ON DECK FOR TUESDAY, FEBRUARY 3RD

KEY POINTS:

- Gold up, Australian markets react to hike

- RBA hikes with a hawkish bias

- Markets paid too much attention to ISM-manufacturing…

- ...that may be signalling a new phase of the inflation cycle

- Other light overnight developments

- US, Canadian vehicle sales on tap

- US government shutdown-induced data casualties start today

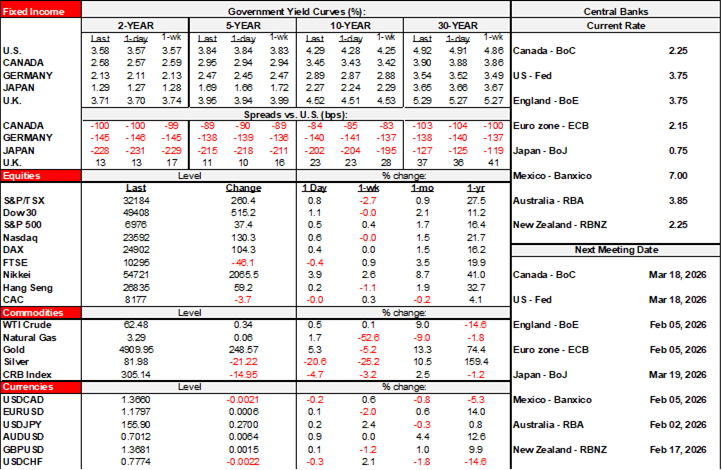

Most of the action across global markets occurred Down Under after the RBA hiked with a fairly hawkish bias (see below). Australian bonds are underperforming other global benchmarks with milder cheapening occurring in Japan and South Korea. Gold is up by nearly 6% as scavengers pick at it. Crypto currencies are playing some defence this morning. Fiat currencies are mixed with the Antipodeans leading the gainers while CAD, the euro and sterling are flat to the dollar and the yen is slightly softer. Equities are little changed on balance, with slight gains across N.A. futures are a mixture of smalls gains and losses in Europe.

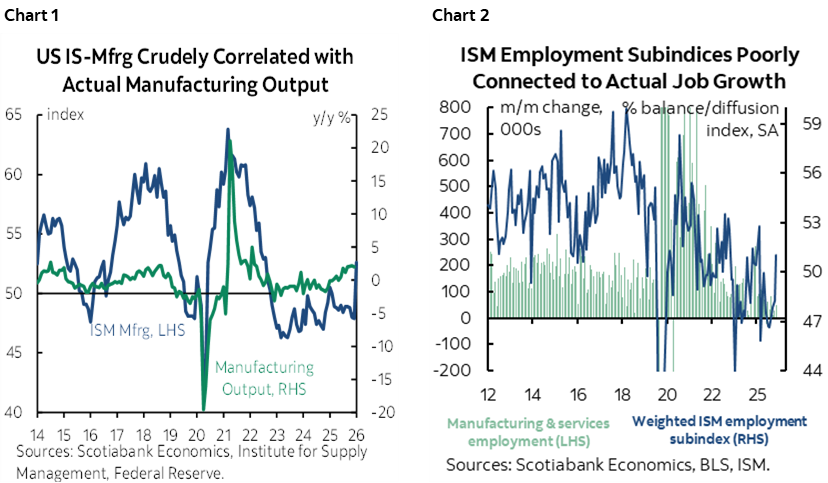

MARKETS PAID EXCESS ATTENTION TO ISM-MANUFACTURING

Yesterday’s spike in US Treasury yields was partly driven by excessive faith in the usefulness of ISM-manufacturing as a predictor of the actual economy after it surprised higher than expected. First off, manufacturing is a small part of the US economy. Secondly, charts 1 and 2 make the point about poor connections with hard data on manufacturing jobs and manufacturing output. ISM has the advantage of being timelier than actual data, but it’s soft data that reflects the opinions of purchasing managers who are closer to some decisions than others.

Further, the ISM folks noted that “A number of comments, however, mentioned post-holiday replenishment and customers’ desire to get ahead of additional tariff-driven price increases as possible reasons for the increase." That suggests that gains in new orders may not be long lived. Pair this with the comment that manufacturers broadly indicated that inventories are “too low.” This means that we may be shaking off the ability to smooth out tariff-induced price hikes through selling down inventories at old prices and transitioning to a new environment in which new orders and inventory replenishing are occurring in a context of higher prices. Let’s see ISM-services on Wednesday and then we can update the weighted price measures as a leading gauge of higher future inflation.

