rate. You need to be able to assign probabilities to the risk to assign probabilities to the rate changes.”

Fair enough, which is why we have the BoC treading water with a neutral stance, balancing risks in a prolonged hold until Fall at which point our analysis and assumptions point to higher risk of moving back up to the upper half of the neutral rate range.

But here’s what still bothers me about the Bank of Canada’s communications yesterday that felt fudged across multiple touch points:

- they upgraded growth everywhere—except Canada. US growth was revised up by almost half a point for 2026, and growth everywhere else from China to the Euro area was also revised up. But not Canada. Excessive domestic pessimism folks with absolutely no translation of higher global growth into Canada? Does your Canada group talk to the international group?

- Macklem repeatedly referenced the unpredictability of President Trump’s trade actions, but is it unpredictable, or as unpredictable as at first? It was at first, but since then it seems to me that he’s become entirely predictable. Trump is in a midterm election-year pattern of repeatedly threatening and repeatedly backing down. Actions—or lack thereof—speak louder than social media posts. I’ll come back to views on CUSMA/USMCA below.

- they went too far in cancelling out the effects of GDP revisions by raising potential GDP in largely offsetting fashion, leaving the output gap unchanged toward the end of 2025. We get more of a lift to actual GDP than potential GDP from the multi-year revisions which should have lowered their estimates of slack. The BoC repeatedly treats potential GDP as a fudge factor to suit its views in the moment. My concern is that Macklem pre-judged the impact of the GDP revisions in December’s press conference and they made the numbers fit that pre-judgement yesterday. Recall that in December, Macklem said “We don’t have a new projection” but that the impact of the revisions “roughly” cancel out through actual and potential GDP. Presto, January’s numbers complied.

- they cherry-picked core measures in chart 7 of their MPR and elsewhere by only emphasizing the recent deceleration in trimmed mean and weighted median CPI. Nowhere did they reference that traditional core CPI (ex-food and energy) has been firmer with a 3-month moving average of 2.3% m/m SAAR and December’s reading of 3.1%. Haven’t they dumped on trimmed mean and weighted median and signalled more use of traditional core? Haven’t they said they look at all measures? But when it suits them in the moment, they cite the most dovish measures and ignore the other?

- there was zero reference to rising breadth of inflationary pressures. You won’t find the word once in the entire MPR.

- there was no mention anywhere—not even in passing during the press conference—of GST rebate changes that will infuse significant cash into the household sector by Spring and that were announced too late to be include in the MPR forecasts.

FOMC—LIKES AND DISLIKES

There were also likes and dislikes about yesterday’s FOMC communications (recap here). I felt the press in the room were in a state of adulation that gave Powell a free pass when he should have been more strongly confronted on his depiction of the labour market.

In terms of likes, there is one big one. I like the careful management of moral hazard. It’s well down the list of any Fed watcher and not central to anyone’s forecasts, but still material. Major further policy easing amid easy financial conditions could embolden other bad policy developments in other areas, like more tariffs, more reckless fiscal policy, etc. In a game of chess, your next move must consider the opponent’s reaction lest the administration’s political pressures declare check mate on you.

But the flaw in that thinking is that it supersedes Fed wisdom above other checks and balances in the system such as the courts, voters, etc. This is why our Fed views have to remain anchored in terms of an understanding of the dual mandate developments. On that count, there were dislikes in what I saw and heard yesterday.

- the biggest one is that I’m not comfortable with Powell’s depiction of the labour market. For one thing, he points to a recently stabilizing unemployment rate. The fact that labour supply and labour demand are cancelling each other out doesn’t address the fact that weakening nonfarm payrolls means weakening income growth (Q4 disposable income growth is tracking very softly with a falling saving rate) and hence downside risk to consumption. Further, the unemployment rate is derived from the household survey and has a massive confidence interval and so it’s silly to place emphasis upon a tenth here or then by way of monthly movement in the UR.

- Further, Powell faded concerns over job numbers by striking out reference to “downside risks to employment rose in recent months.” I strongly disagree with this. Downside risks to employment are accelerating in my view. Headline changes in payrolls are weak but they’re even weaker after accounting for several points emphasized in notes such as the last nonfarm payrolls report here. Powell’s reference to private payrolls being up seemed to bow to Trump while ignoring the many arguments behind the distortions and the key point that taking health care hiring out of the picture points to no breadth and a falling trend in private payrolls.

- there was no mention of the impact of expiring Affordable Care Act subsidies. Some estimates suggest this could cost 25–35k jobs per month on average this year through direct and indirect effects.

- Powell emphasized strong GDP growth as a support to the job market. I think most economists would say that when the job market is wavering, it’s a matter of time for when GDP growth falters. As a case in point, go back to 2007–08. Nonfarm payrolls started to trend lower after 2005 and began falling sharply at the beginning of 2008, yet throughout that period, GDP was whistling by the graveyard posting repeated gains throughout 2005–07 and really only significantly stumbling by late 2008.

- Powell’s hasn’t always adhered to his advice to his successor to “stay out of elected politics, don’t do it.” At times, he has been nuanced such as overemphasizing a grand experiment to push toward the outer bounds of fully inclusive maximum employment in the depths of the pandemic that blinded him to inflation risk. At other times he has definitely locked horns with the administration on topics like tariffs in moderated discussions which I like to see given his leadership position on policy, but don’t overstate your independence from politics.

- it should’ve been a very short presser with questions cut off well before 35 of them!

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.