ON DECK FOR THURSDAY, JANUARY 15TH

KEY POINTS:

- Oil dives as Iran risk moderates for now

- Why Trump appeared to pivot

- US bank earnings continue

- Why gilts barely flinched after strong UK GDP

- Modest US, Canadian data risk on tap

- Canadian home sales likely affected by weather

- Fed's Barr to speak on stablecoin

A lighter note is offered this morning given weather and traffic.

An erratic US President is driving more market volatility this morning. Oil prices are off by over US$2/barrel after comments by Trump that at least temporarily allayed concern about escalating risk of an attack on Iran. Gold is also a little lower.

Trump is either seeking an off ramp from his earlier warnings or trying to lower Iran's guard after previously telegraphing his intentions. His claim that Iran has stopped executing protesters a) ignores the brutal crackdown to date, b) conflicts with reports of ongoing plans for executions, and c) seems based on his claim someone told him they'd stop. Perhaps Trump also looked at the reaction in higher oil prices against his stated goal of bringing them lower and realized the inconsistency. The absence of a carrier group in the Middle East given the focus on the Caribbean could have dawned upon him. Maybe he realized the risks of getting sucked in. Maybe he needs more time for US forces in the region to prepare including evacuations. We can only speculate, but at least for the moment, it's a de-escalation from the report from Reuters yesterday that European and Israeli officials were warning of a US strike on Iran within 24 hours.

Markets continue to digest US earnings from financials including BlackTock, Goldman and Morgan Stanley. Overnight markets saw gilts shrug after strong UK data while China updated December financing figures in a soft year. Relatively modest data risk and Fed-speak are also on the docket in Canada and the US.

GILTS BARELY REACTED TO STRONG UK DATA

The UK economy blew away expectations at the end of last year, but it's likely temporary. That's probably why gilts posted only a mild reaction. GDP grew by 0.3% m/m in December, tripling consensus. Support was broadly based. Industrial output soared by another 1.1% m/m (0.2% consensus) and the prior month was revised up to 1.3% m/m from 1.1%. This time it was driven by manufacturing that expanded by over 2%. Key was that auto production rebounded as the effects of a prior cyberattack on one company were shaken off. Services also outperformed, tripling expectations at 0.3% m/m. On the downside, construction is reeling, dropping 1.3% m/m after the prior month's revised drop was doubled to 1.2%.

NORTH AMERICAN CALENDAR

Canada and the US offer relatively minor data.

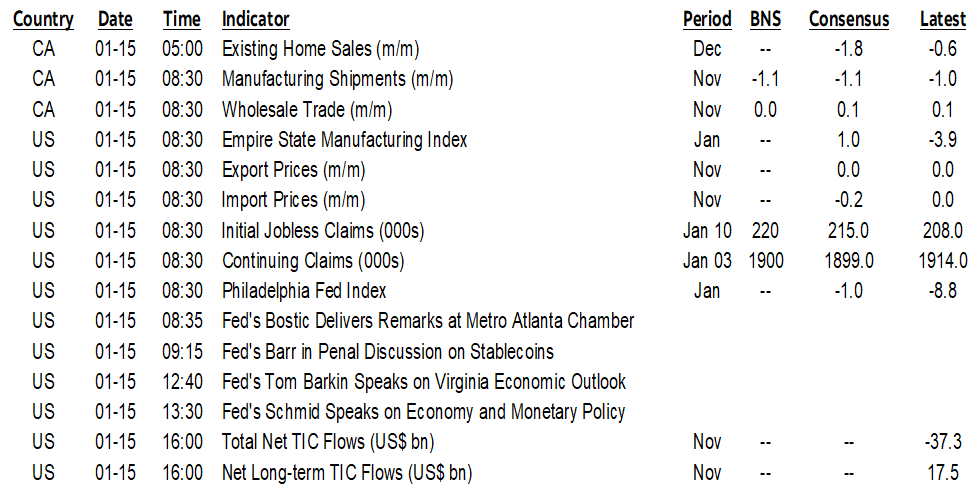

Canadian existing home sales fell 2.7% m/m SA in December. Weather likely played a role as winter gripped large parts of the country earlier than normal in recent years.

At 8:30amET, Statcan will release revised estimates for manufacturing sales and wholesale sales in November; initial estimates were -1.1% m/m and 0.1% respectively.

The US docket includes a pair of regional Fed manufacturing gauges—Empire and Philly (8:30amET)—to use as input into ISM-manufacturing estimates. Jobless claims are due at the same time.

Fed-speak continues with Vice Chair Barr speaking about stablecoins (9:15amET). Goolsbee, Barkin and Schmid also speak today.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.