ON DECK FOR WEDNESDAY, JANUARY 21ST

KEY POINTS:

- Gold keeps soaring ahead of two key events

- How markets may react to the SCOTUS hearing on Fed’s Cook

- Trump unplugged at Davos

- Linking Canadian producer prices and CPI

- UK markets shake off CPI

- Bank Indonesia held as the rupiah tumbles

Global markets are a bit calmer this morning than they were throughout yesterday. That could change as two events collide at similar times. One is Trump’s coming rant at Davos (around 9:30amET) and the mixture of threats, demands, insults and possible policy announcements ranging from housing to the remote chance that he slips in a choice for Fed Chair nominee. He is rather unlikely to get the standing ovation that Canadian PM Carney got yesterday when he delivered an excellent speech that captivated many of us who listened in real time (here).

Then starting 30 minutes later will be the SCOTUS hearing on Fed Governor Lisa Cook with markets keeping an eye on the tone of the court’s banter (see below).

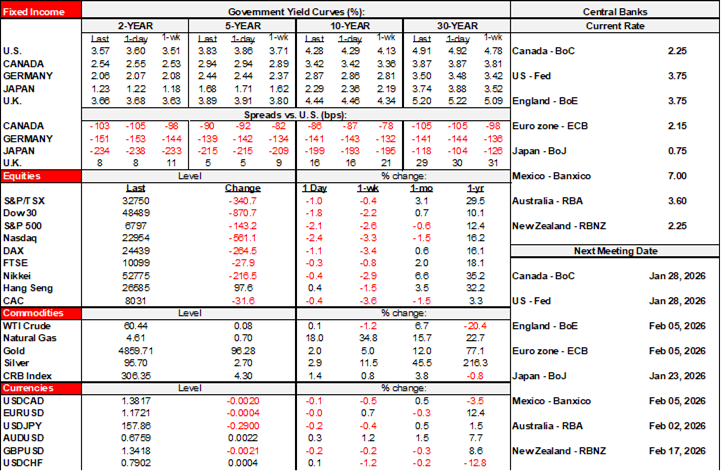

At the time of writing, however, market risk appetite is low. US equity futures are little changed, TSX futures are up a bit, and European cash equities are down by up to 1%. Gold is up another US$100/oz and is approaching US$4,900 as hard assets are preferred in an environment of weakened trust in the USD and as a safe haven amid troubled times. Sovereign bond yields are little changed outside of JGBs that bull flattened overnight with the long-end reversing much of the prior day’s sell off. Perhaps Japan’s finance minister’s call for calm across markets should be directed to her boss.

MARKETS AND THE SCOTUS HEARING ON FED’S COOK

The main focus will be upon the SCOTUS hearing (Trump v. Cook 25A312)—with Powell in attendance waving pom poms and doing leg kicks—to determine whether the Trump administration can eventually remove her from her role as the rest of the court proceedings evolve (10amET). That could open to door to nominating another individual. Most Fed watchers would have infinitely greater faith in the Fed running monetary policy independently—errors and all—than the administration and especially this administration given its persistent efforts to undermine institutions.

This is a good background piece that serves as both a refresher on the path taken so far and how the Court could look at the issues at hand.

A decision is not expected today. This is a hearing with oral arguments, like the hearing for IEEPA tariffs. You will be able to listen—at the Supreme Court’s website—to the tone of questioning put forth to the plaintiff and the defendant which may give you an idea of the bench’s bias.

The tone of questioning could influence financial markets even absent a decision that won’t come for a while. An actual decision—or opinion—isn’t likely for months to come. That could mean Cook will still attend the January, March, possibly April, and maybe even June FOMC meetings. This means she could outlast Powell at least in his capacity as Chair except in the darkest and least probable circumstances.

Frankly anyone with half a brain knows this is about Trump’s effort to shape the Fed’s BoG as he sees fit with the help of FHFA head and homebuilder, Bill Pulte. It would be the height of naiveté to assume that the administration is earnestly interested in weeding out avariciousness. At issue is interpreting ‘for cause’ in the Federal Reserve Act that defines the ability of the US President to sack a Board member. To date, the US courts have not supported the administration’s interpretation.

