ON DECK FOR WEDNESDAY, JANUARY 14TH

KEY POINTS:

- Gold and oil push higher as tough talk awaits action in Iran

- US bank earnings continue...

- ...as card caps stumble in Congress

- SCOTUS tariff ruling—today or teasing again?

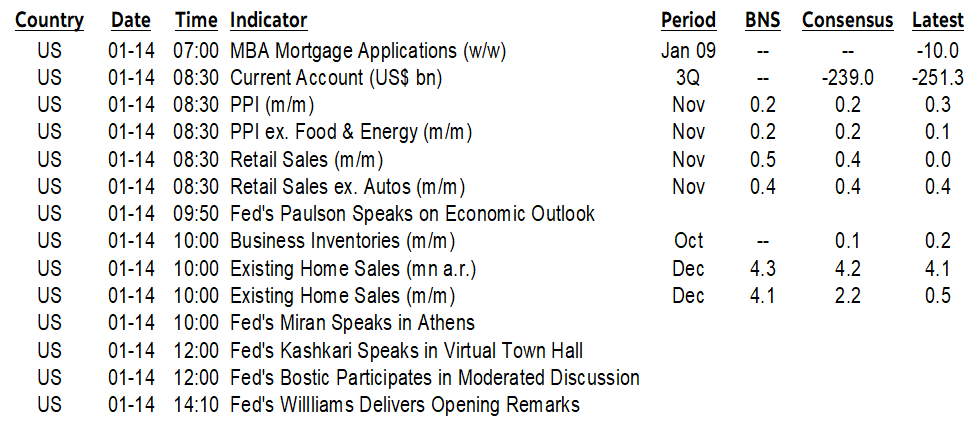

- US macro: PPI, retail sales, home resales

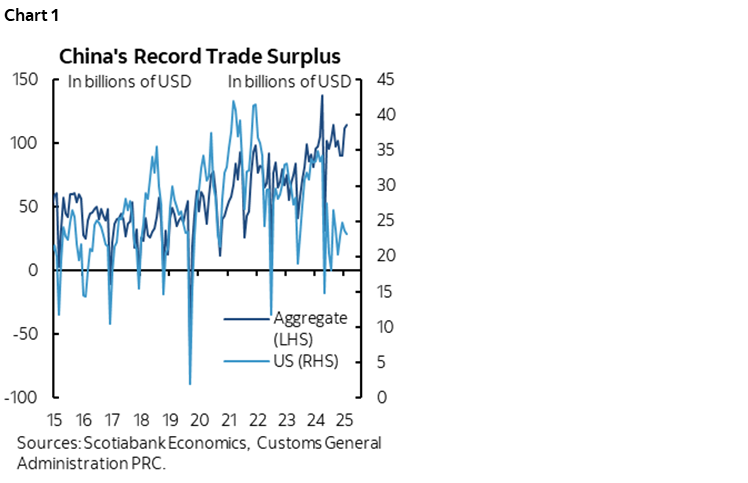

- Chinese trade diverts away from the US

- Carney in China—low headline risk until Friday

Gold and oil prices are up again by about US$50/oz and 1% respectively. Both are waiting on whether Trump will back his tough talk about how "help is on the way" by attacking Iran, how, and its effectiveness. I’ll say it again, the best revolutions in history were driven by enormous sacrifice by the domestic body politic (France, US, wall coming down etc) and foreign interventions carry enormous risks. Broader markets are digesting another round of US bank earnings, while awaiting a potential SCOTUS ruling on tariffs and several US data releases. Trump’s aggressive social media post about Greenland this morning claims that securing it would strengthen NATO as the UK and others in Europe are pondering whether to send troops and open consulates there.

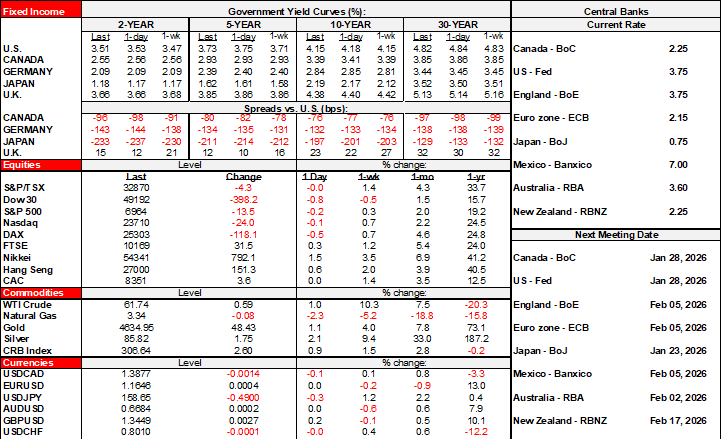

Broader risk appetite is playing defence. Stocks are somewhat mixed with US futures down about ½%, TSX futures up a touch on higher commodities, European bourses mixed after the Nikkei posted another 1½% rise on firming developments toward a Japanese election next month. The dollar is little changed.

