ON DECK FOR THURSDAY, FEBRUARY 26TH

- Global markets little changed

- US continuing claims point to lower UR

- Canadian small businesses are feeling rather good these days

- Canada’s unreliable payrolls report

- Alberta’s budget to spill a little more red ink

- All ‘big six’ Canadian banks beat expectations

- BoK holds and guides an extended pause

- USTR demands on Canada — Keep calm, we’ve seen this movie

- What Canada’s #1 demand in trade negotiations should be

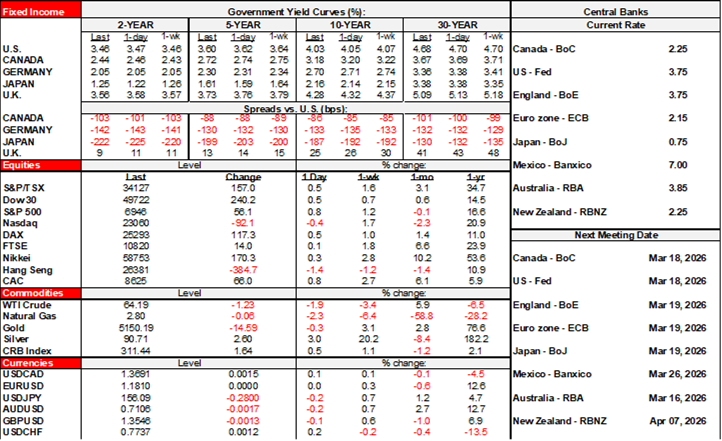

Markets are mixed in the absence of fresh unifying catalysts. US equity futures are little changed following Nvidia’s earnings release in yesterday’s after-market that somehow turned an overwhelming set of beats into scepticism about the future. Canadian futures are slightly in the red despite three more bank earnings beats. European stocks are mostly up. Sovereign bond yields are marked by very slight outperformance across gilts and Canada bonds plus Down Under, with slight underperformance across JGBs. The dollar is a touch stronger except against the yen as JGB yields slightly retraced the prior day’s rally.

CANADIAN BANKS ALL BEAT

Every one of the ‘big six’ Canadian banks beat expectations for earnings per share but with mixed details and market exposures. This morning started with CIBC beating with adjusted EPS of C$2.76 (consensus $2.38). Then RBC beat expectations with adjusted EPS of $4.08 (consensus $3.84). Last out was TD Bank that also beat with adjusted EPS of C$2.44 (consensus $2.25). They add to prior beats by BNS (my employer) and BMO.

LIGHT N.A. DATA

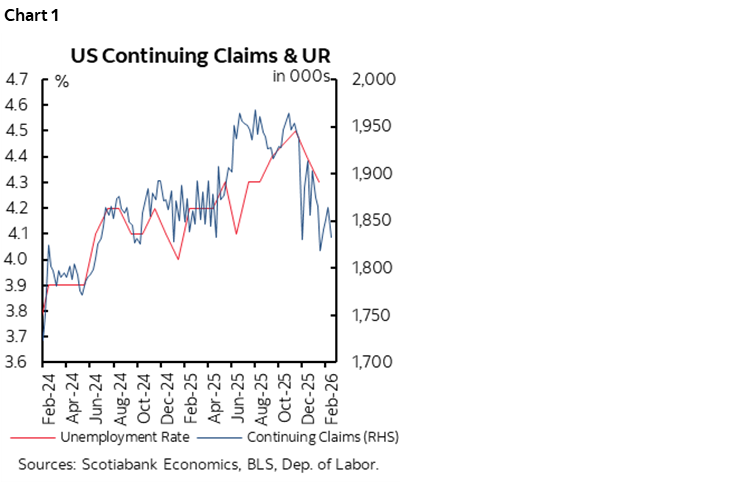

US initial jobless claims were little changed last week (212k, 208k prior) and continuing claims eased lower to 1.83 million from 1.86. The are the conclusion of the reporting through the nonfarm reference period and household survey reference week ahead of next Friday’s job market readings. The continuing claims trend suggests a downtick in next week’s US unemployment rate for February (chart 1).

