ON DECK FOR MONDAY, FEBRUARY 9TH

KEY POINTS:

- What happened in Japan, stayed in Japan

- Japan’s election drive equities and bond yields higher...

- ...as Japanese and US equity markets trade places

- BoJ hike guidance, ebbing contraction of Japanese real wages faded behind election

- Mexican core inflation continues to rise, validating Banxico hold

- Fed’s Waller, Miran, Bostic to speak

- Canada just can’t quash those election rumours

- Global Week Ahead — Trading Places (here)

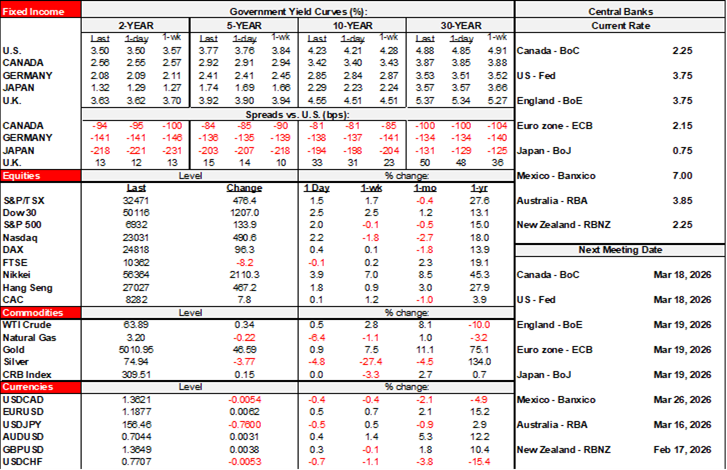

Japanese stocks gained nearly 4% with solid gains across every major sector but led by IT, JGB yields rose 3bps in 2s and double that in 10s and the yen strengthened a touch to become roughly tied with CHF and the euro as outperformers on a down day for the dollar. All of that was in reaction to Japan's election results. Very little of the enthusiasm spread elsewhere. Hawkish BoJ Board member talk and Japanese real wage figures played a back seat to election results.

There is nothing material on tap in the N.A. session. Cyber currencies are selling off this morning while gold gains 1%.

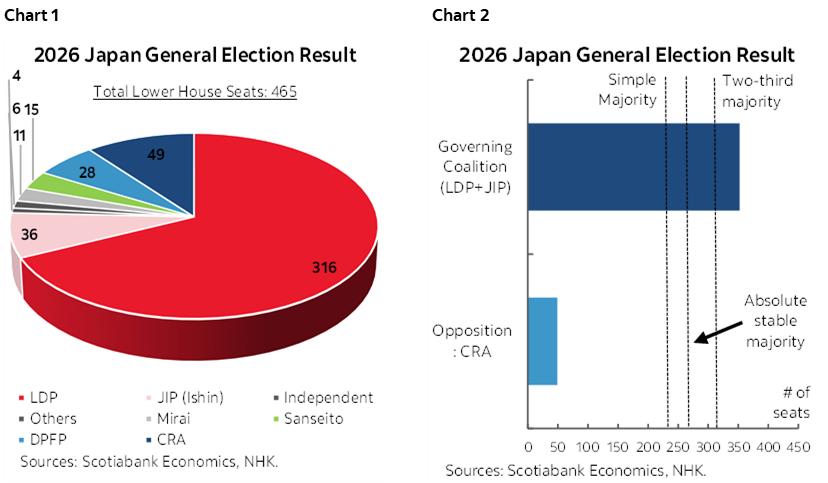

Japan’s Election — Trading Places

Japan's Liberal Democratic Party alone won a super-majority in the lower house of its Diet (charts 1, 2). It didn't even need its new coalition partner—the Japan Innovation Party—to pull it off. The 316 seats that went to the LDP was a massive gain from the 198 going in and exceeds the 310 needed for a so-called super majority. This was PM Takaichi’s dream result because it means the LDP can chair and possess a majority of seats on the powerful committees, can override Upper House rulings with a two-thirds vote which matters since the LDP does not hold enough seats in the Upper House, and pursue changes to the Constitution. Constitutional changes could address Japan’s pacifist stance but this requires a referendum.

That was the easy part. Now the pressure is on to see what PM Takaichi does. She will likely move very quickly to maintain momentum.

