ON DECK FOR TUESDAY, FEBRUARY 24TH

KEY POINTS:

Mixed markets are more stable this morning

- Scotiabank kicks off a strong start to Canada’s bank earnings season

- Yen sinks on rift between PM Takaichi and the BoJ

- Light US data focused on consumer confidence—watch jobs plentiful

- Trump’s SOTU speech is unlikely to win where it counts

- Iran could dominate risk at any moment

- Why shipping costs are not spiking on Iran risks so far

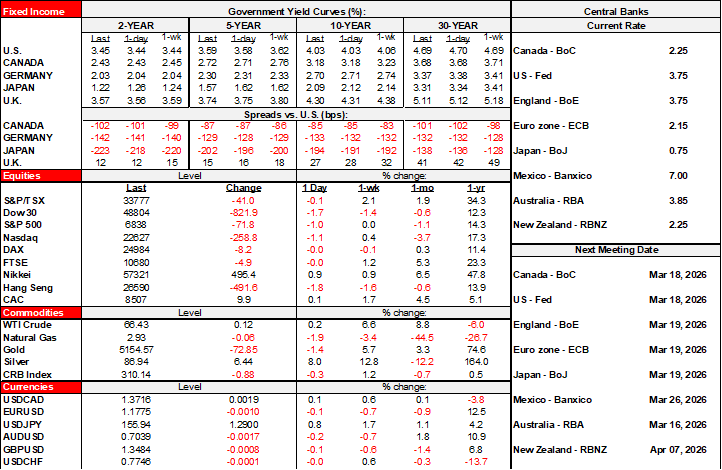

Markets are mixed but generally more stable than they were yesterday. Sovereign yields are generally little changed except for JGBs that are rallying as they catch up from holiday and in reaction to optics of a tiff between PM Takaichi and the BoJ. Stocks are mixed with generally small movements in either direction across N.A. futures and European cash after Chinese and Japanese markets returned from holiday to drive stocks higher. The yen is depreciating after local press reports out of Japan indicated that PM Takaichi expressed concern about further rate hikes with BoJ Governor Ueda.

Otherwise the return of Japan and China from holidays may be a factor in helping to stabilize most markets. Maybe markets are shaking off a work of fiction on AI from a shop that nobody previously heard of and that was as believable as Trump being on hockey skates. Tensions around Iran remain in the mix. Scotiabank got off to a strong start to Canada’s bank earnings season (see below) while light US data is on tap. Trump’s SOTU speech is tonight.

STRONG START TO CANADA’S BANK EARNINGS SEASON

Scotiabank (my employer) kicked off the Q1 earnings season for banks this morning with a solid beat. Adjusted EPS was C$2.05 (consensus $1.95). ROE of 13% beat consensus at 12.2%. NII was higher than expected at C$5.58B ($5.5 consensus). Expenses were lower than expected at $5.3B ($5.46 consensus). Key was guidance that medium-term objectives can be delivered in 2027 which is a year ahead of Investor Day commitments.

LIGHT US DATA TO BE FOCUSED ON CONSUMER CONFIDENCE

Only light US data is on tap for today including weekly ADP private payrolls (8:15amET), US home prices for December (9amET), the Richmond Fed’s manufacturing index for February (10amET) and US consumer confidence for February (10amET).

Of these, consumer confidence probably stands the best chance at being impactful to markets. Watch measures like ‘jobs plentiful’ that offers a consumer take on the tightness of the job market, as well as 1-year ahead inflation expectations.