Canada refreshed the lagging and unreliable payrolls survey for December and payroll jobs fell by 35k. (8:30amET). That contrasts with the Labour Force Survey’s +3.9k rise in payrolls that month (and +10k for total jobs). The payrolls survey is too lagging to matter as we’ll get the more complete February LFS report on March 13th. It’s also subject to wickedly high revision risk every month versus annual benchmarking revisions to the LFS survey. Chart 2 shows how much SEPH gets revised on the first revision and there can be further revisions to every month. #unreliable.

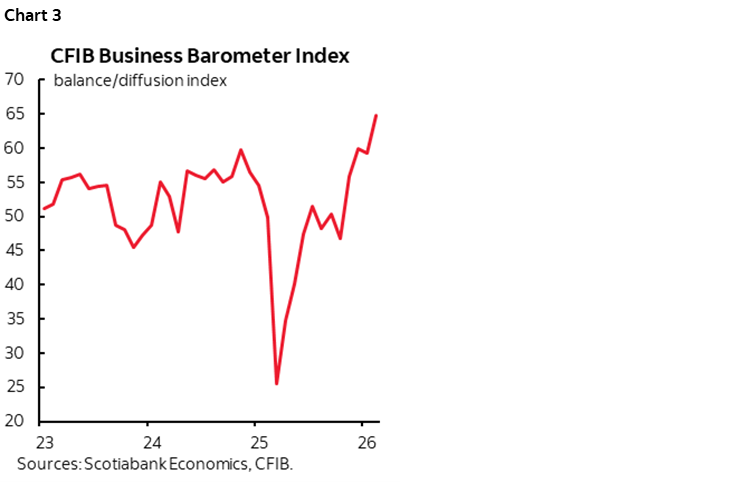

Chart 3 shows exploding business optimism among Canadian small businesses according to the February reading from the folks at the Canadian Federation of Independent Business. On net, they plan on increasing staffing, and raising prices and wages by a little more than the BoC’s 2% inflation target. Smaller businesses have less direct exposure to tradeables and hence tariffs. Also don’t forget that about 75% of Canada’s economy is in services that are not immune to trade risks but better insulated than more export-oriented goods.

ALBERTA’S BUDGET TO SPILL MORE RED INK

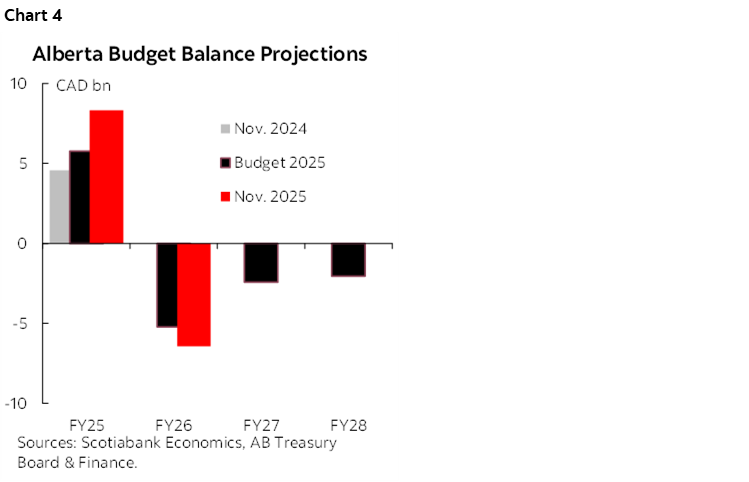

Alberta will release its 2026–27 budget at around 5:15pmET this afternoon. Mitch Villeneuve will be covering it and shares his thoughts in what follows. While the province recorded a sizeable surplus of $8.3 bn (1.8% of GDP) in 2024–25, lower oil prices and higher spending on health and education have pushed the province into the red this year. Alberta’s mid-year update estimated a deficit of $6.4 bn for 2025–26, up from the initial estimate of $5.2 bn in Budget 2025 (chart 4).

