ON DECK FOR WEDNESDAY, FEBRUARY 4TH

KEY POINTS:

- Crypto keeps tumbling

- US shutdown ends, watch for a nonfarm release date

- Jobs and wages push back RBNZ hike pricing

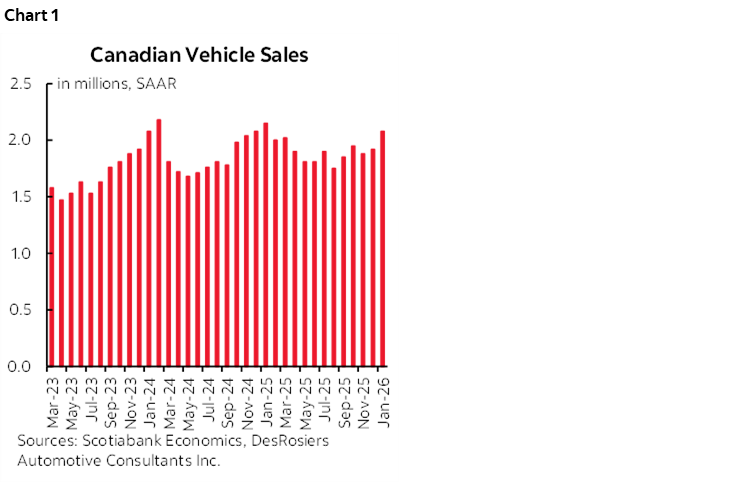

- Canadian auto sales surge to highest in a year, retail sales looking up…

- ...as Canadian jobs, auto sales, housing starts outperform the US

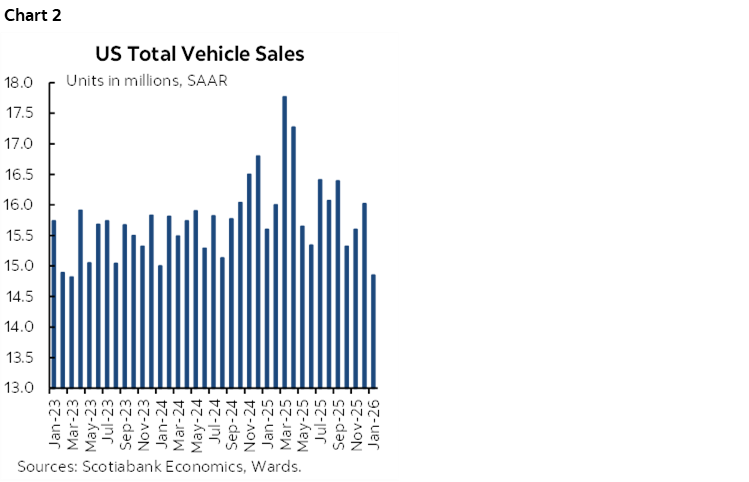

- US auto sales plummet

- US ISM-services, ADP, quarterly refunding on tap

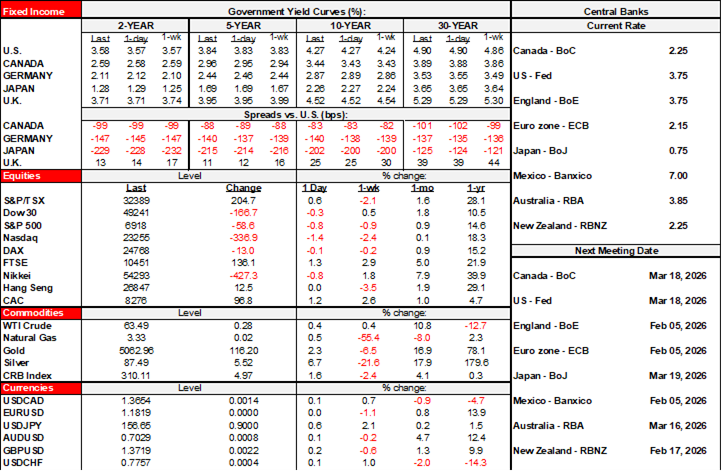

Markets are starting off in mildly constructive fashion on balance. N.A. equity futures and most European cash markets are pushing higher especially in Europe. The dollar is firmer against most crosses. Sovereign bonds are little changed with slight outperformance across the Eurozone following minor negative PMI revisions and a tick lower core than expected CPI reading (2.2% y/y). Crypto currencies continue to decline this morning and Tether’s (a stablecoin) necessary parity to the dollar continues to be under pressure. Today brings US data and more tech earnings in the after-market (Alphabet, Q4 consensus EPS US$2.65) after last evening’s US and Canadian vehicle sales prints that continue to diverge.

Geopolitical risk may flare at any moment depending upon how the Trump administration reacts to Iran’s attacks on US ships and how talks proceed. Human rights groups are reporting horrifying numbers of protesters having been killed. US naval forces are gathered offshore. Neither side may fully grasp the consequences of escalation.

Assuming Trump signs into law the funding bill that reopens the government, we might get a revised date for nonfarm payrolls very quickly. Workers are likely to be ordered back to work today. I doubt Friday is back on, but early next week could be.

