ON DECK FOR WEDNESDAY, FEBRUARY 25TH

KEY POINTS:

- BoJ interference and Nvidia dominate market focus

- Japanese long-bonds smell political interference at the BoJ

- Are PM Takaichi’s BoJ appointees still as dovish as their prior remarks?

- Nvidia’s after-market earnings could make or break tech sentiment

- Australian CPI surprised higher, boosting the A$

- BoT delivers a surprise cut

- Canadian bank earnings continue to beat

- SOTU speech: long, especially since it had nothing new…

- …but watch for ratings and updated polls alongside fact checking

Substantive matters across financial markets are concentrated upon developments at the Bank of Japan, hawkish RBA sentiment, Nvidia’s hotly anticipated earnings in today’s aftermarket (consensus EPS US$1.43), and more Canadian bank earnings beats. A steeper JGBs curve may be spilling into mild effects across other generally higher yields elsewhere with higher Australian yields driven by CPI. Equities are broadly higher across N.A. futures and European cash markets after rallies across Asia. Quite frankly, markets couldn’t care less about last evening’s long SOTU speech and while it’s a stretch, maybe that’s because they’re relieved it contained nothing new.

JAPANESE LONG BONDS SMELL POLITICAL INTERFERENCE IN THE BOJ

The yen fell again overnight and longer-term JGB yields punched higher by 5bps in 10s and 8bps in 30s after PM Takaichi appointed two dovish members to the Bank of Japan’s board. If confirmed, then they are perceived as reflationists who could thwart a hiking agenda in favour of growth while Takaichi pursues expansionary fiscal policy.

Having said that, efforts by newswires to dredge up past remarks by the new appointees seem stale and out of date which will keep markets focused upon their first chances to provide updates in the present context. It’s likely they got the appointments by confirming dovish views with Takaichi, but they could be more nuanced now. The present context is different than the 2021–23 period during which most of the quotes were delivered. Takaichi’s strong preference for expansionist fiscal policy in the wake of a landslide election victory is one such point, plus several years of strong ‘Shunto’ wage gains and greater evidence that the BoJ is achieving its 2% inflation goal.

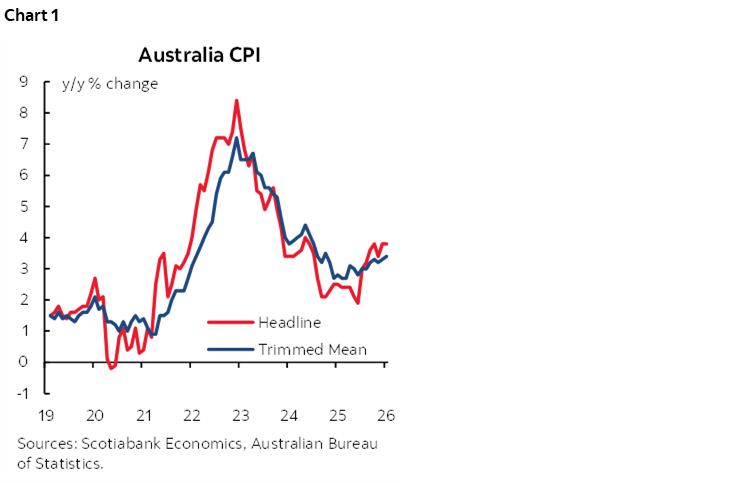

AUSTRALIAN CPI SURPRISED HIGHER, MODESTLY BOOSTING THE A$

Australian CPI surprised a bit higher and drove a modest gain by the A$ and higher local bond yields with 2s up about 4bps in a mild bear flattener. The March 17th RBA decision continues to be priced for a hold, but the May 5th decision is mostly priced for another 25bps hike that was minimally impacted by CPI.

CPI increased by 0.4% m/m and 3.8% y/y (3.7% consensus). Trimmed mean CPI was up by 0.3% m/m and 3.4% y/y, a tick above the prior reading and consensus. Chart 1.

CANADIAN BANK EARNINGS CONTINUE TO BEAT

On the heels of the earnings beat by BNS yesterday, BMO beat expectations this morning with adjusted EPS of C$3.48 ($3.22 consensus). National Bank also beat with adjusted EPS of C$3.25, consensus $2.95.

BOT DELIVERS A SURPRISE CUT

The Bank of Thailand surprised with a 25bps rate cut down to 1% by a 4–2 vote. A minority of three out of 23 within Bloomberg’s consensus got the call right.

SOTU SPEECH—LONG, EMPTY, WATCH POLLS AND RATINGS

If you missed it, then you can still watch Trump’s State of the Union speech here, or read it here. If your focus is upon gleaning fresh insights into policy leanings, then I don’t recommend it.