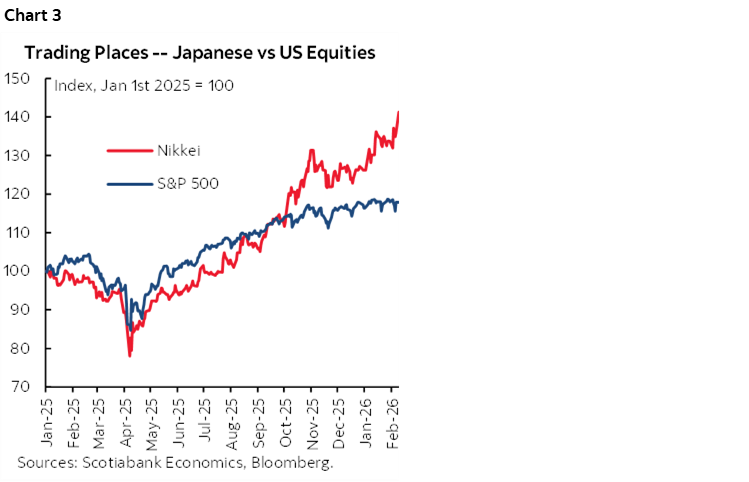

For now, the market response is reinforcing the view that Japan and the US have traded places (chart 3). US equity futures are slightly lower this morning while Japanese equities soar. It all started around when Takaichi first became PM last October and coincided with greater questions over US tech, the Fed outlook, and the state of the US job market and investment picture ex-AI. It was previously the case that the carry trade—borrowing cheaply in yen to finance Japanese investments abroad—was reversing as the Bank of Japan pivoted to tighter monetary policy. Money was flowing back into Japan. That incentive is now stronger. Japanese equities offer more competition to US equities.

In short, there’s a new kid in town and we’ll see how enamoured Trump remains as a more intense competitor for equity flows steps up.

Otherwise Light Developments

Weekend developments were otherwise light.

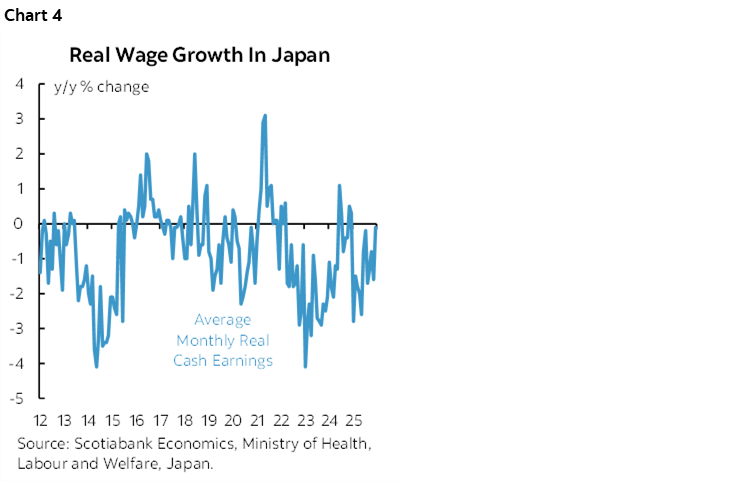

Japanese wage growth accelerated to 2.4% y/y in December from an upwardly revised 1.7% (previously 0.5%) the prior month. That still means real wages are falling (-0.1% y/y) but at a lessening pace including positive revisions (chart 4).

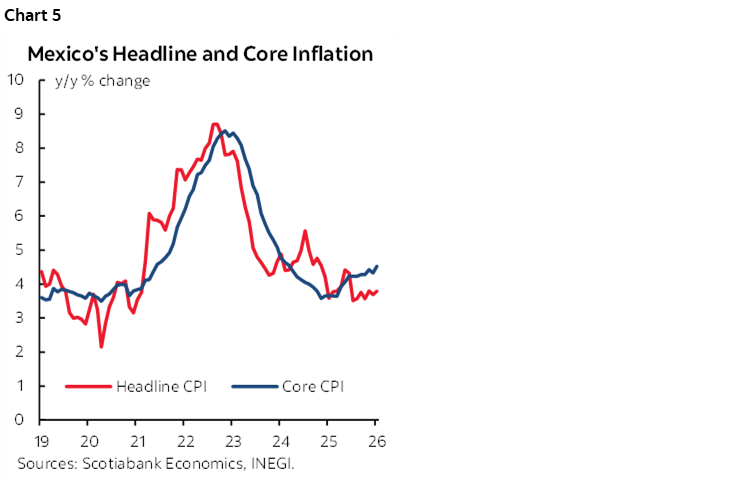

Mexico’s CPI landed on the screws at 0.4% m/m (3.8% y/y) in January and ditto for core at 0.6% m/m (4.5% y/y). Core CPI continues to accelerated off the lows of late 2024 into early 2025 (chart 5). Hence why Banxico held last Thursday with markets not expecting much action for an extended period.

The Canadian election rumour mill remains alive and kicking. PM Carney and Ontario Premier Ford—a ‘Tory’—reportedly discussed an early federal election (here). A federal communications spokesperson tried to downplay the talk which is as expected. Then again, I watched PM Carney’s courtship by the BoE while in his post at the BoC being met with endless denials of interest until ‘ok’.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.