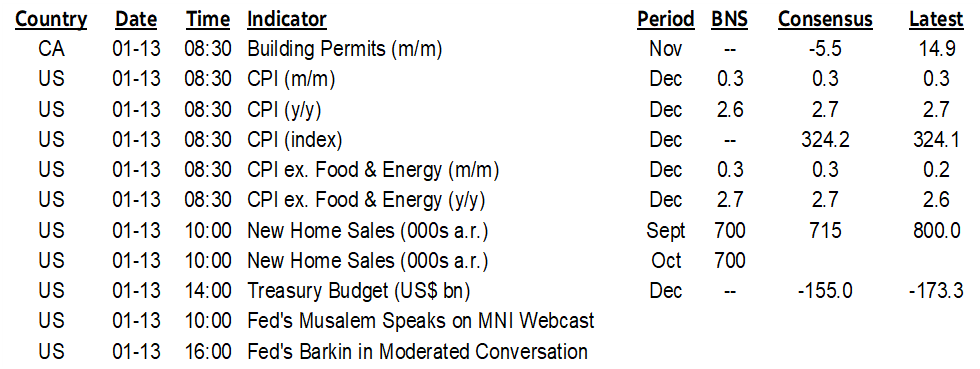

ON DECK FOR TUESDAY, JANUARY 13TH

KEY POINTS:

- Japan returns from holiday to rock bond markets

- PM Takaichi moving toward surprise election call…

- …in attempt at securing control to advance more activist policy

- Fed’s Williams makes it clear that the FOMC is on hold for a while…

- ...even if his confidence on the current policy stance is expressed on a lark…

- ...while several Board members may dissent in favour of easing this month

- Another fake US CPI report on tap

- Why Trump will scoff at foreign central banks rising in defence of Powell

- It’s hardly surprising that US bank earnings are beating again

Japan is back from a holiday and rocking global markets ahead of US CPI and bank earnings. The yen is underperforming, JGBs are bear steepening with the 10-year yield up 9bps and the Nikkei rallied by over 3%. The effects are reverberating across global bond markets through the diminishing carry trade. Sovereign yields are gently higher outside of Japan with N.A. equity futures and European equity cash markets playing defence.

The catalyst is that local news reports that PM Takaichi will dissolve the lower house and call a snap election for as soon as February 8th or 15th. Her aim is the build on the momentum since becoming PM in October to try to secure a single-party majority for the Labour Democratic Party. A disciple of the late former PM Shinzo Abe, Takaichi promotes aggressive fiscal stimulus which puts upward pressure on yields given Japan’s heavy indebtedness.

Markets have put the Trump-Fed spat on the back burner. Trump is very likely to ignore this morning’s statement in support of the Fed by a gaggle of foreign central banks (notably except for the BoJ). For one thing, they fall outside of the purview of ’America First’ rhetoric. For another, he could turn and say they’ve all done a lousy job which, in fairness, they did when it came to managing inflation in the pandemic. That’s not the same as saying monetary policy would be conducted better by politicians, but these central bankers have little to fall back on by way of their collective performance.

FED’S WILLIAMS CEMENTS A HOLD

NY Fed President Williams delivered a speech last evening (here) that made it clear the FOMC will pass on a rate move on January 28th—which has already been priced—and set a high bar for actions at other nearer term meetings such as March.

His speech was more balanced than the immediate flashes that crossed newswires. He acknowledged that labour demand is waning faster than supply and that various measures point to “increasing slack in the labour market” albeit “without signs of a sharp rise in layoffs or other indications of rapid deterioration.” Perhaps, though I think the labour situation is weakening more rapidly than he let on and after multiple under-the-hood considerations behind the headline numbers. Williams also expressed the opinion that the labour market should improve later in the year. His views on the full employment side of the dual mandate don’t make it sound like he’s in a rush to ease. We’ll see how that evolves and frankly I didn’t find any meat to back up his assertions on the outlook for jobs amid the various uncertainties (cycle, policy changes, AI etc).