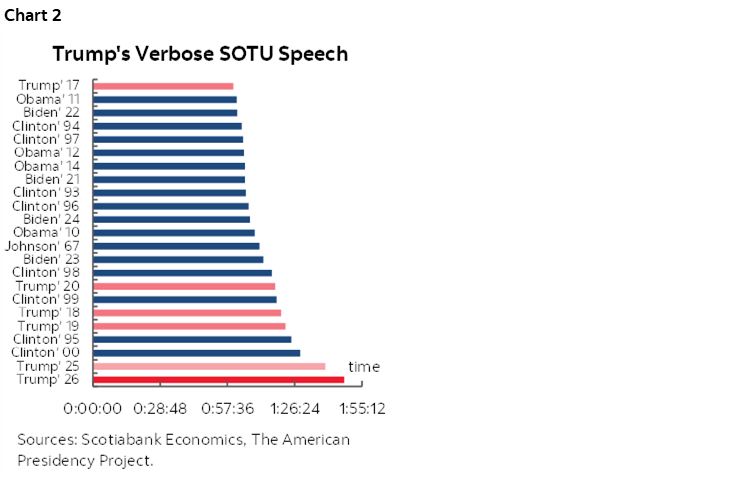

For starters, it was long. Very long. At one hour and forty-seven minutes and forty-six seconds it was the most long-winded SOTU speech ever (chart 2). In fairness, a good chunk of that time was spent on hooting and hollering and general all-around theatrics in Congress.

It was simple in terms of its prose and overall style. Mr. Trump’s speeches have been measured on the Flesch-Kincaid readability level as being at a grade 8 level. He’s not alone; this has generally been the rating assigned to SOTU speeches by all presidents from both parties since 1990 according to UCal-Berkeley. Welcome to the age of social media and/or it’s a comment on the state of the educational system.

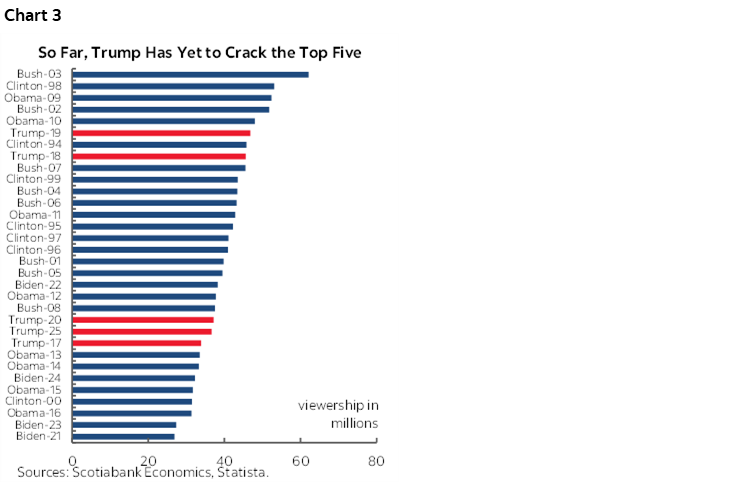

Watch TV ratings as one sign of Trump’s current draw. Trump’s SOTU speeches including last year’s sort-of SOTU speech have never cracked the top five in terms of viewership (chart 3). The record remains George W. Bush’s 62 million viewers in 2003. We’re waiting for this year’s ratings.

Be patient while watching for the polls in the wake of his speech. The first ‘flash’ polls may arrive as soon as today or tomorrow from outfits like YouGov, CNN, Morning Consult etc. They’re usually small sample polls providing instant reactions. It will take several days before we get national polls. Poll aggregators like RealClearPolitics can take 1–2 weeks to report back.

In my opinion, last night’s speech did not contain anything to improve Trump’s sagging approval rating among the folks who put him in office. The ones who did that were not die-hard Republicans, but rather the Latino vote and independents, both of whom have been turning away in droves.

