ON DECK FOR MONDAY, JANUARY 12TH

KEY POINTS:

- Markets rebel against Trump administration’s latest assault of the Fed

- Trump administration delivers subpoena to Powell’s Fed…

- ...and Powell’s forceful counter is right on the mark

- How the Senate acts upon Trump’s eventual nominee for Fed chair could be key

- How Trump’s credit card rate caps would backfire

- Global Week Ahead — War is Peace (reminder here)

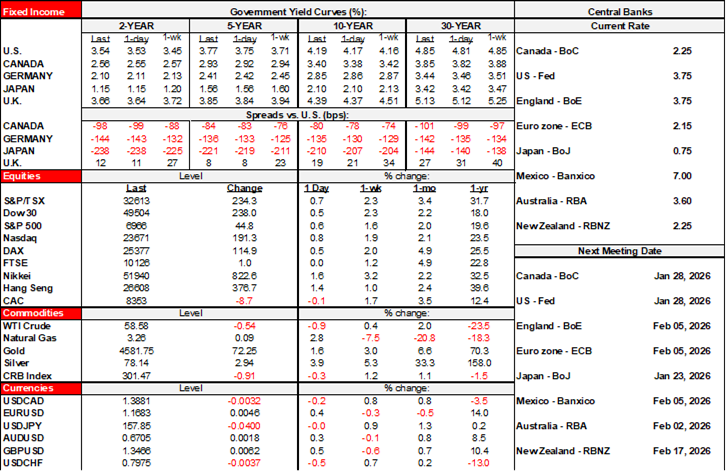

Markets are rebelling against President Trump’s attack on Chair Powell and the Federal Reserve. Gold is up by about US$75/oz to nearly US$4,600. Longer-end Treasury yields are punching higher with the 10-year up 3bps and 30s up 4bps. The USD is broadly weaker against major crosses. Crypto currencies are hardly serving as a hedge against political meddling in the dollar as they’re mostly down as well. S&P equity futures are down by about -¾%.

The assault on the Fed is dominating markets but the reaction may be limited thus far by virtue of the fact it’s a national holiday in Japan and so Asian market reaction was constrained overnight. Let’s see the full reaction in the North American session, though I wouldn’t be surprised to see a consolidation of the early reaction and a pivot toward other developments on tap for the week like tomorrow’s US CPI, US bank earnings, geopolitical risks etc.

Other overnight developments were light. Australian household spending beat expectations (1% m/m, 0.6% consensus) which is driving mild underperformance of Australia’s front-end. India’s CPI was softer than expected (1.3% y/y, 1.6% consensus) which had no effect on the 50–50 market pricing for a quarter point cut by the RBI on February 6th.

TRUMP ADMINISTRATION EXPLICITLY THREATENS THE FED

At issue is the move by the Trump administration’s Department of Justice under Pam Bondi—and possibly an extension of efforts by FHFA head Bill Pulte—to serve a grand jury subpoena that threatens a criminal indictment of Chair Powell for what he allegedly said about renovations during his testimony before Congress in June. And if you believe it has anything to do with that, then in my opinion, there’s no hope for further understanding.

Chair Powell’s unprecedented and brave counter of the allegation was released last evening (here) and stated “This new threat is not about my testimony last June or about the renovation of the Federal Reserve buildings. The threat of criminal charges is a consequence of the Federal Reserve setting interest rates based on our best assessment of what will serve the public, rather than following the preferences of the president.” Good for you. He perhaps wisely resisted the opportunity to point the finger at other famous renovations. I haven’t always agreed with Powell’s judgement—including the aftermath of the pandemic—but I’d be vastly more concerned about a scenario in which the administration of the day is calling the shots on monetary policy.

Would it fly legally? I would think not, but the often-complicit Supreme Court raises doubts should it go that far and of course I’m no lawyer, let alone a lawyer well versed in the specific matters at hand. The move comes before the administration’s other case against Fed Governor Cook one week from Wednesday before the Supreme Court that is unlikely rule in favour of the administration, although this is not assured. One would hope the US legal system can see through the true motives of the subpoena.

