ON DECK FOR MONDAY, JANUARY 26TH

KEY POINTS:

- Gold keeps soaring on economic uncertainty

- Trump’s tariff threat against Canada lacks details and credibility

- Canadian business: don’t use this as another excuse to avoid investing

- Carney administration to announce limited affordability measures today

- US durable goods orders—strong headline, muted core?

- Global Week Ahead—Excuses, Excuses! (reminder here)

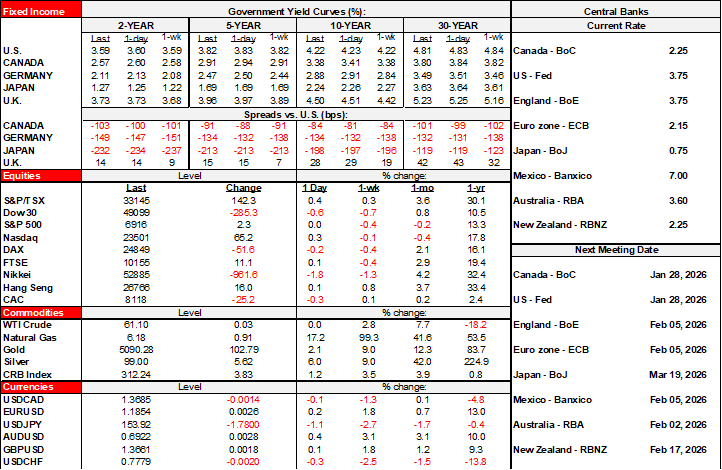

Gold is up by about US$100/oz and closing in on US$5,100. Silver is also up by about 6% and closing in on US$110/oz. These are the stand-out moves across asset classes to start the week. Canadian markets are largely shaking off Trump’s latest threat (see below) as CAD is slightly appreciating compared to Friday, TSX futures are outperforming US equity futures, Canadian government bond yields are only slightly outperforming US Ts and full-year BoC pricing is unchanged with markets still slightly leaning toward the next move being up by year-end.

The day’s line-up is light with only two notable things. One is that Canada’s government will announce affordability measures including increased GST credits at 9amET. The other is that the US updates durable goods orders that are expected to post a sharp headline gain on airplane orders, but muted growth in orders ex-air and defence (8:30amET).

TRUMP’S LATEST TARIFF THREAT WON’T HAPPEN

Trump delivered this threat against Canada on Saturday and followed it up with more general attacks yesterday. I’ll expand on arguments provided to staff and clients through chats on Saturday morning and that are embellished below.

What is Trump’s threat? Sign a deal with China, and a 100% tariff will be applied to everything.

Before turning to why it would never see the light of day, here are some more practical issues.

It wasn’t initially clear what deal Trump was referencing. The modest deal struck during PM Carney’s visit to China? In other words, the one that swaps canola for low e-vehicle quotas and other vague intentions?

Treasury Secretary Bessent clarified yesterday that it was a threat levied should Canada strike a broader agreement than the one the Carney administration inked during a visit to China. Bessent also said the tariff threat would depend on evidence that Canada is allowing Chinese goods to be dumped into the US; there is no such evidence of this happening or likelihood of such with one example being that the US prohibits imports of Chinese e-vehicles.

In my opinion, Bessent’s comments were an attempt at de-escalation, though it is often unclear the extent to which he speaks for Trump.

Carney also rightly pointed out that the US administration would be made aware ahead of time if a broader deal were being targeted since a 30-day notification of free trade deals with non-market economies is a requirement under the CUSMA/USMCA deal. Carney said no such notification has been made because “We have no intention of doing that with China or any other non-market economy.” Why would the US administration have levied this threat, knowing full well it hadn’t received such notification?

The added curiosity is that Trump had initially praised Carney for the deal with China and said it didn’t bother him. The only developments since he said that have included PM Carney’s aggressive speeches at Davos and at home, so perhaps this is about retribution through mere words. It may also be that the Ontario government’s tactics to sharply criticize the Canada-China mini-deal through grossly exaggerated and politically hyped fears drew unwanted US attention.

Extra curious is that Canada’s small deal with China merely winds back some of the protectionist measures each side took—such as banning Chinese e-vehicle imports, and China’s tariffs against Canadian canola and beef—rather than truly advancing trade other than loose, unspecified intentions to allow more Chinese investment. The US did the exact same thing last Fall.

Naturally, we don’t know details surrounding the threatened tariff, given the practice of leaving them out of social media posts. We don’t know timelines, what tariff tool could be used especially with IEEPA under SCOTUS review, whether CUSMA/USMCA-compliant trade would be exempt, etc etc.

But here’s why I think it’s an empty threat.

First, it would be devastating to US businesses across multiple industries. For example, when far, far lower tariffs were threatened early last year, auto industry execs such as Linamar’s CEO remarked that it would mean "it wouldn't be more than a week before we would see vehicle production in North America grind to a halt, and that means millions of people laid off, the majority of which would be in the U.S., and I can't see how that's a good thing for America."

Apply this reasoning across multiple industries. It could no longer be economical to supply oil and gas, hydro, any resources, or any manufactured product or service. Supply chains could freeze across multiple industries. Millions of American workers could be laid off. Millions of US consumers could find bare shelves, could be unable to heat their homes, and would be literally left in the dark.

Second, the market reaction to actual implementation could resurrect the “Liberation Day” trade after the April 2nd, 2025 tariff moves. Markets may lose faith in the US institutional framework, view it as having much higher country risk, and sell assets across the board toward a new equilibrium that reflects higher risk. That means dumping the dollar, dumping Treasuries, dumping credit and ditching equities. This is already a contributing factor to surging gold prices.

Third, such threats make it clear that the US administration is violating the original intent of pieces of legislation to impose tariffs. It further strengthens the case for SCOTUS to shoot down IEEPA tariffs although court observers suggest the next likely day on which court opinions may be offered is not until February 20th. Then to start the next round of challenges against the use of other tools. The entire tariff house of cards could come down in a striking rebuke.

Fourth, much of what is threatened never sees the light of day. Witness Greenland, European tariffs etc.

Fifth, if such a threat were actually carried out, then there would be enormous pressure to invoke major retaliation and that would include federal and provincial governments and consumers.

In conclusion, the thing about threats is that they have to be remotely credible. Nevertheless, instability only adds to the case to diversify away from the US. That has been underway for a while, as the share of total Canadian exports that go to the US has fallen from 85% about a quarter-century ago to 67% today and will likely keep falling over the next decade. Please also see my weekly that expands upon my view that USMCA/CUSMA risk is no excuse against investing in Canada after decades of such excuses have driven chronic under-investment.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.