ON DECK FOR FRIDAY, FEBRUARY 6TH

KEY POINTS:

- Markets seeking a better end to a rough week

- Canadian jobs — fifth time lucky?

- BoC’s Macklem reminds markets of the supply side’s constraints…

- …and beseeches firms to rise to the occasion

- RBI holds, indicates neutral bias

- US UofM sentiment, Fed’s Jefferson speaks

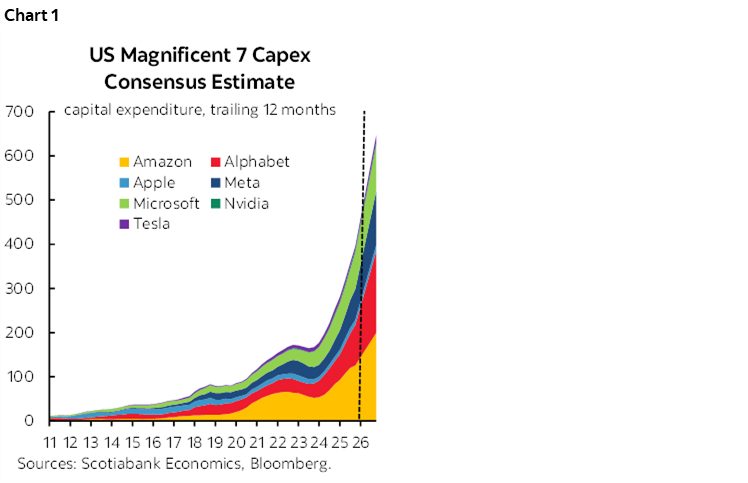

Risk appetite is a touch more constructive so far this morning; let’s hope it ends the week that way. Stock futures and cash markets are broadly higher across N.A. and Europe except Italy which almost seems rude as the Milan Olympics arrive today. The gain in US futures is despite Amazon’s plunge following release of its earnings in yesterday’s after-market as weakness spills over. Markets are pushing back on the massive cap-ex plans of the Mag7 including Amazon’s US$200B guidance for this year that adds to the tally in chart 1. Sovereign bonds are mixed with US Ts broadly cheaper while European yields are broadly lower. The dollar is mixed but with a bit of a soft under belly. Cyber currencies are mostly higher after yesterday’s plunge. Modest gains are being registered by gold and silver prices.

My main focus will be upon Canadian jobs and related metrics for the month of January (8:30amET) while US data could be a follow-up wild card.

Canadian Jobs — Spin the Wheel Time

Will it be a fifth time lucky for Canada, or about payback? Most within consensus think it will be another mild gain but no one should have much confidence in the estimates. Eventually the bears will be right like a stopped clock twice a day. Yet so far, Canada has surprisingly created almost 200k jobs over the past four months of consecutive gains. I think part of the reason is despite trade uncertainty as the capital:labour ratio shifts more toward labour to achieve output plans while business investment continues to shrink. See my weekly for a further preview and, well, good luck!

Watch the trend, not any one particular month. Beware of confirmation bias that overreacts to a drop or a large gain among some who have seemingly been longing for some bad news to support their hate on Canada. Ideal would be a modest change.

Light Overnight — German Data, RBI Hold

German data was mixed overnight. Exports were up by a whopping 4% m/m SA (1.1% consensus) in December after falling by 2.5% the prior month. Industrial output fell by 1.9% m/m (-0.3% consensus) during the same month after rising by 0.7%. The previous day’s massive back-to-back gains in factory orders during November (5.7%) and December (7.8%) will likely lift industrial output in coming months.

India’s central bank held its repurchase rate unchanged at 5.25% as most had anticipated. The RBI described its current rate as “appropriate” with a “neutral stance” while noting that trade deals support the economic outlook and inflation risk through the soft rupee and commodity prices remain material. India’s bond yields rose slightly overnight.

Amazon's earnings in the after-market may dominate the rest of the global line-up unless UofM rattles some cages.