The risks could cut deeper. Republican Senator Tom Tillis bluntly stated he would not approve any fed chair nominees “until this legal matter is fully resolved.” On his own, he cannot be effective. But the GOP has a slim majority in the Senate with 53 seats to the Dems’ 45 and 2 independents who caucus with the Dems. One scenario could be if there are three other principled GOP Senators who may join him in, say, rejecting a Fed Chair candidate who is deemed to be too close to the administration. Trump 1.0 set precedent for this administration with rejected candidates.

WHY CREDIT CARD INTEREST RATE CAPS WOULD BACKFIRE

On Friday evening, Trump delivered this social media post stating that he is “calling for a one-year cap on credit card interest rates of 10%” effective January 20th which he wasn’t shy about noting is the anniversary of his inauguration day. It may never see the light of day or be sustained given industry lobbying around arguments shared below.

The motive for such action is political and not rooted in any market failure. The credit card industry is a hotly competitive one in which borrowers have choices. They have choices not only across competing cards, but they can also choose to borrow on cheaper lines of credit—secured and unsecured—or installment loans or mortgages. Americans do a lot of the latter because of mortgage interest deductibility that tilts borrowing preferences more toward mortgages than elsewhere in the world. Ill-advised auto loan interest deductibility would have the same effect of altering the after-tax costs of different types of debt.

Here’s why such a move to cap credit card rates could spectacularly backfire:

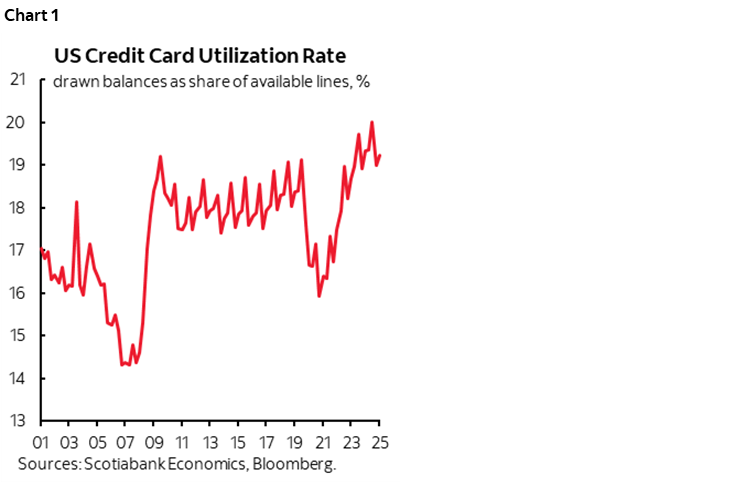

- The end of free credit for most: A May 2025 NY Fed study showed only 46% of American credit card holders carried a credit card balance at least once in the past year, the so-called extender rate (p.56, chart 28 here). The other 54% who manage their money wisely got free money for the grace period which can be several weeks. Only less than 20% of available credit card lines are utilized (chart 1). Set a cap on credit card rates for the rest and the grace period for the ones who get free credit would likely collapse.

- Buh-bye minimum monthly payments: The folks who do carry a balance would likely have to pay higher minimum monthly payments for card companies to recoup the effects.

- Other borrowing costs would rise: Card companies would have no choice but to raise other fees like annual fees, FX conversions and scale back loyalty programs etc.

- Card issuance would suffer: Perhaps existing card holders would be cancelled which is within the rights of the companies and new card issuance would be curtailed for all but the most credit worthy customers.

- Choice: There are substitutes for prudent money management. Eg. lines, mortgages, installment loans. You would have to prove market failure to demonstrate that people have no choice than to borrow on cards.

- Financial stability could suffer: The impact upon firms that rely relatively more on card revenues—like monolines—could be destabilizing to the financial system.

In short, education and efforts to raise financial literacy may be more effective than rate caps and so could efforts to address severe income disparities within the US economy that are not the fault of the cards industry.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.