Budget 2026 is likely to increase projected deficits further—especially for future years, given that oil prices trended lower rather than the expected higher over most of the past year (though a narrower WTI-WCS differential is providing an offset). The Premier of Alberta has warned people to “brace themselves” for deficits in this budget, and over the last week the government has announced that the budget will include a 22% increase ($1.4 bn) in pay for doctors and a 7% increase in education funding ($0.7 bn). However, the Premier has also said that there will be some spending reductions, including through cuts to “unnecessary bureaucracy” and new income testing for some benefits. She has also announced an October referendum that will seek public guidance on a variety of proposals, including limiting the access of temporary residents to the health system.

Alberta’s current fiscal rules limit the allowable 2026–27 deficit to around $7 bn and require a plan to balance the budget by 2028–29, though rules of thumb indicate that the revenue shortfalls alone could push the 2026–27 deficit to close to $10 billion. Despite the fiscal headwinds, Alberta is likely to continue to have the lowest provincial debt burden, and contingency buffers in the budget and recent increases to oil prices provide some upside risk to overperform on the deficit projections.

BOK HOLDS WITH DOVISH GUIDANCE

The Bank of Korea held its base rate unchanged at 2.5% as widely expected by consensus and markets. Neutral guidance included a central projection for no rate change over the coming six months. Stability issues remain significant with the BoK still monitoring house price gains in Seoul and spillover into household debt markets. The South Korean yield curve rallied by 6–7bps at the front-end and a little more at the longer end.

USTR DEMANDS — WE’VE SEEN THIS MOVIE BEFORE

So, US Trade Representative Jamieson Greer said yesterday that Canada will simply have to buckle to US demands and accept higher tariffs and more access to the local market by US firms. Well bully for him.

My first piece of advice to market participants is not to litigate trade negotiations on a daily basis. I get that markets need to manage trading books and portfolio positions in real time, but this horizon is fundamentally at odds with the patient nature of complex trade negotiations that evolve very gradually over time and reach a frenzied rush late in the game. It’s a long process that starts with asks aplenty and gradually migrates toward crunch time when the executive level of power makes the final decisions on what they’re prepared to live with.

Recall 1988 when Reagan and Mulroney made the key decisions leading to a deal after a prolonged stalemate held up by logjams related to unrealistic US demands. Recall 2018 when Trudeau/Freeland dug in and reached a deal with Trump in the late stages after tense negotiations amid a long wish list of demands; CUSMA/USMCA turned out to be a minor refresh of the original NAFTA agreement at least in Canada’s case and with a little more by way of changes in Mexico’s case (higher effective wage floor in autos, higher N.A. content etc).

In short, we’ve seen this movie before. It’s full of high drama, bad acting, and with significant risk of forgetting to craft a plot until one gets slapped together at the end just when the budget runs out. By ‘this’ movie I mean demanding everything from Canada including higher tariffs and more market access and giving nothing. The sequel isn’t any better than the original from about eight years ago, but we’re long past being surprised by the Trump administration’s tactics. Enter game theory in which the players learn more about each other like how there’s no real ‘art’ to the art of the deal. For that matter, we’ve seen these issues, demands and threats dating back to the 1980s with the birth of the original Canada-US Free Trade Agreement before Mexico joined and made it NAFTA. In my 3+ decade career and as a student monitoring the developments before then, I’ve always found that the only trade negotiation that matters is the one immediately before the ink hits the page.

Canada has plenty of seasoned negotiators who were around long before Mr. Greer and have dealt with these same issues over and over. So does the US. So does Mexico. They’re all sovereign nations with lots of expertise and plenty of policy options. We know that threatening higher tariffs and simultaneously demanding more access to Canada’s market while offering no concessions of your own is a pure negotiating tactic. We well remember Robert Lighthizer’s tactics. Concessions on both sides could leave consumers better off everywhere if well played, but my concern is that the US administration is subjugating the interests of its consumers to the whims of political preference and on that let’s see how voters feel about it on November 7th.