US UofM Sentiment

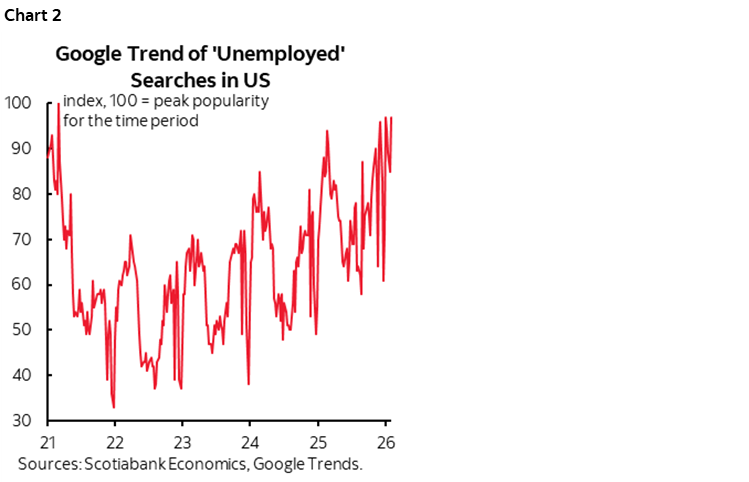

US markets face a light calendar. UofM consumer sentiment for February (10amET) is more driven by markets and cash flow than the Conference Board’s consumer confidence reading. That means that it will be less sensitive to deteriorating job markets but more sensitive to wavering market conditions. Watch expected unemployment over the coming year as a highly correlated predictor of eventual unemployment. Do so while noting that clearly Americans have rising worries on their minds toward the state of the labour market (chart 2).

The Fed’s Vice Chair Jefferson then speaks on the economic outlook and the supply side inflation dynamics at 12pmET. Too bad nonfarm was delayed by the government shutdown until next Wednesday, otherwise he might have been looked to for a reaction.

BoC’s Macklem Emphasizes the Supply Side, Beseeches Firms to Rise to the Occasion

Bank of Canada Governor Macklem’s speech yesterday didn’t materially impact markets or offer new information to a policy rate forecast. Nevertheless, it’s worth reading as it more clearly enunciates the BoC’s views on the uncertainty surrounding the future direction of the policy rate by doing a better job than previously of explaining the dance between demand and supply.

Key were the two following passages.

"We have to be careful not to misdiagnose economic weakness. Monetary policy should not try to compensate for lost supply. Lowering interest rates in the face of weak economic activity risks stoking future inflation if the weakness is due to lower productive capacity rather than a cyclical downturn in demand. And there is also a risk that overstimulating demand when the problem is structural could delay needed structural change."

and

"Second, by its nature, structural change will affect different sectors and workers differently. We can’t just look at the average impacts. US tariffs are already hitting the economy very unevenly. AI is poised to disrupt some industries and occupations more than others. Experience has taught us that these sectoral differences are important to understand inflation. For example, strong demand in some sectors may boost inflation by more than weakness elsewhere lowers it."

Overall, the speech is basically a primer on supply and demand 101 that constantly—in differing ways—reinforces the point that demand variables are likely to be on the soft side with some growth but monetary policy has to also consider the structural and cyclical factors that are restraining the supply side. That's a point that still gets lost in a lot of dialogue despite having just gone through the granddaddy of all supply side shocks.

Macklem also took a subtle poke at businesses in Canada, beseeching them to "lean into" structural change. If the economy fails to restructure by adopting new tech, pursuing new markets and products and investing then:

"…productivity and GDP growth do not recover. Canada becomes a less attractive place to invest. Businesses become less competitive. Job and wage growth are weak, our incomes don't recover, and affordability worsens. That's what we really can't afford. That's why we need to lean into this structural change."

Good for you, Governor. This is kind of a different but complementary angle to what I argued back here. Too many Canadian businesses always say it's too uncertain and risky to invest, so they don't. Some do, but Canada lags way back on the capital stock share of GDP, on R&D rankings, on adopting new tech etc.

I don't subscribe to CUSMA/USMCA falling to pieces. Further, the tariff shock is commonly overstated. Almost 90% of US-bound Canadian exports are tariff free according to US Customs data itself. USDCAD is about 1.37 from 1.20 coming out of the pandemic with about a zero real cost of short-term borrowing, and a low cost to longer term financing. Relative tariffs favour Canada over America's other trade partners. The lion's share of Canadian exporters have seen an improvement in their terms of trade and financing conditions. What do you want, a silver platter to go with it?

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.