TRUMP’S SOTU SPEECH IS UNLIKELY TO WIN WHERE IT COUNTS

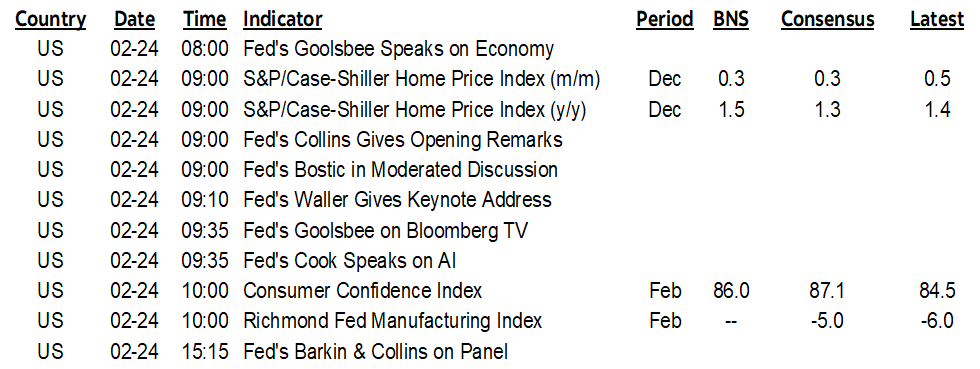

Trump has indicated that tonight’s State of the Union speech (9pmET) will be long. Uh oh. Last year’s clocked in at a record 100 minutes. His biggest challenge is how to appeal to voters without sounding out of touch and dismissive toward their concerns as his approval rating sinks (chart 1). I haven’t seen signs of his willingness to do so and he’s simply not winning where it matters. There is good reason for this and I went over an economist’s take on the State of the Union in my weekly (here) that included a balanced take on a large variety of measures and also included comparisons across Presidents by several of those measures.

IRAN COULD DOMINATE RISK AT ANY MOMENT

Off-calendar risk could easily dominate at any moment should Trump put to work all the firepower gathered around Iran. Timing possible action is purely speculative, but the signs are building.

The US ordered the evacuation of its embassy in Lebanon yesterday afternoon due to fear of retaliation. The USS Gerald Ford is arriving near Israel’s coast with another carrier off the coast of Oman along with thousands of US troops, dozens of fighter jets and over a dozen ships. Iran has moved ballistic missile launchers into position aimed at Israel and US bases.

All of that obviously invites speculation it’s not just a bluff, yet US Joint Chiefs Chairman General Caine warned Trump today about a campaign against Iran. Plucking Maduro is one thing, Iran's Ayatollah Ali Khamenei is another especially with the reported multiple layers of leadership that have been created throughout the regime and military. There are plenty of geopolitical pundits arguing that Trump has left himself without an out which could prove to be a dangerous thing especially given his commitment in the election campaign to avoid forever wars.