UK CORE CPI SHAKEN OFF BY MARKETS

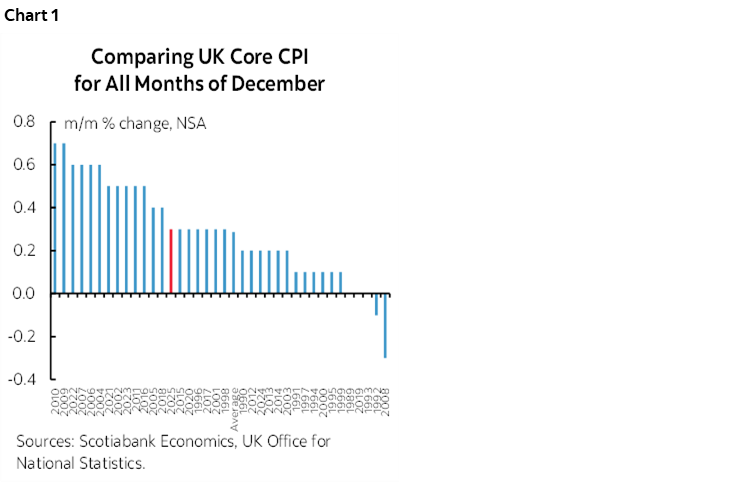

Sterling and gilts largely ignored UK CPI with no effect on BoE pricing for a hold on February 5th and only a 1–2bp further movement toward an April cut. Key is that after one of the weakest Novembers on record for core CPI in m/m NSA terms, December put in a bland reading pretty much smack dab in the middle of historical norms of like months of December (chart 1).

In year-ago terms, core CPI of 3.2% was unchanged and a tick beneath consensus versus headline CPI that accelerated to 3.4% y/y and a tick above consensus. Services inflation remains hot at 4.5% y/y, up a smidge but a touch lower than consensus.

BANK INDONESIA HOLDS ON RUPIAH WEAKNESS

Bank Indonesia held its policy rate unchanged at 4.75% as widely expected. The scope for policy surprises is often high for this central bank, but not at this point given the weakening rupiah that reflects rising geopolitical and trade policy risk overhanging markets. The rupiah is about 5% softer to the USD over about the past five months with the sell off accelerating this month.

A LEADING INDICATOR OF CANADIAN CPI

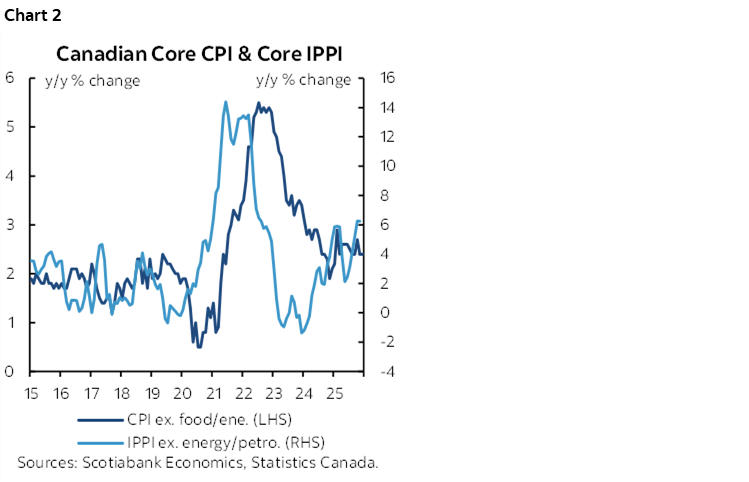

And while Canadian producer prices represent a pretty dry release that often sails under the market’s radar, they will be worth keeping an eye on given that they lead core CPI pressures. December’s reading is due at 8:30amET. Accelerating industrial product price indices ex-energy are pointing to pass through risk that carries upside influences on core CPI in the months ahead (chart 2). This is one part of the cost drivers behind inflation risk.

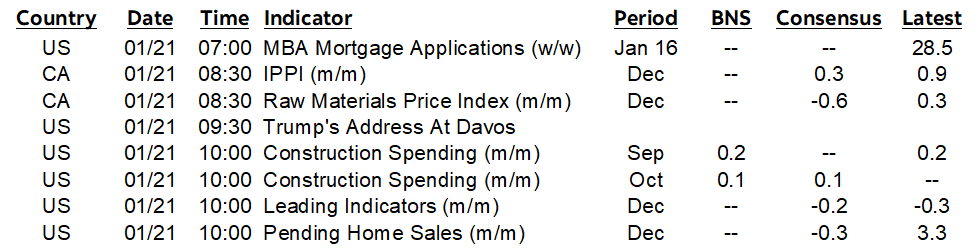

The US calendar is otherwise light with just construction spending for September and October (8:30amET) and pending home sales during December (10amET) due out.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.