RBA HIKES WITH A HAWKISH BIAS

The RBA hiked 25bps to a new cash rate target of 3.85% last evening. The move was mostly but not entirely expected and the bias sounded rather hawkish. As a result, the Australian dollar is the strongest performer among major crosses this morning and the Australia government bond yield curve is bear flattening with 2s up 7bps and 10s up 2bps. At one point the 2s yield was up 10bps but settled down during the press conference when Governor Bullock sounded a little more cautious on the bias.

The decision to hike was unanimous. Bullock noted there was no discussion of a larger hike at this meeting. The economy was judged to be in excess demand and more so than at prior meetings with ongoing tightness in the job market. Key was the remark that “Uncertainty in the global economy remains significant but so far there has been little or no depressing effect on the Australian economy; indeed, recent growth and trade in Australia’s major trading partners has surprised on the upside.”

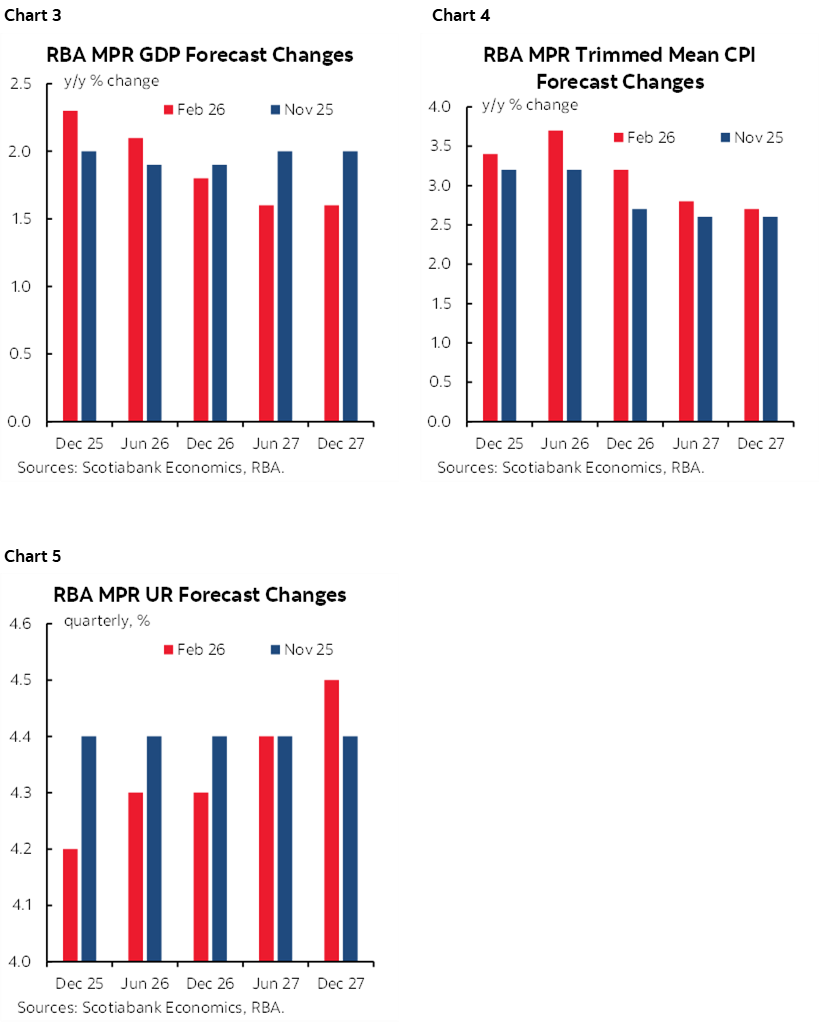

Forecast changes reflected a combination of encouragement in the near term and more binding effects of tighter monetary policy over the medium-term which likely embodies an assumed further tightening path. Compare the current forecast here to the previous one in November here and in charts 3–5. The way the RBA captures this is to incorporate market expectations of policy rate with some methodological changes that were made to how that’s done this time; the result is that the forecasts assumed the cash rate will rise to about 4 ¼% by the end of the year and then flat line, versus 3.3% previously. The growth forecast was raised to 2.1% y/y to mid-year (1.9% previously) and lowered thereafter toward 1.6% through 2027–28 (2.0% previously) presumably as the effects of a tightening bias work through. The core inflation forecast was raised by half a point throughout 2026 to end at 3.2% y/y and raised a tick to 2.7% by the end of 2027. Wage growth is forecast to remain around 3.1% y/y through most of the forecast horizon, up a tick from previously. The unemployment rate forecast was raised slightly to end 2027 at 4.5%, up from 4.4% previously.

