ON DECK FOR TUESDAY, JANUARY 27TH

KEY POINTS:

- Markets are biding their time before developments heat up

- Party time for Canadian consumers this summer?

- South Korean markets ignored Trump’s tariff threat

- US consumer confidence leads a light data calendar

- BCCh likely to hold with cut risk

A very light session is on tap in terms of calendar-based risk before things heat up tomorrow with central banks and earnings. Today brings just a handful of second- or third-tier US macro releases and Chile’s central bank decision after nothing of note overnight.

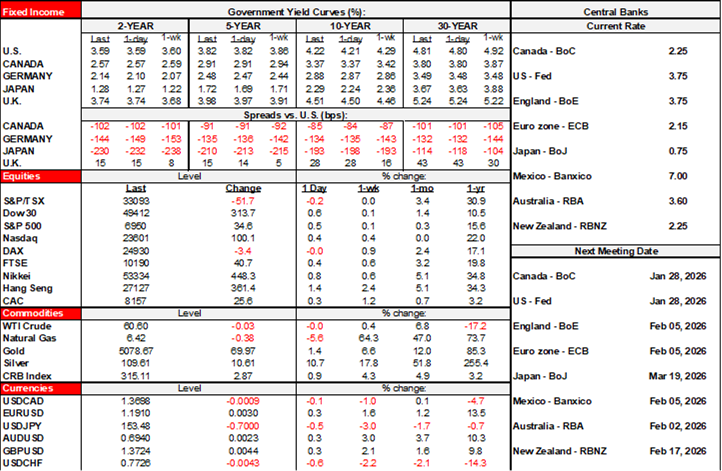

Markets are largely in wait-and-see mode. Stocks are generally a little higher across US equity futures and most European cash indices, but with TSX futures a touch lower. Sovereign bonds are mostly just treading water. Gold is up by over US$60 to US$5,075 after starting off strongly yesterday morning but then losing momentum. The dollar is broadly softer against all major crosses.

SOUTH KOREAN MARKETS IGNORE TARIFF THREAT

Korea’s Kospi rallied by 2¾% as traders assume Trump’s threat to raise tariffs against the country from 15% to 25% due to stalled progress passing a bad deal with the US will merely die on social media like many other tariff threats. The won is flat but slightly underperforming on a day of general dollar weakness, but not by much. South Korea’s front-end is outperforming others with the 2s yield down 3bps which is another big whoop-di-doo on tariff threats. Raise the price of giant screen TVs before the Super Bowl? Jack up cell phone bills? Brilliant…..

BCCH EXPECTED TO HOLD WITH CUT RISK

Chile’s central bank makes another rate decision at 4pmET. All but one in consensus expect a hold (Scotia’s Santiago-based Jorge Selaive expects a 25bps cut). Doves can point to the appreciating Chilean peso. CLP has rallied by just under 10% to the dollar since October. Inflation has fallen back to 3½% with core at 2.8% compared to the inflation target of around 3%. BCCh expects inflation to drop further to 3% over 2026H1.

CONSUMER CONFIDENCE HEADLINES US DATA

The US updates a series of second- and third-tier releases this morning.

- It starts with weekly ADP private payrolls (8:15amET) that will further inform tracking for next Wednesday’s monthly gauge.

- House prices have been showing some signs of life with the too-long-of-a-name-to-mention measure of repeat sale home prices (9amET) posting small gains in the past three months, but still only tracking just above 1% y/y in nominal terms and falling in inflation-adjusted terms which implies a negative housing wealth effect.

