ON DECK FOR WEDNESDAY, JANUARY 28TH

KEY POINTS:

- Dollar shakes off Trump’s indifference ahead of central banks, Mag7 earnings

- FOMC — A Long Yawn

- BoC — All Talk, No Action

- RBA on track toward becoming the first of the majors to hike…

- …after inflation ended 2025 higher than expected

- Are US layoffs surging again?

- Tech earnings may matter more than central banks

- Brazil’s central bank to hold

It’s the day you’ve all been waiting for this week. The Fed, the Bank of Canada and Brazil’s central bank all deliver decisions and with Mag7 earnings in the after-market.

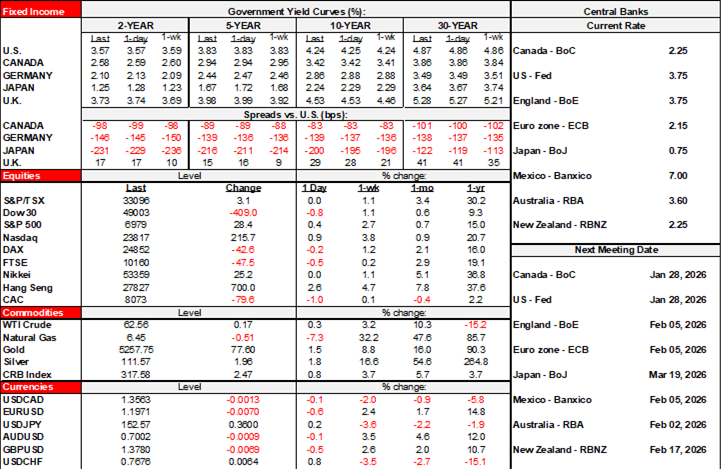

Market positioning could easily change by day’s end, but for now, the broad tone across global markets is highly mixed. US equity futures are up mildly, TSX futures are flat and European exchanges are pushing lower by up to -1¼%. The rates space is dominated by moves Down Under after CPI pushed RBA hike pricing higher. Trump’s indifference toward dollar weakening was soooo yesterday’s trade as the dollar is gaining against several other major crosses this morning; what the President says plays third fiddle to fundamentals and broader sentiment. Gold is up another US$70/oz or so and closing in on US$5,300 with the latest headline motivators including Tether—that stablecoin turning hedge fund—and its actions to bulk up in gold.

Please see my Global Week Ahead—Excuses, Excuses! (here) for full previews of the central bank decisions that I won’t repeat here other than brief highlights.

BANK OF CANADA—ALL TALK, NO ACTION

Did you feel the earthquake last night? That question will likely cause more of a buzz in Ottawa and Canada’s financial capital of Toronto than the Bank of Canada. No policy changes are expected. The numbers and verbal guidance may inform the bias going forward, but we’re not expecting much.

The statement will be here and lands at 9:45amET along with Governor Macklem’s written opening remarks to his press conference (to be here at that time) and the Monetary Policy Report (to be here) that includes full forecast updates. He and SDG Rogers will deliver a press conference at 10:30amET for around 45 minutes plus or minus; I recommend running multiple feeds (such as CPAC with translations) since the various outlets frequently have a/v and translation (if needed) issues.

Markets are priced for absolutely nothing to be done until at least the end of the year. The only pricing that matters is near-term in my opinion as markets lack much foresight to be able to see beyond.

FOMC—A LONG YAWN

The FOMC statement will arrive at 2pmET sans forecasts or dots that were delivered at the last meeting in December with the next updates due in March. Chair Powell’s press conference starts at 2:30pmET for around 45 minutes +/- depending upon how many ways he finds to say he’s not doing anything for now.

Markets have the next cut fully priced only by the July meeting and have two cuts priced for all of 2026. I wouldn’t necessarily pay attention to that; markets have missed countless inflection points at the Fed. Still, expect a patient message with policy being well situated for now.

ARE US LAYOFFS SURGING AGAIN?

Challenger layoffs for the month of January are likely to spike again when released next Thursday. UPS announced 30,000 cuts and Amazon announced 16,000. Still, I’m not tracking other large layoffs for the month so we’re likely looking at a spike to probably around the 80k mark that could be the second highest monthly tally since August. The UPS and Amazon layoffs are tied together through less demand for packages, rather than necessarily a wholesale deterioration in total job cuts in the US economy.

These latest announcements fall outside of the nonfarm reference period for January so next Friday’s figures won’t be affected.

Still, I went with 0k for the change in nonfarm payrolls in January and will provide a preview in Friday’s weekly.

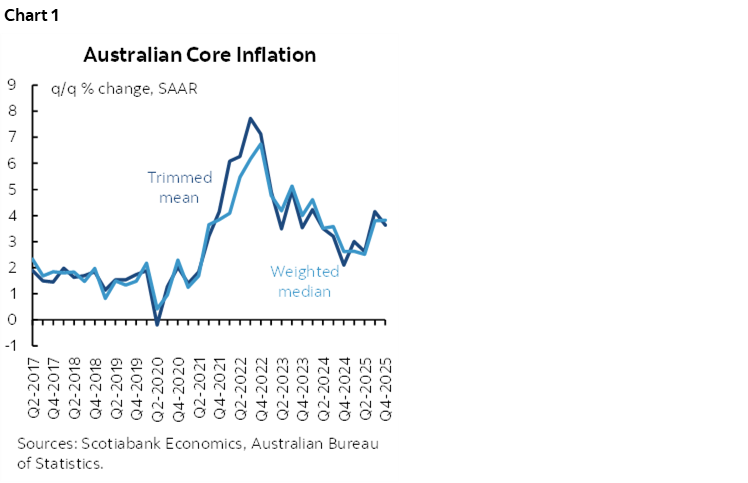

THE RBA MAY BE THE FIRST TO HIKE

The RBA’s meeting on February 3rd got a little more interesting after last evening’s Australian CPI figures. Pricing for the decision jumped a little higher to about 18bps of a quarter point hike. Pricing pushes a little higher for the March 17th meeting and more than a quarter-point hike is priced for May 5th. Several local shops changed their rate calls to a hike at next week’s meeting.

CPI ended the year up 3.8% y/y in December (3.4% prior, 3.6% consensus). Quarterly Q4 CPI was on the screws at 0.6% q/q SA nonannualized with trimmed mean (0.9%) and weighted median (0.9%) both matching expectations with a slight downward revision to median. At seasonally adjusted and annualized rates, trimmed mean CPI was up 3.6% q/q with weighted median up 3.8% (chart 1). Both are well above the RBA’s 2–3% headline CPI target range and signalling persistence.

TECH EARNINGS MAY MATTER MORE THAN CENTRAL BANKS

Tech earnings aplenty arrive in today’s after-market. Tesla (Q4 EPS US$0.45), Microsoft (US$3.92) and Meta (US$8.19) will release.

BRAZIL’S CENTRAL BANK TO HOLD

Brazil’s central bank also delivers its latest decision in the after-market (4:30pmET). A hold is widely expected.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.