ON DECK FOR MONDAY, FEBRUARY 23RD

KEY POINTS:

- Markets are largely shaking off trade turmoil for now…

- …although Japan and China are out

- EU to halt ratification of trade deal with US

- Updated tariff rate calculations for Canada, Mexico and the US

- German IFO surprises a bit higher

- Mexico’s economic growth doubled consensus in December

- US factory orders, Dallas Fed’s index, Fed’s Waller on tap

- Team Canada showed class in an unfortunate loss

- Global Week Ahead — The State of the Union (reminder here)

Markets are little changed across broad asset classes despite ongoing spillover effects from policy turmoil in the United States. Much of the world’s money is sidelined. China remains out for the Lunar New Year holiday. Japan’s markets were shut overnight for the Emperor’s birthday. US and Canadian equity futures are slightly negative with Europe mixed. Sovereign yields are little changed across most markets except underperformance by New Zealand’s curve. Gold is up about $45/oz, but oil is softer despite more weekend saber rattling about Iran.

The EU said this morning that it would halt ratification of its trade deal with the US, likely in no small part because the US administration’s choice of tariff tools, levies and exemptions has been in turmoil.

A very light line up of calendar-based risk kicks off the week. German IFO business confidence surprised a bit higher in February's reading with both present and expected assessments rising. Mexico’s economic activity index advanced by 0.4% m/m SA in December, roughly doubling consensus. The US updates factory orders for December that will struggle to stay in the black after durable goods orders fell 1.4% due to weaker transportation orders (10amET). Fed Governor Waller speaks on the economic outlook after the trade turmoil (8amET) before the Dallas Fed’s manufacturing index (10:30amET).