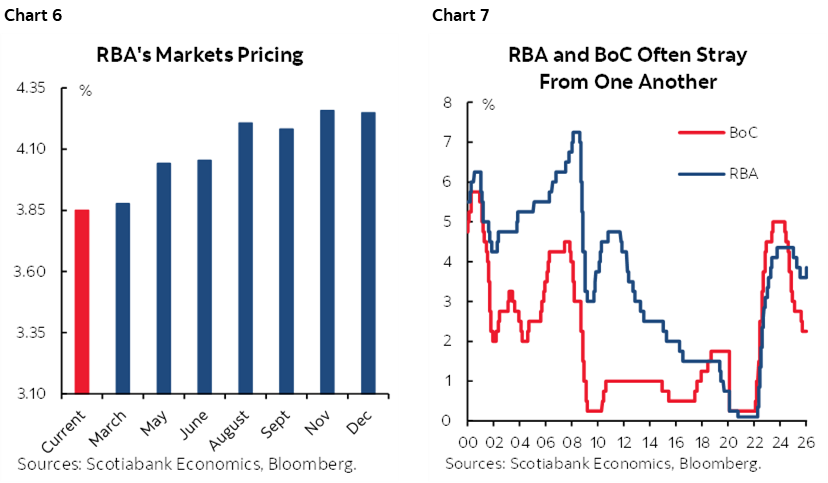

The press conference emphasized that inflation is too warm and persistent and if this continues, then further tightening may be required. Still, Bullock said she didn’t know if this was a tightening cycle per se and that she didn’t wish to commit to future moves. With markets pricing up to two more hikes this year it’s likely that the RBA delivers on further tightening as opposed to easing financial conditions that would be counter to its overall revised forecasts. One hike alone does nothing to the economy.

What happened in Australia generally stayed in Australia with little spillover effect into other markets. Even neighbouring New Zealand’s bond market went the other way with mildly lower yields overnight. There is no spillover effect into Canada and be careful with casual linkages as markets price further RBA hikes (chart 6). Chart 7 shows that the policy rate spread can be very wide at times as the central banks pursue different paths, but there are notable instances when the direction of moves coincided. Eventually we expect the BoC’s next move to be up, but not for quite some time.

OTHER LIGHT OVERNIGHT DEVELOPMENTS

Other overnight developments were light. French CPI was weaker than expected (-0.4% m/m, consensus -0.2%) but was ignored as some countries have already released and confirmed expectations for a weak Eurozone tally tomorrow ahead of nothing being expected from the ECB on Thursday. South Korean inflation met expectations at 2% y/y and 0.4% m/m but core inflation was a tick above consensus at 2% y/y. Combined with the RBA’s hike, the effect was to push short-term Korean yields a little higher. Turkish inflation surprised a little higher at 4.8% m/m (4.3% consensus) and 30.7% y/y (30% consensus).

MY FRIDAY GOT A LITTLE EASIER FOR THE WRONG REASON

A light N.A. calendar lies ahead. We were to have received the JOLTS job vacancies reports for December this morning but it’s the first casualty of another US government shutdown. The next casualty will be initial claims (Thursday) and then Friday’s nonfarm payrolls report has been delayed until the government re-opens and a new release date can be set. The suspended US payrolls report will mean a cleaner read on Canada’s jobs numbers, where the government remains open!

So in the meantime, we’re left with vehicle sales figures from Canada and the US. The US releases by the end of the day with a combination of industry guidance for the first half of January and crippling snowstorms over late January expected to drive sales sharply lower (consensus 15.2 million SAAR, Scotia 14.8, prior 16.02). Canada’s sales figures may be released at some point today.

Also watch for more Fed-speak from Richmond Fed President Barkin (8amET) and Governor Bowman (9:40amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.