It’s called a negotiation. In a negotiation, you come in big, offer little to nothing, threaten to hold your breath until mommy gives you what you want, test your opponent’s mettle, and then eventually exhale and get on with things.

And there’s another word I’d like to introduce. It’s spelled n-o.

As in no, Canada won’t be pressed into a bad deal. As in no, it’s not true that Canada has no negotiating leverage of its own. As in no, it’s not true Canada has no demands of its own. As in no, nothing should be off the table from Canada’s standpoint. Like, oh, forget about your golden dome that a) is a flawed concept, b) easily bypassed as evidenced by Israel’s porous ‘iron dome’ or by a boat on the Hudson River, and c) extraordinarily expensive by taking the CBO’s hundreds of billions estimate and probably multiplying by 2–3 times by the time it’s operational ages from now when it won’t matter. Like forget about our critical minerals and other resources. Try coffee grounds instead of potash and see what your crop yields are like. Like how damaging Canada boomerangs right back at the US economy through tightly integrated supply chains. Like retaliatory tariff measures. Like excluding US firms from Canadian procurement as hundreds of billions—possibly trillions—get spent on defence and infrastructure. Like Gripens over F-35s for the same reason that doing one’s weekend errands doesn’t really require a Ferrari but it would be fun. Subs from the Koreans or the German-Norwegian consortium.

The one difference this time, however, is the growing evidence that US isolationism is taking its toll on the US job market that is losing jobs on a trend basis in terms of private nonfarm payrolls ex-health sector hiring, falling US investment ex-AI, US inflation, and US economy and with midterms coming. The courts are challenging tariffs and more challenges likely lie ahead. Pushing it further yet would only raise that cost into the midterms and then 2028. The economic and political cost of tariffs to the US economy and the Trump administration's sagging poll numbers should give Canada more confidence to stand firm amid the very real prospect of a lame duck US administration next January.

I’ll repeat what I said over and over throughout the last time in 2018—it’s better to be stuck with uncertainty by digging in than to sign a bad agreement you could be stuck with for decades. That was the playbook in 2018 and the playbook in 1988.

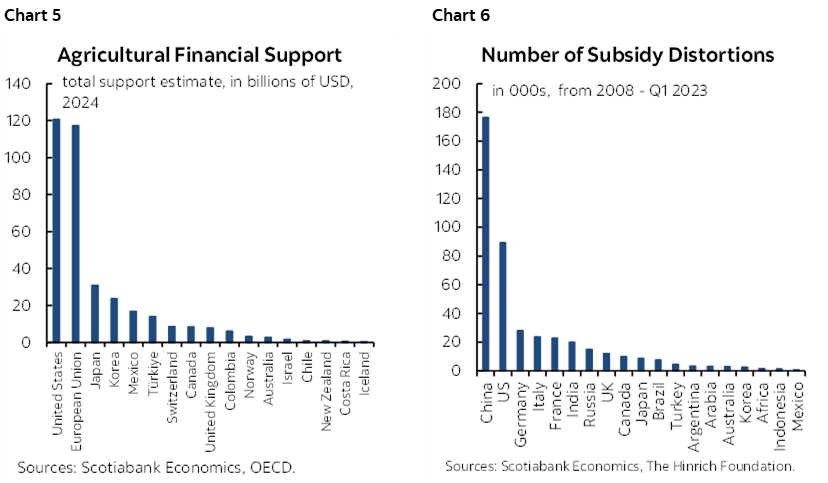

As for what Canada can demand, at the top of my list would be more effectively bringing the US addiction to subsidies into the framework. Canada’s no saint either, but the US tops the world in the use of subsidies. That’s true for agricultural subsidies (chart 5) along with the Europeans including but not limited to the hundreds of billions granted annually to rich corporate farms through the US Farm Bill as they’re not the mom-and-pop farms of the 1930s. The US is right up there with China in the number two spot for total subsidies to all businesses (chart 6).

