ON DECK FOR THURSDAY, FEBRUARY 5TH

KEY POINTS:

- Gilts rally, sterling slides on dovish BoE guidance

- ECB, Banxico to hold

- US job cuts soared in January while hiring activity vapourized

- US job openings may increase in today’s JOLTS reading; claims also on tap

- German factories are crushing it

- BoC's Macklem to speak

- Mag7 Cap-ex — Boon or Bane to the US economy?

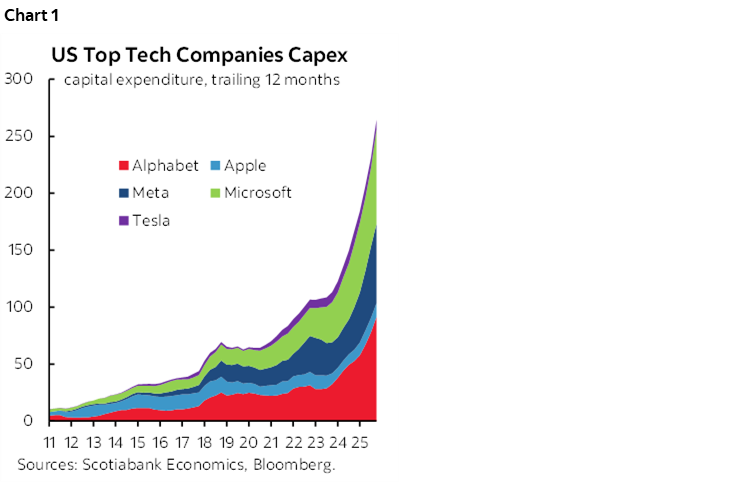

More tech earnings, BoC’s Macklem, US job market readings, and three central bank decisions lie ahead. Alphabet’s earnings beat, but heavy cap-ex is increasingly being questioned by markets in relation to return expectations.

MAG7 CAP-EX — BOON OR BANE?

Enter chart 1 that shows what five of the Mag7 are spending on cap-ex up to the end of 2025 since we don’t have Amazon and Nvidia yet. If we added the latter two up to Q3 of last year, then the Mag7 would be spending almost US$360B/year on cap-ex and adding Amazon’s and Nvidia’s Q4 tally is sure to push this significantly higher.

The numbers are poised to get a lot bigger this year; Alphabet’s US$91billion last year is guided to rise to as much as US$185 billion in 2026. Think about this. Doubling their cap-ex budget means that one single company could spend more on cap-ex this year than the GDP of six out of 10 Canadian provinces while equalling well over half of the GDP of each of the third and fourth largest provinces of BC and Alberta. By comparison to US states, Alphabet’s targeted AI cap-ex budget this year could exceed the annual GDP of 40% of US states.

Pending Amazon’s and Nvidia’s numbers, consensus estimates point to 2026 cap-ex guidance from the Mag7 totalling about US$540 billion from about $400B or more last year.

If this year’s total cap-ex exceeds half-a-trillion USD which is likely to be sharply exceeded, then the Mag7’s cap-ex could exceed the GDP of all but the top dozen or so US states and the annual GDP of every single Canadian province except for Ontario.

We’d all better hope that the tech bros find a way to make an awful lot of money with an awful lot of multiplier effects across the economy out of an awful lot of cap-ex . This could be a boon to the US economy if it persists and ripples throughout.

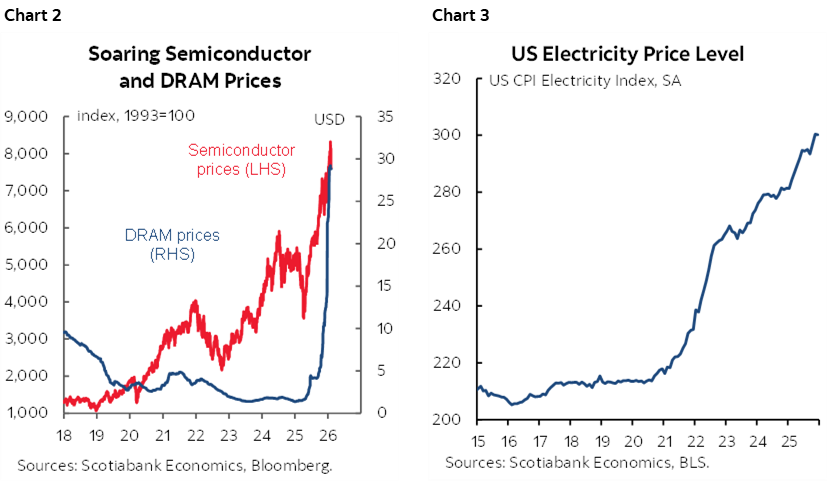

It could also become a bane to the US economy should it soften as it’s the only game in town holding up US investment activity that is otherwise trending lower. The only game in town that is driving semiconductor and DRAM prices through the roof (chart 2). Electricity prices too (chart 3). And they say AI is disinflationary.... Perhaps ultimately, although views on this becoming the case are largely speculative and highly uncertain. In the meantime, we’re left with the immediate consequences of driving key prices higher and with coming spillover effects into the broader economy.