Life Support is Highly Underrated

Canadian vehicle sales soared to about 2.09 million units at a seasonally adjusted and annualized pace in January which is the highest tally since last January and a gain of around 9% m/m SA (here). Sales continue to trend around multi-year highs (chart 1). Backed by job growth that leads the world.

There is never any one measure of auto sales in Canada that aligns well with how they are captured in retail sales, but all else equal, this may lean toward a solid reading for total retail sales in January. Recall that retail sales volumes were up by 1.1% m/m in November, then dipped based on preliminary guidance for December, and they appear to be gaining again in January. This kind of auto sales surge could add

I guess if you call that being on life support which seems to be the glam narrative du jour, then clearly life support’s highly underrated. Relative GDP doesn’t tell all especially given massive inventory and trade distortions through bouts of tariff front-running and consolidation episodes. Look at the relative performance of Canadian versus US jobs, or Canadian versus US vehicle sales, or Canadian versus US housing starts and it seems the tariff boomerang returned to smack the US.

US Vehicle Sales Are Tumbling

US vehicle sales landed at 14.85 million SAAR in January (15.2 consensus, 14.8 Scotia, 16.02 prior) for a -7.3% m/m SA drop. That's the lowest sales reading since March 2023 (chart 2). The smoothed trend has been pointed downward ever since the temporary peak in March when consumers tried to get ahead of tariffs. A combination of tariffs, expired EV subsidies in September, and recently lousy weather have driven auto sales lower.