On inflation, Williams expressed the view that “we’re seeing no signs of broader inflationary pressures.” He stated that tariffs have added around ½% to inflation of around 2¾% y/y while “the upside risks to inflation have lessened somewhat.” Williams expects inflation to peak around 2 ¾% to 3% y/y over 2026H1 and then fall back to 2% into 2027. I’d maintain that the inflationary forces across global supply chains are more insidious and longer-term in nature than more dovish views are anticipating.

Overall, Williams’ remark that “Monetary policy is now well positioned to support the stabilization of the labour market and the return of inflation to the FOMC’s longer-run goal of 2 percent” and his emphasis upon resilience are code language for a pause.

We’ll see how this evolves. I find he’s too dismissive toward sustained labour market weakness and sustained inflation risk which still makes what to do in future an empirical question with respect to which side of the mandate deteriorates the most. In my opinion, that’s jobs and I wouldn’t take comfort in any measures of inflation expectations as they’re all flawed and routinely fail to anticipate broad trends in disinflationary or inflationary pressures over the decades.

There is an alternative way of understanding the Committee’s stance. It’s feasible that the FOMC doesn’t wish to embolden bad fiscal, trade and immigration policies or be viewed as willing to wilt under pressure from Trump in defence of the Fed’s independence. It’s also feasible you will see several dissenters at the January 28th meeting including perhaps at least 2–3 on the Board. #divisions.

US CPI WILL BE MEANINGLESS

After Williams’ remarks, it’s pretty clear that this morning’s CPI report for December (8:30amET) won’t matter to any nearer term decisions by the FOMC. That bolsters the case for why this report won’t matter at all. It’s not a ‘clean’ reading precisely in part because the jumping off point from the prior report was not a clean reading.

See my weekly for a preview (here). Here's the distribution of forecasts US core CPI by frequency of forecaster:

- 2 x 0.5% m/m

- 25 x 0.4%

- 34 x 0.3% (including Scotia)

- 11 x 0.2%

In other words, it's a consensus with no real conviction. If anyone tells you they have high conviction, then count your knuckles after shaking hands with them.

Why? There are too many distortions. It’s garbage data.

- only half a month of price data was collected for November for the most part after most October price data wasn't collected. Some point to that being the period of holiday discounting. The BLS did, however, note that they "attempted to collect data for the entire month of November" so we don't know exactly how much to weight that argument. Plus, maybe the fifth highest November SA factor for core CPI on record wasn't high enough given this, or maybe it was. Watch this month’s SA factor that has tended to be high in recent years (chart 1). Besides, it's not like major categories like OER and rent go on sale.

- year-ago CPI and core CPI offered similar issues: if this November was only partially collected in a period of peak discounting compared to full collection during the prior November then the y/y rate may have been artificially depressed in which case we bounce higher by a reset base effect and full collection of data in this December's reading compared to last December’s full month price collection.

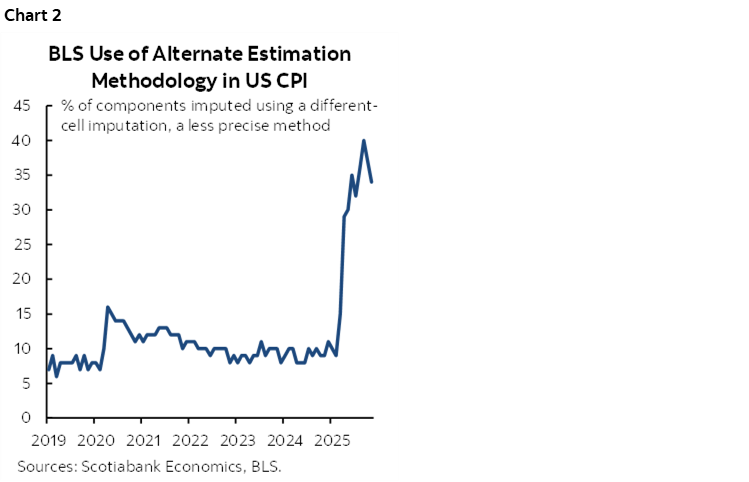

- the share of the basket being made up by proxy methods instead of direct collection of price data continues to float around record highs (chart 2).