Large US corporations get handouts in spades.

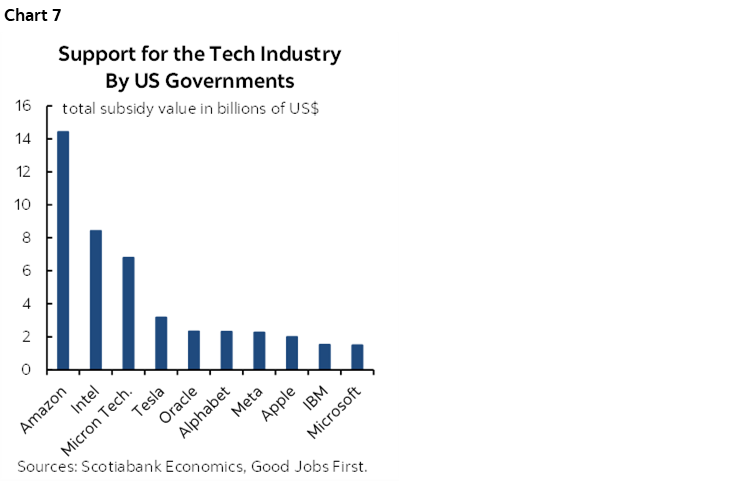

The US attracts data centers with dollops of taxpayer funded money. Chart 7 shows the massive subsidies granted to US tech firms.

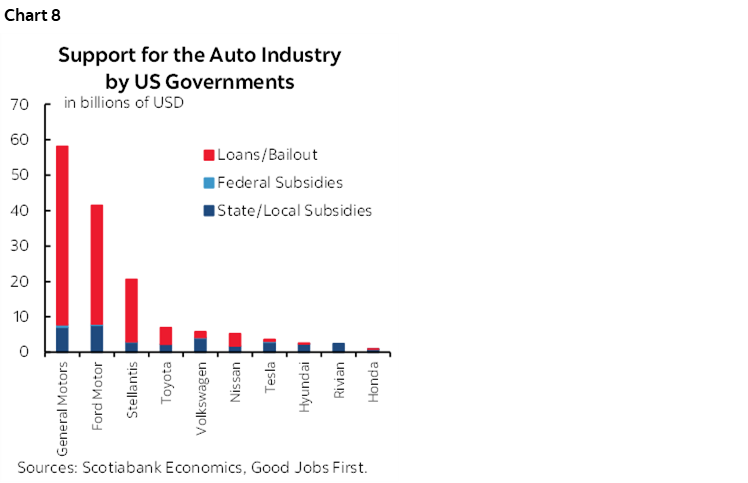

For decades the Midwest and southern states siphoned off investment from the northern US states and Canada by spending billions on subsidies to attract auto plants. Chart 8 provides one depiction of subsidies handed to auto firms. Now the US wants to pull away investment by making American firms and American consumers pay for tariffs as just another tax paid to Washington. US auto policy ripped off the northern states for decades and now the goal is to rip off US consumers; it doesn’t get better than that in terms of own goals.

Or try GFC-era bailouts.

There’s also my personal fave, the “chicken tax”, a 25% tariff on light truck imports into the US that was born out of trade disputes with France in 1964 and which exists to this day while protecting the US auto companies against competition from foreign truck makers. Again, Americans pay the price for this protectionist measure.

My second personal fave is all the subsidies granted hockey teams to locate in southern US markets. Like the allure of no state income tax in Florida for multimillionaire puck passers, or heavy subsidies to build arenas, the combined effects serving to buy talent from Canada to win Stanley Cups in the US.

The US military-industrial complex is a notorious swamp of taxpayer funded subsidies.

So is the US fossil-fuel industry with estimates pointing to a doubling of subsidies since the beginning of Trump’s first term (here).