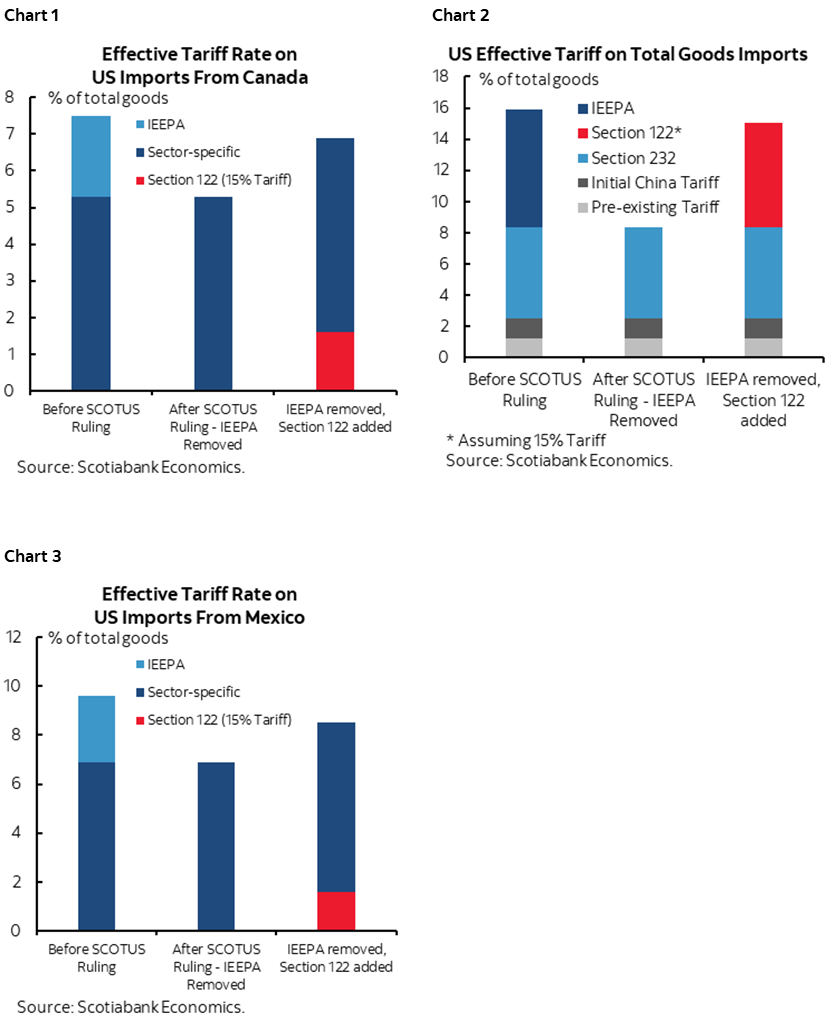

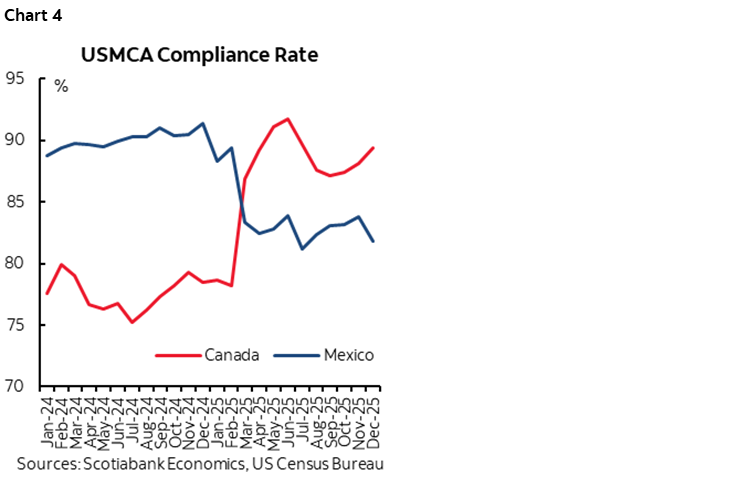

NEW TARIFF RATES FOR CANADA, MEXICO AND THE US

After swapping Section 122 tariffs for IEEPA tariffs in Trump’s press conference on Friday afternoon, the White House released the executive orders (here and here) and fact sheet (here) Friday evening after sending my weekly. At first it was a tentative plus for Canada and Mexico to see America—the developed world’s most reluctant trading nation—easing off some of the charges for now.

Then on Saturday, Trump changed his mind in a social media post that lashed out at the Supreme Court again and raised the rate to 15%. There is, however, no accompanying executive order to go with that increase. It may not rise to 15% given that Trump threatens a great deal and executes a fraction of his threats.

Assuming that the rate does get officially changed to 15%, we can refresh our calculations for effective tariff rates. Key is that CUSMA/USMCA compliant goods from Canada and Mexico are exempt from the 15% section 122 tariff that Trump is using to replace IEEPA tariffs. Also exempt from the 15% Section 122 tariff will be Section 232 tariffs. Furthermore, the Section 122 tariff will not stack on top of existing sector-specific tariffs.

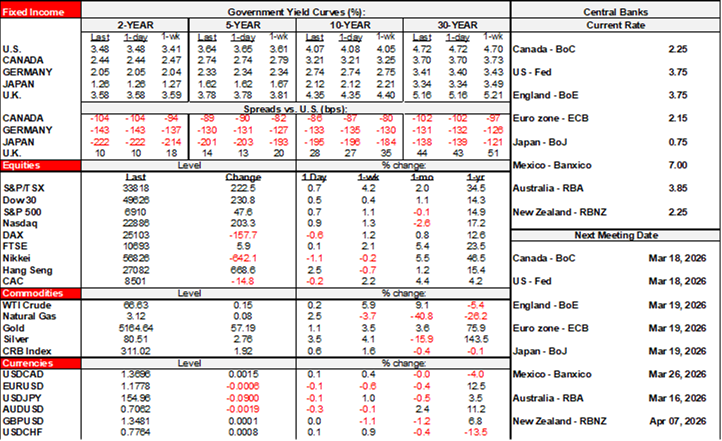

Charts 1–3 show the results. Since almost 90% of Canada US trade is compliant and duty free, this means that around 13%+ of the potential 15 percentage points of the Section 122 tariff will not apply. Mexico’s compliance is lower and so more of the 15% rate will flow through (chart 4).

