ON DECK FOR FRIDAY, JANUARY 23RD

KEY POINTS:

- Risk appetite wobbles on competing effects from earnings, PMIs and the BoJ

- The US consumer cycle is showing strong signs it is maturing

- PMIs signal that global growth accelerated to kick off the new year

- Bank of Japan drives higher short-term yields, yen volatility

- UK retail sales were ok, not spectacular this holiday season

- Canadian retail sales: strong November, December uncertain

Risk appetite is a tad wobbly across global markets this morning. Tech earnings from Intel in yesterday’s after-market disappointed in terms of guidance which has markets a touch nervous ahead of next week’s onslaught of earnings across the ‘Magnificent 7.’ Competing against such sentiment is a batch of global purchasing managers’ indices that indicate strengthening global economic growth to kick off 2026. Developments out of Japan drove short-term JGB yields higher with the effects reverberating through some other major global benchmarks.

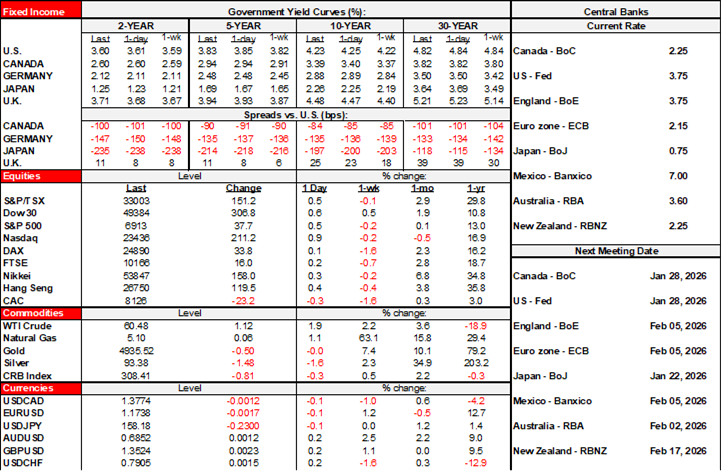

All of which has US equity futures slightly in the red with little changed TSX futures ahead of modest data risk on both sides of the border. European cash markets are offering a blend of small gains and small losses. US Treasury yields and Canadian government yields are little changed and the dollar—USD—is broadly softer against the majors. Gold is little changed, for a change, with oil up a buck.

A MATURING US CONSUMER CYCLE?

I think what also has markets a touch edgy is evidence of a maturing US consumer cycle as discussed with clients in morning chats yesterday following a batch of updated readings. Q4 consumption growth is tracking a respectable gain of 2.7% q/q after 3.5% growth in Q3. That’s a big part of why GDP nowcasts are looking so strong with the Atlanta Fed’s measure punching past 5% q/q annualized GDP growth in Q4. That’s great stuff for the US and world economies.

The rub lies in the fact that inflation-adjusted personal disposable income (after taxes and transfers) is tracking at only 1% q/q annualized growth in Q4. Spending more than is being taken in is driving the personal saving rate lower to 3.5% which is the lowest since October 2022 and down from the early 2024 peak of 6.4%. Take inflation off the saving rate and Americans are hardly saving at all. I’m not sure now is the time to be entertaining policies to get Americans to save more; then again, it seems it’s never the time.

The wealth effect on consumer spending has reversed with inflation-adjusted house prices in decline and given that most equities are owned by the upper income cohorts—not main street. Are consumers smoothing through the effects of tumbling payrolls and weakening incomes and a softening wealth effect in a rational sense by saving less only temporarily with sunnier days ahead? Or is this is a harbinger of a softer consumer in 2026? I lean to the latter interpretation as the zenith for US economic growth has probably passed and we’re now entering the period in which the lagging effects of uncertainty and policy changes can be more cleanly evaluated.

THE BOJ, YEN AND POLITICS

The Bank of Japan held its target rate at 0.75% as widely expected and by an 8–1 vote with one member voting for a 25bps hike. Governor Ueda held his cards close to his chest insofar as forward rate guidance was concerned. Forecast revisions offered a bit more of a signal. GDP growth was revised up for 2025 to 0.9% from 0.7%, the 2026 growth forecast was revised up three tenths to 1% and the 2027 forecast was revised down a bit to 0.8% from 1%. Core inflation ex-energy was revised up two-tenths to 3% in 2025 with 2026 raised two-tenths to 2% and 2027 raised a tick to 2.1%. Risks to the growth and inflation forecasts were described as balanced.