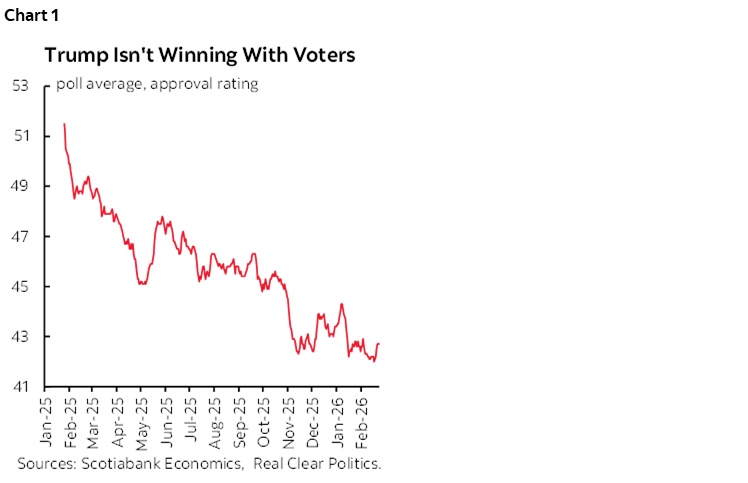

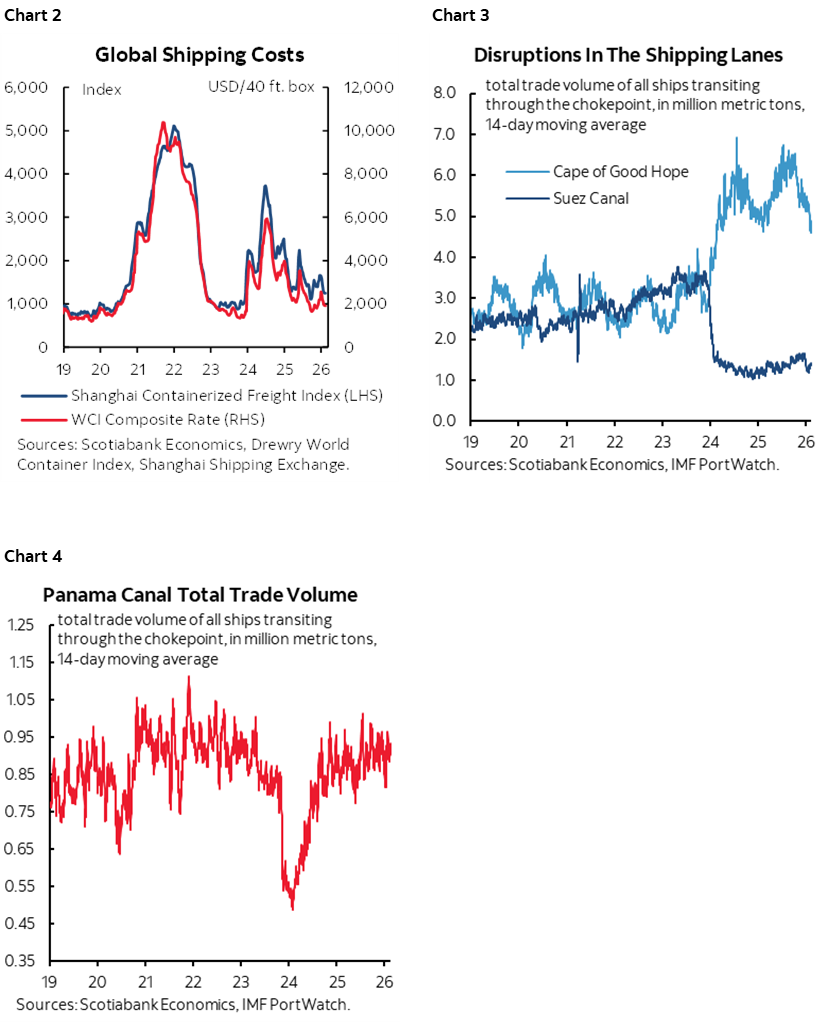

Yet so far we're not seeing even so much as a hint that shipping costs are reacting as they did in past tensions and especially in the pandemic. Chart 2 shows shipping costs through the Suez canal as a route from Asia to Europe. Reasons why we are not seeing such a reaction include excess capacity in global shipping and route adjustments. Further, chart 3 shows that the Suez never recovered from the workaround the last time into 2024 as shipping companies took the long route around the Cape of Good Hope to dodge tensions with Iran and Houthis flinging missiles into shipping lanes. Chart 4 shows that the Panama Canal’s rebound helps with shipping volumes versus the correlated problems with the Suez canal in 2024. So far this is all a good thing for shipping costs and inflation risk.

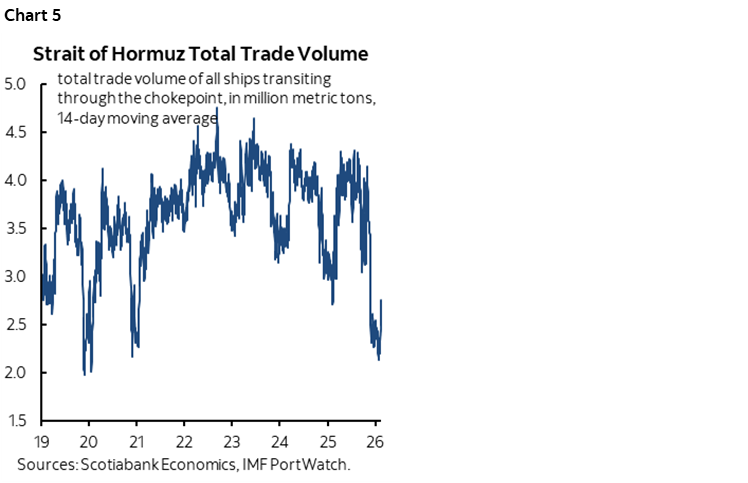

Yet chart 5 shows that the Strait of Hormuz has seen shipping volumes drop off recently. The Strait of Hormuz carries an estimated 20% of global oil production and a further 20% of LNG shipments. War risks shutting the Strait and hence clearly risks driving spikes in both prices which is very much opposed to Trump’s constant desire to secure lower energy prices.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.