RBNZ Not About to Follow the RBA Anytime Soon

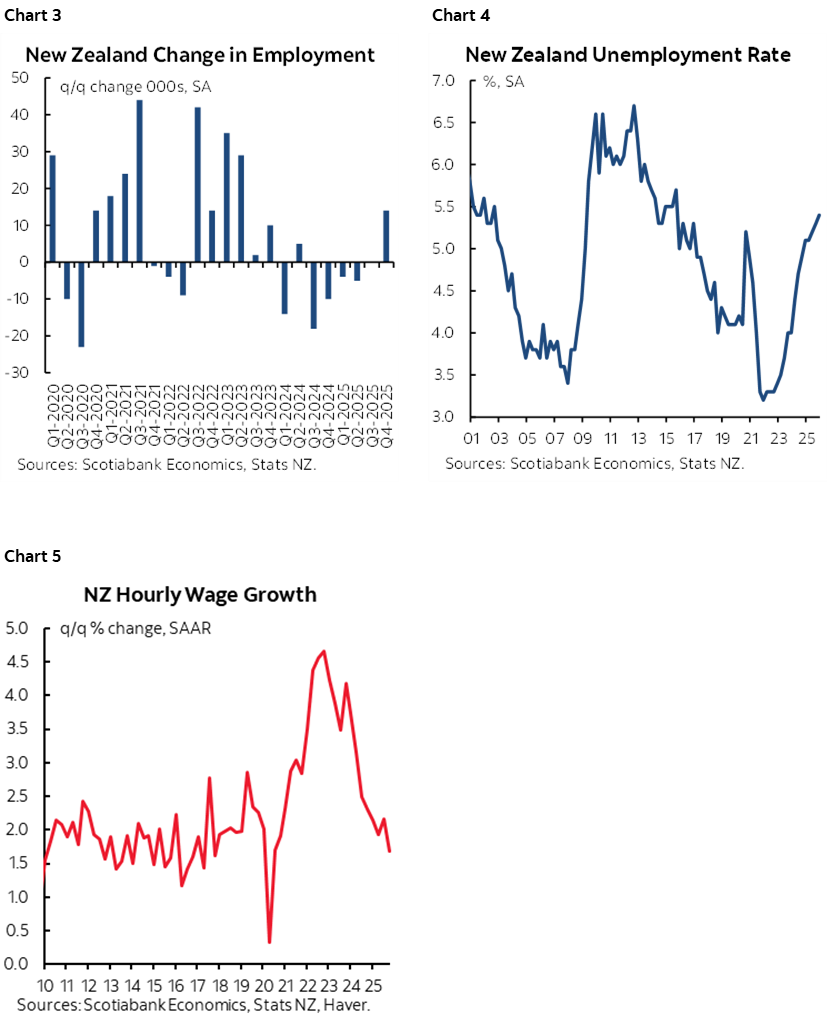

If the labour market calls the shots, then don’t expect the RBNZ to rapidly follow the RBA on a hiking path. NZ’s 2-year yield fell by about 4bps after updates. NZ jobs were up by 0.5% q/q SA in Q4 (0.3% consensus) which translated into a decent gain in employment (chart 3) but the participation rate’s rise to 70.5% helped to push the unemployment rate up a tick to 5.4% (chart 4). Wage growth excluding overtime was up 0.4% q/q SA (0.5% prior and consensus) which slowed somewhat as shown in chart 5.

US ADP, ISM-Services On Tap

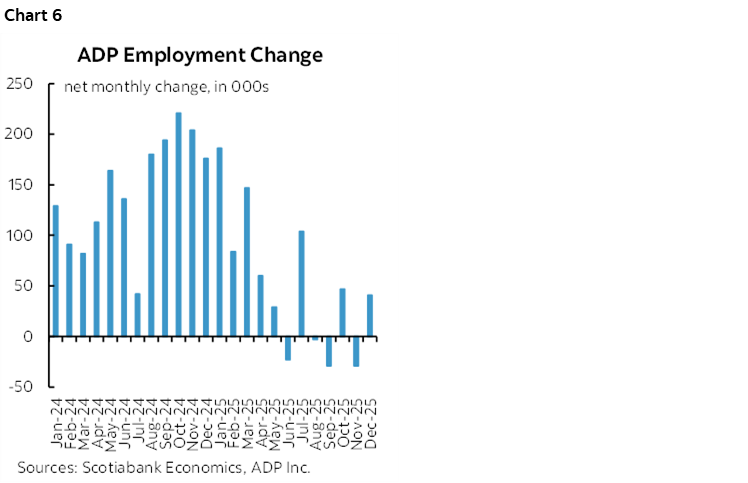

US ADP private payrolls (8:15amET) are likely to expand with consensus at 45k and Scotia at 35k based on the available 4-week rolling weekly average of changes. Meh, it’s a poor nonfarm guide, but the lost trend momentum over the past year reinforces the nonfarm readings (chart 6).

Then ISM-services (10amET) will be looked to for signs it reinforces or contradicts the signal from the much smaller manufacturing sector this past Monday.

The Treasury market will also consider the Treasury quarterly refunding announcement this morning (8:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.