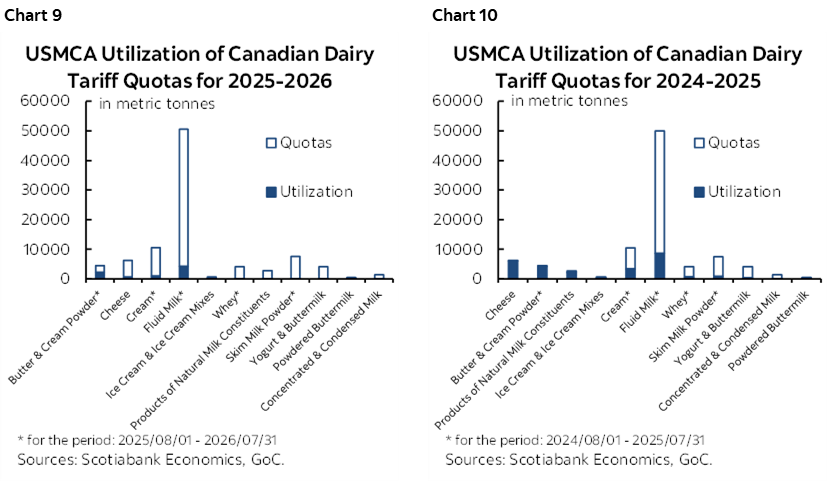

As for dairy, US producers don’t use their existing export quotas into Canada above which tariffs apply (charts 9–10) and the US has the same system!

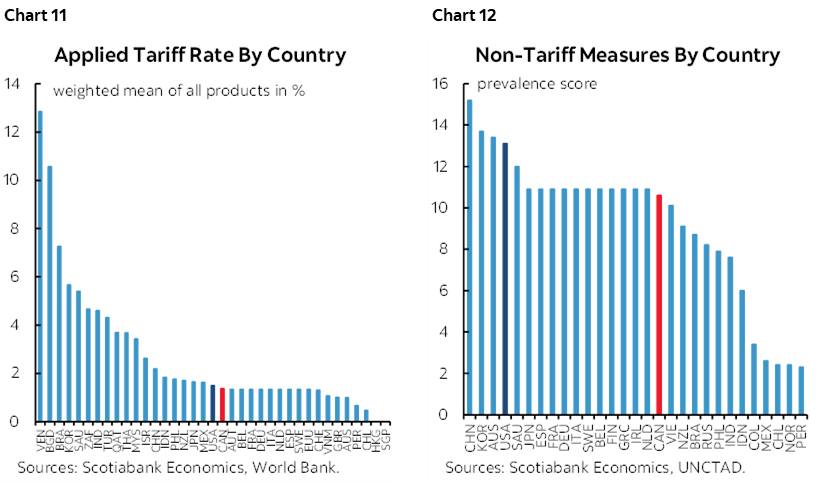

You see, the reason why developing economies use tariffs and other measures is because they don’t have the resources to play the subsidy racket the way Uncle Sam does. Canada, however, is no different from the US on tariffs (chart 11) or nontariff barriers (chart 12).

We could go on and on to include the Chips Act, the Inflation Reduction Act and other examples of subsidy frameworks employed by various administrations over time.

I admire an awful lot about the US economy. It’s innovative. Its labour market is flexible. It has deep, highly liquid, sophisticated financial markets. It doesn’t dwell on failure and instead lets bygones be bygones while moving on. It has historically had strong institutions, though this is now a more open question mark. But ring fencing a subsidy swamp with a tariff wall doesn’t serve anyone’s interests especially the interests of Americans. It’s exactly what folks like Adam Smith warned you about when commercial interests take over public policy and in the end it doesn’t serve them well either. Over time, such an approach will challenge the nimbleness of US businesses, their innovative tendencies, their cost structures, and the ultimate price for all of that would be paid for by consumers and by workers — in the US.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.