ON DECK FOR TUESDAY, JANUARY 20TH

KEY POINTS:

- ‘Liberation Day’ redux?

- Stocks, bonds and the dollar fall…

- ...as Japanese election campaign stokes deepening concern over finances…

- ...and Trump escalates tensions with Europe including another tariff threat

- Possible SCOTUS tariff decision: embolden, embarrass or neither?

- PM Carney to speak at Davos this morning, Trump tomorrow

- UK markets shook off job market updates

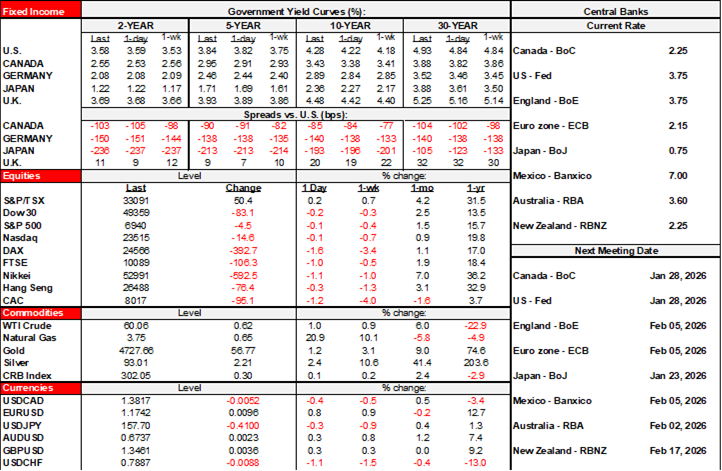

Prices for stocks and bonds are falling and the USD is out of favour. This is a smaller scale version of the ‘Liberation Day’ revolt; instigator take note! The prime catalysts appear to combine fears of lax Japanese fiscal policy and associated debt issuance, plus rising US and European tensions that are being driven by Trump as both sides escalate tensions over Greenland.

The result is that sovereign debt curves are bear steepening as the long ends across major markets are getting pummelled. 30-year yields are up by 27bps in Japan which, through carry, is associated with a 6–9bps sell off in 30s across Europe, the US and Canada. US equity futures are down by 1½% to 2% with TSX futures down by half as much and European cash equities are falling by up to 1¾%. The dollar is broadly softer.

What’s up? Commodities. Gold in particular, as the yellow metal gains another US$60/oz to a new nominal record of US$4,730. Oil is also slightly firmer by about 1%.

JAPANESE FISCAL AND MONETARY POLICY FEARS

What’s also up is market pricing for Bank of Japan action this year. OIS markets have raised pricing for full-year BoJ rate hikes to 51bps from Friday’s 44bps and from around 35bps a week or two ago. Markets are expecting the Bank of Japan to sterilize some of the increasing signs of a pivot toward more expansionary Japanese fiscal policy should PM Takaichi win the election she called yesterday for February 8th.

PM Takaichi remarked overnight that she would suspend the consumption tax on food for two years as “my strong desire.” On how to pay for it, she remarked that it would be through “a review of all expenditures and revenues, including subsidies, special tax breaks and nontax revenues, without issuing special government bonds.” Markets declared phooey on that, in favour of assuming that Takaichi would print more bonds. Why? Takaichi has a reputation—based upon her past stances—as a disciple of the late, former PM Abe and is known for her views in favour of lax fiscal policy. If she is not careful, then further upward pressure on the Japanese 30-year yield that has climbed by 85bps since November could see voters revolt and her campaign go down in flames.

TRUMP ESCALATES TENSIONS WITH EUROPE

President Trump banged out 10 posts on his own social media platform overnight. Topics ranged from a belligerent picture of him planting a US flag on Greenland’s soil, to unethically sharing a text from French President Macron, to attacks on Fed Governor Cook and protesters in Minnesota, to criticizing UK PM Starmer for his decision on a military base.

Among the threats was “I’ll put a 200% tariff on his wines and champagnes and he’ll join” in an attack on Macron’s decision to boycott Trump’s ‘Board of Peace’ of which Trump would be acting chairman in an effort to undermine the UN and other collective agencies while including folks like Putin and Lukashenko. Why is Canada among the ones saying yes??

SCOTUS DRAMA RETURNS

Not this again. They love us. They love us not. Maybe we will, maybe we won’t. What’s it to ya.

At or shortly after 10amET we’ll find out if this is tariff day, or if the pre-announced Opinion Day is focused upon other cases. I’m expecting it to be a waste of time unless SCOTUS really wants to either embolden or embarrass Trump the day before his Davos rant. Embolden, and critics of SCOTUS independence will howl. Embarrass, and Trump will scream. Either way, SCOTUS’s timing would probably invite rebukes, so maybe it’s best to keep teasing and to keep procrastinating while reminding us over and over of the frailties of the American judicial system. Polymarket continues to put less than 30% odds that SCOTUS rules in favour of Trump on tariffs.

The SCOTUS hearing concerning Federal Reserve Governor Lisa Cook is tomorrow. Fed Chair Powell will attend and drew scorn from Treasury Secretary Bessent for this decision.

UK JOB MARKET PUTS IN MIXED PERFORMANCE; MARKETS IGNORED

UK job market readings were largely ignored in the context of bigger global considerations this morning. That’s also because the releases followed last week’s solid activity readings but precede tomorrow’s UK CPI. Here’s the rundown of the figures for what it’s worth.

