ON DECK FOR FRIDAY, FEBRUARY 27TH

KEY POINTS :

- Markets seeking safe harbours to end the week

- Iran tensions driving oil futures higher

- The BoC may well yawn at Canadian GDP

- US producer prices to inform Fed’s preferred inflation gauge

- Eurozone CPI tracking softer than expected

- Japanese core inflation hits four-month high

Happy Friday! Unless you’re trading US equities this morning in which case my sympathies. US stock futures are gently lower by about ½%, TSX futures are slightly lower, and European benchmarks are flat on average. There is a safe haven bid into sovereign bonds across the US and Europe but it’s small. This is despite oil futures being up by about 2% partly as pressure on Iran builds into what could be a pivotal week; the US ambassador to Israel advised embassy workers to leave “TODAY” with his emphasis upon caps.

Overnight releases were neither here nor there in terms of market significance but included generally soft Eurozone inflation versus hotter Japanese inflation than some of the coverage indicated.

Canada updates GDP figures today which may provoke a yawn from the BoC, with the US updating producer prices to inform inflation risk.

TRACKING CANADA’S ECONOMY

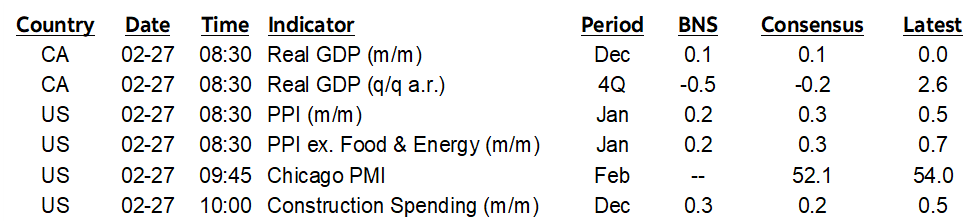

Canada gets a trio of GDP readings this morning (8:30amET). Key will be how it relates to the BoC’s expectations for 0% Q4 growth and a 1.8% rebound in Q1.

Q4 GDP is expected to be soft with consensus at -0.2% q/q SA, Scotia at -0.5%, and estimates ranging from a low of -0.9% to a high of +0.5%. That would follow the trade-influenced surge in Q3 (chart 1). Details will matter in terms of drivers like underlying momentum in the domestic economy reflected in final domestic demand and particularly the consumption and investment components. Government and net international trade are expected to be positive drivers. There are likely to be upward revisions to trade contributions to Q3 growth given data since the estimates were offered, but it’s uncertain how this could affect other GDP components like inventories.

GDP for the month of December is expected to be up by 0.1% m/m SA based on Statcan’s preliminary ‘flash’ reading of about a month ago. That would extend a soft trend as two of the prior four months were down and one was flat.

The preliminary estimate for January GDP will help to inform early tracking for Q1 GDP growth when combined with how 2025 ended. We have little to go by in terms of advance readings.

Little impact on BoC thinking is expected from these readings given Governor Macklem’s message of general patience, but he’ll have an opportunity to comment on the figures next week.

US PPI TO INFORM FED’S PREFERRED INFLATION GAUGE

On deck for the US is the January reading for producer prices (8:30amET). Recall that the prior month’s strong 0.7% m/m SA rise (0.3% consensus) spooked markets about supply chain inflation pressures that may pass through to consumers. Most expect a reading of about 0.3% this time around. Select components will be used to firm up expectations for the Fed’s preferred PCE inflation reading that isn’t due out until March 13th given the ongoing data backlogs from the government shutdown.

EUROZONE INFLATION TRACKING LOWER THAN EXPECTED

German inflation acted as a downward weight against upside surprises from France and Spain ahead of next Tuesday’s Eurozone tally when Italy also releases. Consensus went into the releases thinking the Eurozone tally would be up by 0.5% m/m which now looks too high. None of it mattered as there is slight richening across sovereign bonds in Europe and elsewhere and expectations for a prolonged hold by the ECB remain intact.

- Germany’s national print arrives at 8amET, but the individual states registered two readings of 0.4% m/m, one at 0.3%, and three at 0.2% which likely provides a weighted average well below consensus expectations for 0.5% on the add-up.

- France registered a CPI change of 0.8% (0.5% consensus).

- Spain’s EU-harmonized reading was 0.4% m/m (0.3% consensus).

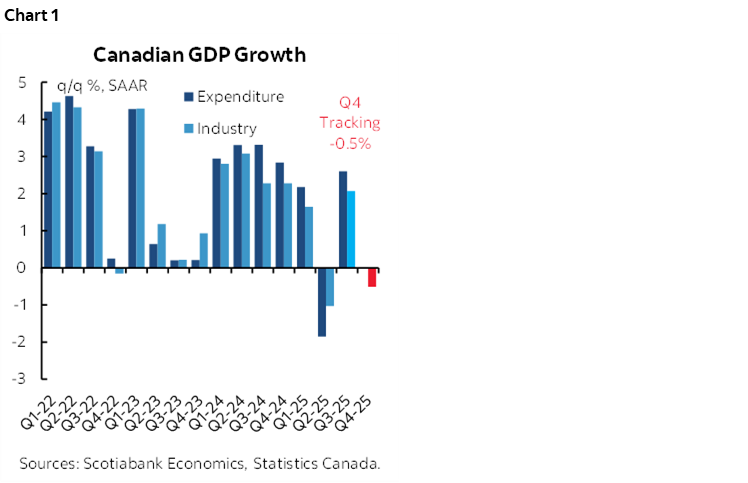

TOKYO CORE INFLATION ACCELERATES

JGB bond yields rallied in bull flattener fashion despite firmer inflation figures. The fresh Tokyo core CPI reading for February was up by 3.7% m/m at a seasonally adjusted and annualized rate for the hottest print since October (chart 2). The year-over-year core inflation rate fell back to 1.8% (2% prior) excluding only food as per the Japanese convention, but ex-food and energy it accelerated to 2.5% (2.4% prior).

What probably dented the reaction to CPI was a mixed set of macro readings. Retail sales soared by 4.1% m/m (1.5% consensus), but industrial output grew 2.2% m/m (5.5% consensus). Both numbers were nevertheless quite strong.

OTHER MACRO

Why is Canadian PM Mark Carney off to India? Here’s a hint—GDP was up 7.8% y/y (7.6% consensus) as the economy remains one of the hottest on the planet. That’s great, but Canada would get more of a lift from trade liberalization within its own country than anything a trade deal with India could offer.

French consumers were in a spending mood as inflation-adjusted spending climbed by 0.5% m/m SA during January but after two months of small declines through the holiday season.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.