This means that the average effective tariff rate imposed on Canadian exports of goods to the US will drop from 7.5% to 6.9%. On exports of goods and services to the US it goes from 6.3% to 5.85%.

Canada’s overall average effective tariff rate on all exports to everywhere in the world dropped from 4.5% to 4.2% which is a rounding error. This is not a debilitating shock, folks. CAD at 1.37 from 1.20 coming out of the pandemic alongside last fall’s BoC insurance cuts, fiscal stimulus and supportive commodity prices (especially if turmoil escalates in the middle east) all help to insulate the economy from the effects as it adjusts to a more isolationist, protectionist and insular United States. The bigger risk to Canada than tariff rates is if the cracks in the outlook for the US economy continue to get bigger.

As for the US, the tariff rate imposed on its own imports of goods and services from around the world went from 12.9% (15.9% on goods) before the SCOTUS ruling and Trump’s changes to 12.3% (15.1% goods) after all was said and done.

And for Mexico, the ETRs went from 7.3% on all exports to the world (8.8% to the US) to 6.4% (and 7.8%).

There are two caveats in addition to whether the order actually does change to 15% from 10% . A minor one is that there were other targeted exemptions listed in the executive order, but their influence on the calculations is likely small.

The bigger caveat is that Trump has said he plans on launching section 301 investigations and this could give rise to more protectionist sector-specific measures. It can take months to conduct such ‘investigations’ at the behest of the USTR and the outcomes could be rather arbitrary.

Such arbitrariness adds to the arbitrary rationale for the Section 122 tariffs given that there is no balance of payments crisis in the US including no currency crisis in a flexible exchange rate regime that differs from the fixed rate change rate regime of the founding context for Section 122 tariffs. I’m sure affected companies have put their legal teams to work.

Overall, protectionist US trade policy remains ambiguous, chaotic and lacking merit. The costs will continue to be borne by Americans as at least five studies by global groups conclude.

TEAM CANADA SHOWED CLASS IN AND UNFORTUNATE LOSS

Kudos to the US team for their first Olympic gold in nearly half a century. Their win keeps the sport internationally competitive and resuscitates US hockey competitiveness after a long drought in international competition and that’s good for everyone who enjoys the sport. It inspires American kids to take up the sport and stick with it just as happens in my country and that’s a beautiful thing. It gives American kids of all ages something to celebrate about a game that is flourishing across much of the continent and world. The Americans have created their share of top talent as the NHL grew stateside. There were truly very talented players on their team who played well throughout the tournament.

Yet hearts hang heavy as Canada lost at our game yesterday. Yes, our game, as no other country can claim that the sport permeates so much of their culture from backyard rinks to street games, from raucous arenas and bars to living rooms. Hockey here is like cricket in India, or football in many European and Latin American countries. You’ll never take it in spirit or exceed its share of our soul.

Both countries needed the win for different reasons. Only one could. America because of its deepening divisions at home. Canada needed it because of challenges at home and the relentless, unprovoked and unjust attacks upon it by the US administration.

Yet Canada has nothing to be ashamed of after consistently outplaying the opponent, outshooting them by a landslide, and having multiple great chances despite missing one of their best players. An overlooked too many men on the ice penalty was unfortunate. Olympic hockey’s treatment of overtime is an absolute joke; 3 on 3 sudden death and then a shoot out if overtime is to no avail? Those are hockey rules created by bureaucrats who just want to get the game over with, not by people who truly love the sport.

Canada was not let down in terms of what really matters because the Canadian team showed grace and class. They took it like Canadian gentlemen.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.