Markets reacted a touch hawkishly because of the signal that they have more confidence in sustained progress on inflation compared to the deflation years. Short-term Japanese bond yields increased by 3bps in 2s but rallied at the long end by about 4bps. Markets are leaning toward the next rate hike to be delivered at the June or July meetings.

The yen stole the show. It gyrated overnight, trading between 159.2 and about 157.60 around Governor Ueda’s press conference. Finance Minister Katayama noted “We’re always watching with a sense of urgency,” in reference to the yen’s volatility but did not comment on whether they intervened.

The bigger issue here—and which kept the BoJ relatively neutral—is the election campaign as PM Takaichi’s call for a vote on February 8th puts in play high uncertainty over the fiscal policy path that lies ahead.

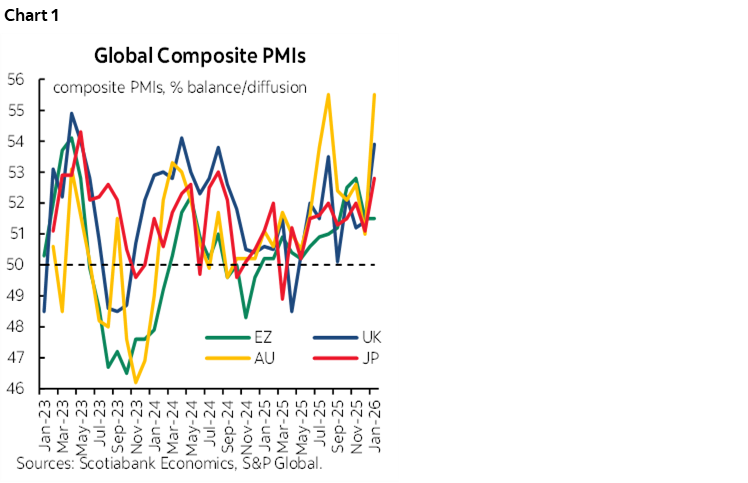

GLOBAL PMIs SIGNAL QUICKER GROWTH

A batch of global purchasing managers indices—soft data from folks making actual decisions in the economy—points to accelerating global GDP growth. Readings above 50 signal expansion, below, well, not. Here’s the run down.

- Eurozone: The composite PMI was flat at 51.5 as a slight deceleration in the growing services sector was offset by a slightly slower pace of contraction in manufacturing. Within the Eurozone we only get break outs for the two biggest economies at this stage and more later on. Germany led the way (52.5, 51.3 prior) as France’s composite PMI slipped into contraction (48.6, 50.0 prior) as services tanked.

- UK: Growth accelerated as the composite PMI picked up by 2.5 points to 53.9 because of both faster growth in services (54.3, 51.4 prior) and a pick up in manufacturing (51.6, 50.6 prior).

- Australia: Growth really accelerated here, with the composite PMI jumping 4.5 points to 55.5. Services gained almost five full points to 56 as manufacturing picked up a little steam (52.4, 51.6 prior).

- Japan: Here too, growth picked up a little with the composite gaining 1.7 points to 52.8. Faster growth mainly came through services (53.4, 51.6 prior) as manufacturing edged higher by 0.5 points to 51.5.

- India: The composite increased by 1.7 points to 59.5, beating all others in terms of the pace of growth. Both services (59.3, 58 prior) and manufacturing (56.8, 55.0 prior) accelerated.

- US: The US PMIs for January will be released at 9:45amET before 10amET revisions to the UofM’s consumer sentiment survey.

UK CONSUMERS DROVE AN OK HOLIDAY SEASON

UK retail sales beat expectations which drove short-term yields on gilts a little higher including a 3bps rise in 2s before the PMIs added to this, and a modest appreciation of sterling albeit that it’s a middle of the pack performer to the dollar this morning. Sales volumes were up by 0.4% m/m SA in December versus consensus expectations for a flat reading. Excluding fuel, volumes were up 0.3%. Both readings recovered from small declines the prior month. Call it ok, not spectacular.

CANADIAN RETAIL SALES—STRONG NOVEMBER, DECEMBER UNCERTAIN

We’ll get two readings for Canadian retail sales this morning and they will held to round out tracking of consumer spending in Q4. First is the revision to the initial estimate for November’s sales gain that Statcan had initially pegged at over 1% m/m without adjusting for price changes. That will include the first estimate of volumes separate from prices, and details by category of spending.

Statcan will also give an initial estimate for December’s sales in value terms. It would take a really strong December—despite snowstorms—to drive Q4 q/q sales volume growth into the black versus tracking of a small contraction. Then it’s over to whatever happened to services spending that dominates overall consumer spending.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.