BANK EARNINGS CONTINUE; CARD CAPS STALLING IN CONGRESS

US bank earnings continue with BofA, Wells and Citi delivering. BofA solidly beat on EPS, revenues and provisions. Wells Fargo disappointed even as adjusted EPS of US$1.76 beat consensus by almost a dime; net interest income disappointed and drove the share price lower. Citi is due out at 8amET (consensus Q4 EPS US$1.63).

Trump’s ill-conceived credit card rate caps have overshadowed the bank earnings season so far. Comments by House Speaker Johnson and Senate Majority Leader John Thune suggest that the cap is going nowhere. Their greater focus is a) keeping government open after January 30th to avert another shutdown, and b) scoping out room for another budget reconciliation bill that’s less big and less beautiful.

CHINESE TRADE — THE BEST OF BOTH WORLDS?

China’s trade surplus hit a new record high of US$1.2 trillion in 2025 as exports continued to grow by 6.6% y/y in December and nearly doubling consensus while imports grew by 5.7% which was nearly six times consensus. Trump’s incorrect ways of looking at trade balances are unlikely to be inflamed, however, as Chinese exports to the US fell by 20% last year which drove the US share of China’s exports to about 11% from nearly 15% the prior year before tariff lunacy kicked in. Trade diversion was on full display in China’s trade stats as the country’s export machine pivoted toward seeking growth elsewhere; its trade surplus with the US fell sharply (chart 1).

US MACRO REPORTS

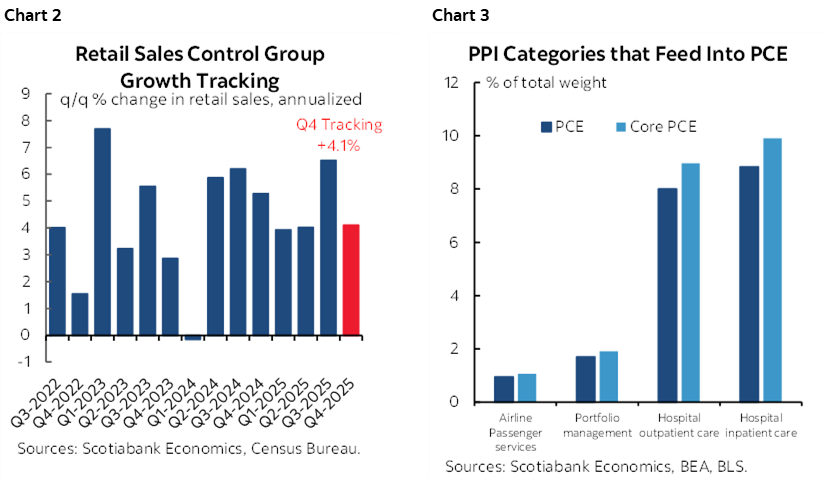

US macro data is on tap including an expected rise in retail sales (8:30amET), two PPI reports for October and November (8:30amET) that will only marginally help to inform PCE tracking because we won’t have CPI m/m for October or November, and home resales (10amET). Retail sales growth has been tracking a sharp slowdown in 2025Q4 pending this morning’s figures, but the important ‘control group’ that reflects how retail sales get captured in broad consumption within GDP has continued to register solid growth (chart 2). As for PPI, chart 3 shows the categories that are included in PCE and that markets are likely to pay the most attention to given their roughly one-fifth weighting in the Fed’s preferred inflation measure.

IS TODAY THE DAY FOR SCOTUS IEEPA DECISION?

The US Supreme Court has another opinion day today and could issue any possible IEEPA tariff decision at 10amET. Trump’s reaction would likely be rather quick in terms of shifting to other less appealing (to him) tariffs that themselves may be challenged.

OTHER

Canadian PM Carney is in China now to kick off three days of meetings including with President Xi Jinping (Friday) after Premier Li Qiang (Thursday). There will likely be low headline risk until then.

Fed-speak will continue with Philly Fed President Paulson (9:50amET), Governor Miran (10amET), Atlanta’s Bostic (12pmET) and NY’s Williams (2:10pmET) all speaking.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.