Your turn, Amazon, that releases Q4 earnings and guidance including on cap-ex in today’s after-market (Q4 EPS US$1.96).

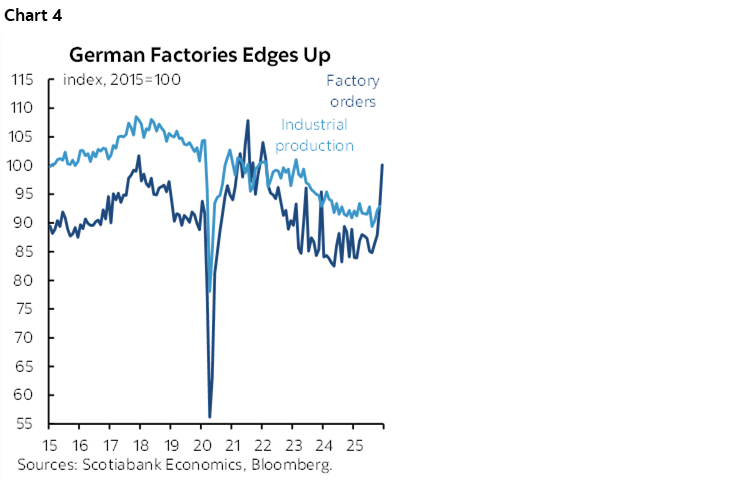

German Factories are Crushing It

Overnight data was light. German factory orders utterly crushed consensus by posting a 7.8% m/m SA gain in December (-2.2% consensus), adding to the prior 5.7% jump in November. Let's see tomorrow's factory output and exports. Chart 4 shows the stunning ascent of German cap-ex orders which I suspect is at least partly tied to the US AI-driven cap-ex boom.

French factories are not doing as well. Output fell by -0.7% m/m SA in December (consensus +0.2%) after a roughly flat prior reading.

BoE Guidance Drives Strong Easing Bets

A trio of central bank holds is expected to hold. The Bank of England already announced it held Bank Rate at 3.75% which surprised…..absolutely no one! What did surprise markets was dovish inflation guidance with the comment that inflation persistence is “less pronounced” and that the policy rate is “likely to be reduced further.” As a result, gilts are rallying across the front-end and outperforming all other global benchmarks this morning while sterling is underperforming all major crosses. Markets now lean a little closer to another 50bps of cuts this year.

ECB and Banxico to Hold

Also on tap are decisions from the ECB (8:15amET statement, presser 8:45amET) and Banxico (2pmET) today. Previews are in my weekly.

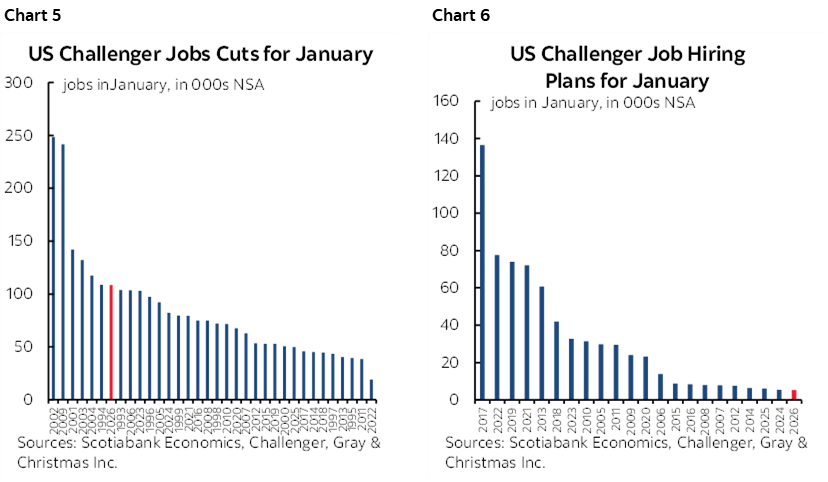

US Layoffs Soared in January

Challenger job layoffs soared to 108.4k in January which is much more than the lumpy announcements from UPS (30k), Amazon (16k) and Dow (4.5k). This is the highest total for monthly layoffs since October’s surge that was driven by DOGE cuts and tech. Charts 5 & 6 compare months of January (since it’s not seasonally adjusted) across the years for both cuts and hiring. Cuts are not the highest for a January but higher than average, but hiring activity vapourized last month compared to like months of January in history.

US JOLTS job openings (10amET) were delayed by the mini shutdown but I’m tracking a rise for today's figure.

BoC’s Macklem to Speak

BoC Governor Macklem talks about “Structural Change — Canada at a crossroads.” The speech will be released at 12:25pmET at which point headlines will scroll. There will be a moderated Q&A and then a 2pmET press conference. This is Macklem-goes-Roady to pitch last week’s narrative in customary fashion so I don’t expect much of anything new. Since their communications a week ago we’ve only taken down monthly GDP and Warsh’s appointment and light other global data and developments. Recall he said that they can neither judge whether the next move will be down or up as one example of the long pause.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.