ON DECK FOR FRIDAY, JANUARY 16TH

KEY POINTS:

- Markets mixed, oil up on volatile Iran headlines

- Well done, Carney & Co!

- Canada and China reset their relationship

- What Canada and China announced, and the risks...

- ...accompanying immediate benefits to agriculture and seafood industries…

- ...and medium-term benefits to investment and jobs in autos, energy, clean-tech

- Light other developments

Global markets are mixed to end the week. US and Canadian equity futures are slightly higher while European cash markets are a little lower after a softer tone in Japan, HK and mainland Chinese equities. Sovereign bond yields are gently higher across global benchmarks. The dollar is mixed, with CAD flat against it and otherwise small movements across others. Oil is up 1½% as volatile Iran headlines continue, including one about the US moving a carrier strike group to the Middle East. Gold is little changed.

The main consideration is the deal framework announced by Canada and China overnight. Otherwise there is light data to consider, such as Canadian housing stats for December (8:15amET) and US factory output in December (9:15amET). Fed-speak will drone on with Collins (10:50amET), Bowman (11amET), and Jefferson (3:30pmET) poised to take a swing.

CANADA AND CHINA PRESS RESET

Well done, PM Carney and Co. Canada’s delegation of cabinet members, provincial premiers and business lobbyists went to China to reset the approach of the past 10+ years that subjugated bilateral commerce to virtue-signalling and often hypocritical finger wagging. Commerce is in charge now. US protectionism was one of the motivators and the pivot toward China is happening across much of the world as a direct consequence that I’ve flagged dating back to Trump 1.0. If a main goal of US isolationism was to thwart China’s ambitions, then it’s failing. Economic necessity is the main driver as the US mistreats and abuses its Canadian relationship. So was bubbling frustration among Canadians over an underperforming economy for too long and partly as a by-product of policies that thwarted opportunity.

The deals will offer immediate, modest, and concentrated economic benefits to Canada. Most of the nearly immediate benefits will flow through to the agricultural and seafood sectors. Medium- and long-term benefits could include investment by China in sectors like autos, energy and clean tech—and the jobs that go along with that.

To be sure, there are risks aplenty. One is implementation risk on the long road ahead to which we can only say time will tell.

Second is how the US may react given, for example, that the US has thrown up roadblocks against imports of Chinese e-vehicles. Canada has no choice but to broaden its relations as the US retreats from its trusted economic partners in an increasingly protectionist and isolationist fashion. China’s long-run growth potential cannot be ignored to satisfy an isolationist US regime.

Third is that there are legitimate concerns about Chinese motives—for example, those of the SOEs and their ties to a uni-party state’s mixed objectives—and China’s human rights abuses. Carney’s response to this is pragmatic: “We take the world as it is—not as we wish it to be.” Perhaps that’s a touch dismissive, but Canada isn’t perfect either, and the US administration’s tactics are increasingly impure.

What Was Announced

Canada and China announced a trade deal and several memorandums of understanding at the conclusion of PM Carney’s visit. Go here, here, here, and here for more information and details. The announcements are a starting point, and the language is careful to emphasize further opportunities while raising just as many questions as those that were answered. A rather large one is exactly how and how much China may invest in Canadian energy and clean tech (batteries, solar, wind and energy storage). How Canada will get product to China in areas like energy absent further infrastructure development is also unclear.

On tariff changes, they reversed much, but not all, of the tariff hits that were bilaterally imposed last year. Here’s the summary.

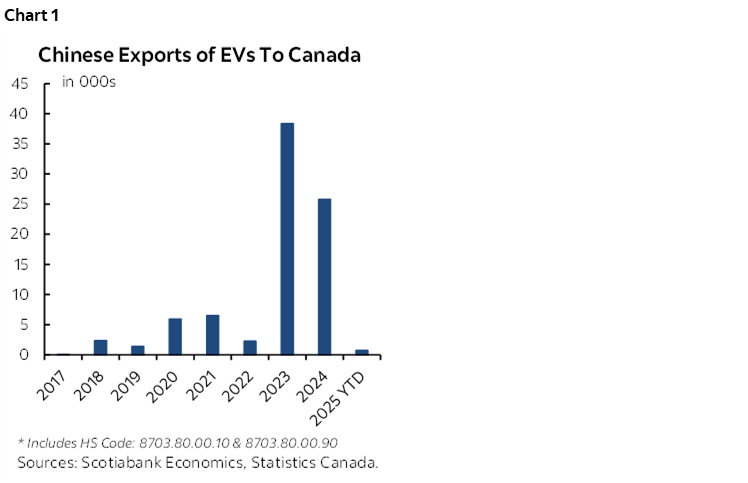

Chinese Electric Vehicles

Canada dropped tariffs on imports of Chinese electric vehicles from 100% to the most-favoured nation rate of 6.1% on the first 49,000 vehicles that are imported annually but rising to 70,000 within five years. 49k is the number of e-vehicles China sent to Canada in 2024 and equals just under 3% of new vehicles sold in Canada. Canadian imports of pure e-vehicles (ex-hybrids) from China are shown in chart 1. Lower priced EV models under C$35k will ultimately account for half of the quota by 2030.