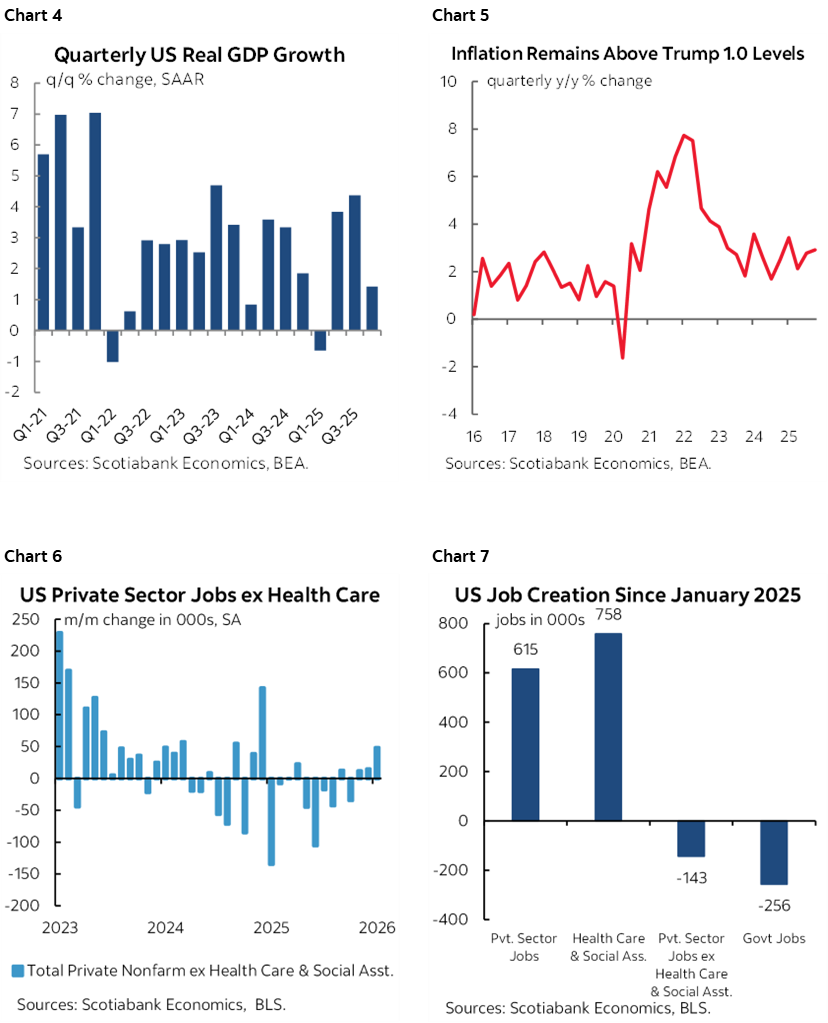

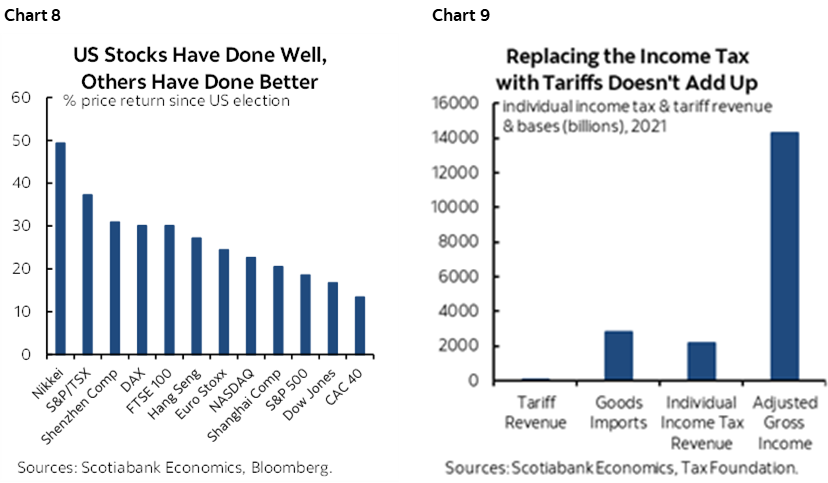

The speech was the customary fact checker’s paradise with many listeners finding it difficult to tell truth from fiction. Here’s one attempt at fact checking. Chart 4 shows that claiming Trump resuscitated an underperforming US economy is not true; growth was solid and less erratic before Trump took office. Chart 5 shows that today’s inflation under Trump 2.0 remains higher than under Trump 1.0 which contrasts with his claim the Biden administration caused the affordability problems which was partly true given expansionary fiscal policy but also in fairness heavily due to the pandemic and overly easy monetary policy for too long. Charts 6–7 show how exaggerated his claims on the health of the US job market are; it has noticeably weakened since ‘Liberation Day’ in April and the US unemployment rate is about half a percentage point higher now than in 2024. Chart 8 shows that Trump overemphasizes the strength of the US stock market since his election. Chart 9 demonstrates that Trump’s claim that tariff revenues can replace income tax revenues is just plain wrong; the massive gulf between the tax bases for tariffs versus income taxes means you’d need punishing tariff rates at which point imports would be vapourized with nothing earned. So was Trump’s claim that Congress won’t be needed to approve tariffs; they would have to approve any extension of Section 122 tariffs past 150 days (ie: beyond late July). And we could go on and on, but most folks are probably well aware that the claims often don’t line up with reality.

Trump beseeched Congress to pass the Stop Insider Trading Act that would attempt to stop members of Congress from using insider information. This could be welcome if it becomes truly effective which we’ll see about, though critics will say it could be a performative distraction from accusations that the Trump family has used the office for self-enrichment.

There was nothing material by way of fresh policy insights. Matching 401k contributions for Americans underrepresented by pensions with a $1k state contribution is small potatoes and needs legislation. There was nothing new on geopolitical matters, or tariffs. The rumour going into the speech about a new tax cut being offered fell flat as nothing was revealed. There was nothing on housing. Nothing new was said about Iran as Trump just repeated the longstanding policy across several administrations that Iran must not acquire nukes. There were no material references to China which was unusual compared to Trump’s past attacks. Nor Canada. Trump’s remarks on Mexico were confined to emphasis upon its drug wars with nothing on trade. I’ll take a big nothing burger compared to the risk that Trump’s natural leanings could have ignited unfavourable risks.

Much of the speech’s emphasis was placed on the economy and affordability. These are Trump’s weak points among voters as his popularity tumbles. My weekly (here) offered a ‘state of the union’ across many different readings and offered very preliminary comparisons of Trump 2.0 to past Presidents across multiple economic and market indicators.

Lastly, Trump teased about a third term and said that “strange things happen.” This won’t allay concern he would reject any unfavourable votes like he did in refusing to admit that he lost the 2020 election fair and square.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.