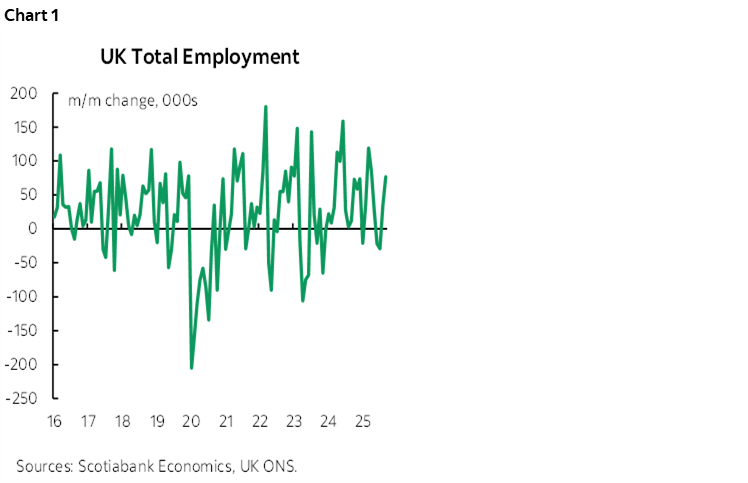

- total employment was up by 77k in November (chart 1). It lags and has performed a better over time—posting steady trend gains since 2021—because of employment at employers without formal payrolls, namely smaller businesses.

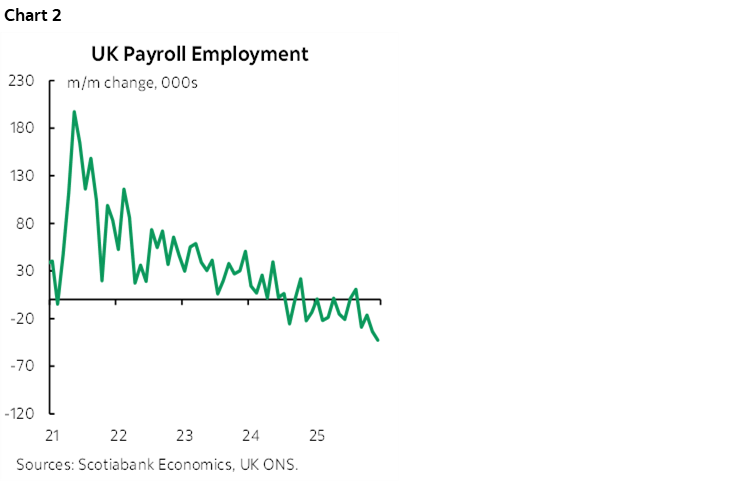

- payrolls fell for the fourth straight month, this time by another 42½ thousand positions in December (chart 2). Payrolls are down by 223k since the July 2024 peak.

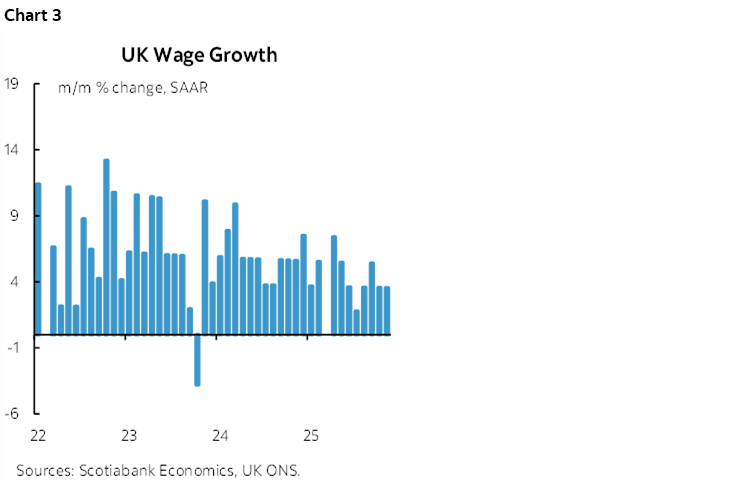

- wage growth held steady at 3½% m/m SAAR (chart 3).

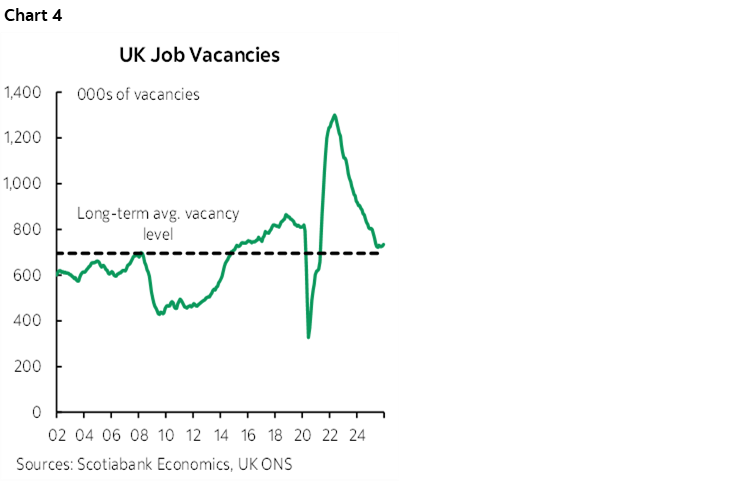

- job vacancies edged up a bit to 734,000 in December (chart 4).

- jobless claims were 18k in December but the prior month was revised down by about 23k to -3.3k.

DAVOS BRINGS CARNEY TODAY, TRUMP TOMORROW

The World Economic Forum at Davos commenced last evening with a boring concert and boring introductory speeches. Canadian PM Carney speaks this morning at 10:30amET; I hope the Europeans cheer. Trump has to wait until tomorrow to lash out at everyone—judging by his past speeches and ongoing tone—and it may be interesting to see what kind of reception he gets. The heavily European audience might well just walk out, given his threats. The fuller WEF Agenda is here.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.