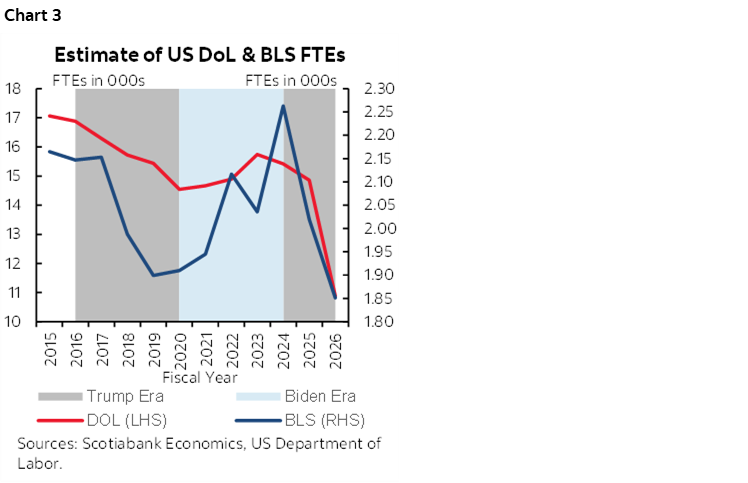

And I don't fundamentally trust the data we're getting from the BLS. Massive staff and resource cuts under Trump 1.0 and 2.0 that Biden attempted to reverse in between both periods carry lasting damage (chart 3). Those cuts affect sampling, data collection, turnaround, revisions, and possibly objectivity.

US BANK EARNINGS SEASON BEGINS

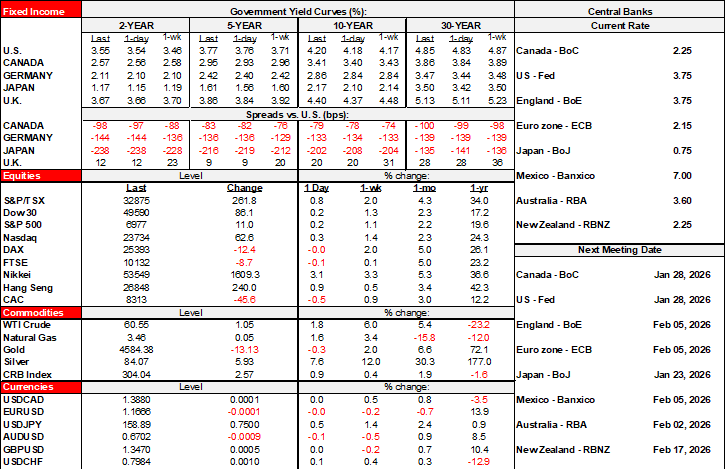

US bank earnings season kicks off. JP Morgan beat with adjusted EPS of US$5.23 (consensus Q4 EPS US$5.0) and stronger than expected revenues in aggregate and across most units except investment banking. BoNYM also beat with EPS of US$2.02 (consensus Q4 EPS US$1.99) and stronger than expected revenues.

These beats shouldn’t be much of a surprise. You’re usually better off betting on a beat given cautious US analysts after the dot-bomb and SOX periods.

OTHER

The US also updates the weekly ADP private payrolls measure (8:15amET), new home sales for October (10amET) that are expected to drop, and the federal budget balance for December (2pmET). There will also be at least two more Fed speakers on tap including St. Louis President Musalem (10amET) and Richmond’s Barkin (4pmET), both of whom are nonvoting in 2026.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.