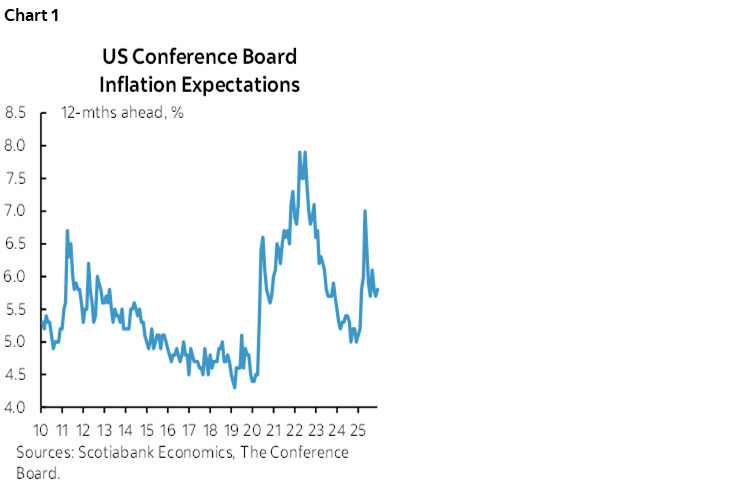

- Consumer confidence in January (10amET) will be the main release. It has been on a falling trend and is inches away from the lowest reading in about five years. Watch the measure of short-term inflation expectations (chart 1) with caution as consumers fundamentally don’t understand inflation. Consumers judge inflation by pointing to high frequency purchases like groceries and gas, they emphasize price levels (not inflation) instead of rates of change (inflation) and they fall prey to the representative agent problem that looks at spending patterns of all consumers and not individuals. The latter matters because it means even though individual consumers don’t buy cars, tvs, phones, concert tickets etc every day, someone somewhere is doing so and all prices therefore need to be taken into account.

- The Richmond Fed’s manufacturing index during January (10amET) will update tracking of ISM-manufacturing that is due out next week. So far, we know that the Empire, Philly and Dallas Fed measures improved over the prior month but the KC Fed’s measure was little changed. That could imply a small improvement in the ISM-manufacturing measure but still in contraction territory.

CANADA’S GST HAND-OUT SURE SMELLS LIKE ELECTION PRIMING

What will be the impact of Canada’s curiously named “Groceries and essentials benefits” that has absolutely nothing whatsoever to do with groceries? I’ll share what I wrote in staff/client chats yesterday.

The biggest of the effects stems from the one-time 50% boost to the GST credit by no later than June. The smaller effect stems from raising the existing GST credit amount by 25% for 5 years.

It could be party time in Canada this summer folks.

The combination of the announcements should boost nominal growth in disposable (after-taxes and transfers) income to about 6% q/q at a seasonally adjusted and annualized rate (SAAR) which is around double the run rate. That's mainly due to the one-time GST hand-out. Afterward, disposable income growth drops back to around 3% to 3½% q/q SAAR which is still healthy. The amounts are tax-free so they flow through 100% to disposable income.

Given past tendencies for the amounts to be spent and the fact that there are no strings attached to what people do with the money, that could mean consumption growth pops higher toward 5–6% q/q SAAR with the timing depending upon a) exactly when the payments go out in Q2 especially the one-time gift that is supposed to be sometime in Spring but no later than June, and b) how their saving behaviour changes.

Will households save it by putting the extra amounts toward funding spending on essentials they were going to consume in any event, or will they boost spending outright by purchasing all manner of other goodies? If they do the latter, then call it outright stimulus, or pump-priming, with or without an election call waiting in the wings. If they do the former, then it’s more about assistance. I suspect folks will boost total spending with a bit of a recognition lag after they see the extra funds in their accounts.

Another uncertainty is how much of this will drive higher prices versus higher volumes of spending. Only the latter counts toward GDP growth. Giving people more money to spend won't drive lower inflation including lower grocery prices, or lower borrowing costs. I thought we learned that lesson.

To the doves, priming consumption in Spring is another nail in the coffin of BoC rate cut hopes. Other economists are misrepresenting our views, however, in that we’re not calling for 2026H1 rate hikes and are instead very clear about hikes being a late year expectation.

The good part is that we're not looking at GST/HST rate cuts like we did the last time from mid-Dec 2024 to mid-February 2025. Over that period, measures of core inflation soared in m/m SAAR terms as the incidence effects of the cut were partly captured by retailers. From December to February, traditional core jumped to 3.2% to 5.6% m/m SAAR in each of the months, weighted median CPI jumped to 2.8%–4.0%, and trimmed mean jumped to 3.5% in each month.

Is it part of a ploy to prime the pump on the path to an election call? PM Carney got somewhat visibly testy in response to being questioned on this. He sort of denied it, which one would expect, but not explicitly. If poll aggregator sites that convert to seat projections like this one are on the mark, then the federal Liberals still have their work cut out for them in order to retain the party's existing seats, let alone pick up a couple for a majority that would make it worth an election call.

Also keep an eye on what measures come out of yesterday afternoon’s meeting between PM Carney and Ontario’s Premier Ford. Colour me suspicious. Ford went from slamming the Canada-China mini-deal over the very low quotas set for Chinese e-vehicles last week, to suddenly singing the praise of the Federal government’s auto initiatives as a joint review was pledged. Industry Minister Joly indicated there would be further developments over coming weeks on an auto sector strategy. Cha-ching. Someone’s support likely got bought behind closed doors with the means and ways pending further announcements.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.