Importantly, the deal pledges that China will make joint-venture auto investments in Canada within three years. It will be important to monitor how much of an investment and how many jobs were talking about particularly in light of opposition to the tariff reduction by the Ontario government.

Jobs, investment, more choice, cheaper and with cleaner emissions—what’s not to like? Trump’s preference toward gas guzzlers is against the way the world is going.

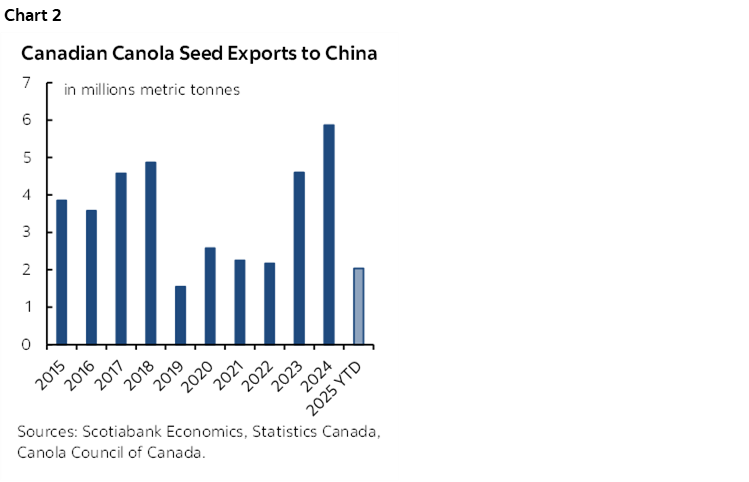

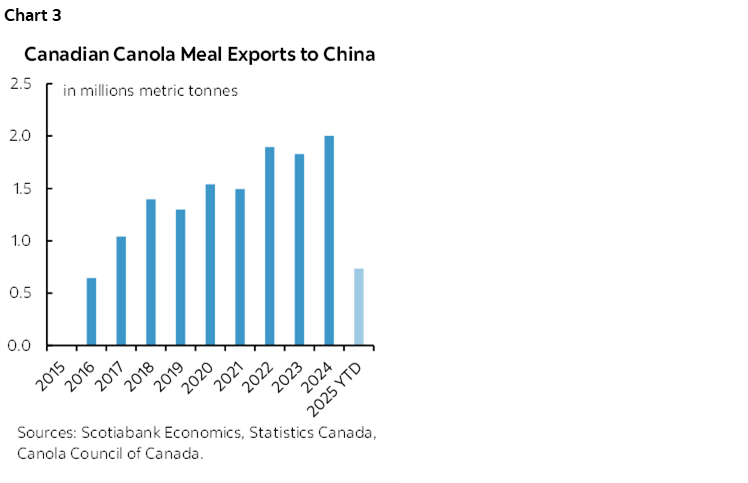

Canola

China imposed a 100% tariff on Canadian canola oil and canola meal last March and then a 76% tariff on Canadian canola seeds for a combined tariff of about 85% which will now drop to about 15%. The impact on canola producers was harsh as follows using statistics from the Canola Council of Canada:

- In 2024, China bought 5.86 million metric tonnes of Canola seed which dropped to 2.03 million over the first nine months of 2025 for an annualized total of 2.71 million tonnes. Chart 2 shows the reversal from the surge over 2023–24.

- 735.87 thousand metric tonnes of canola meal was exported to China in 2025 up to September, down from 2 million metric tonnes in 2024. Chart 3 shows this category falling off a cliff in 2025.

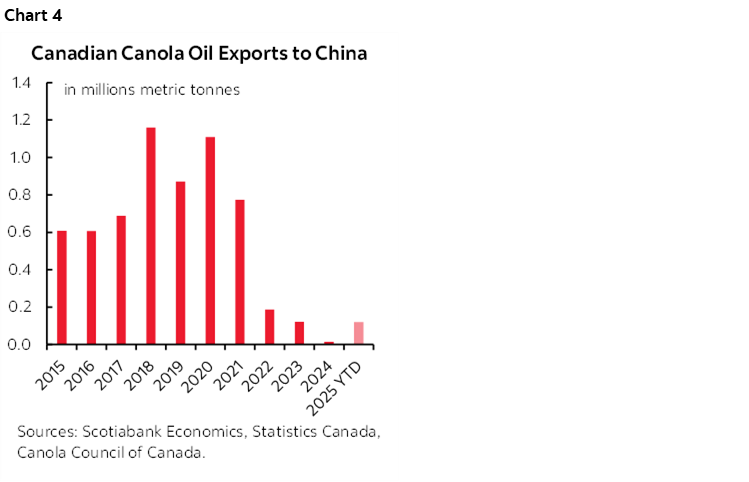

- Canola oil exports to China totalled 120.45 thousand metric tonnes over the first nine months in 2025, up from 15.35 in 2024. Chart 4 shows this category has collapsed since the pandemic.

Other

- China will drop tariffs on canola meal, lobsters, crabs and peas with some funny language. The tariff won’t drop until the start of March and for the rest of this year with no clarity on what lies beyond. It’s unclear why.

- China said it will drop visa requirements for Canadians who travel to China. I could be mistaken, but I don’t see Canada dropped visa requirements for Chinese visitors.

- Canada and China issued a loose pledge to increase two-way investment in clean energy and technology, agri-food, wood products and other sectors.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.