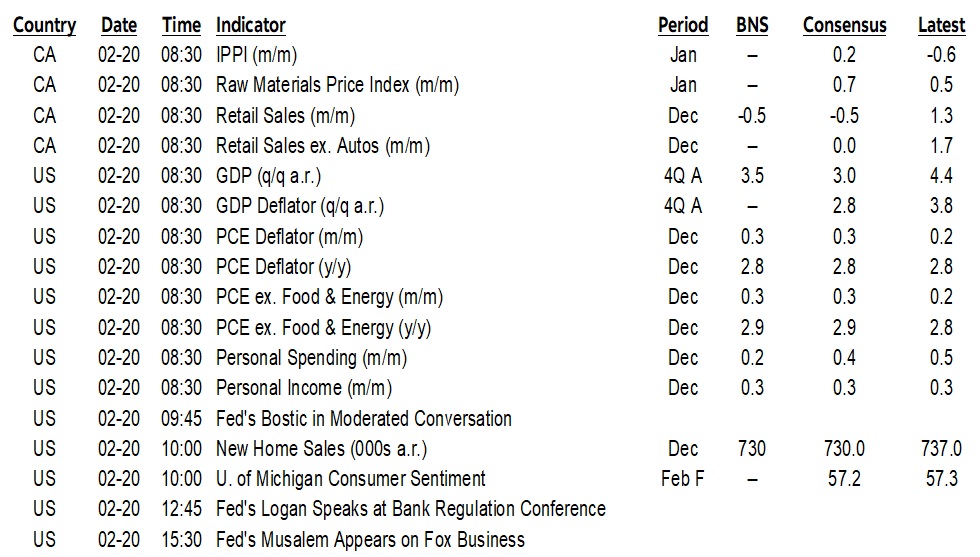

ON DECK FOR FRIDAY, FEBRUARY 20TH

KEY POINTS:

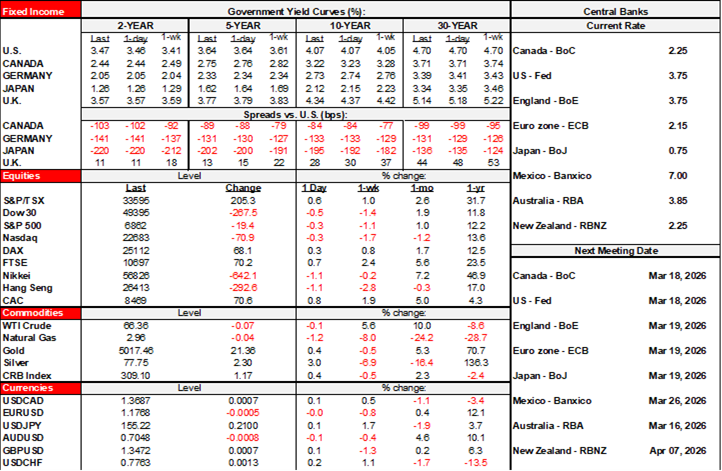

- US equities are underperforming ahead of key data, possible tariff decision

- SCOTUS decision on IEEPA tariffs is possible today, but here’s why it’s unlikely

- Q4 US GDP estimates are all over the map

- Global PMIs diverged

- Lagging US PCE inflation

- Canadian producer prices signalling lagging pass through to consumer prices

- Canadian consumer spending may be weighed down by harsh weather

- UK consumers charged ahead into the new year

Global markets are tentatively showing promise of a risk-on session with equities pointed higher across most exchanges except the US following an overnight dump of global PMIs and UK retail sales.

That could change with a deluge of US data and a possible—but doubtful—SCOTUS IEEPA tariff decision on tap. Canadian markets face inflation and consumer updates.

WHY A SCOTUS DECISION ON IEEPA TARIFFS TODAY WOULD BE A SURPRISE

And SCOTUS will deliver an opinion or opinions starting at 10amET. An IEEPA decision is possible but unlikely for two main reasons.

1. It would be surprising if they ruled before Trump's SOTU speech next Tuesday. The tone of the SCOTUS hearing on the tariffs and the odds favour ruling against their use in some form or another with uncertainties over what to do afterward, but it doesn't strike me as the way the court rolls to dump on the trade agenda right before Trump's showtime. The justices will all be seated in Congress for the speech and no doubt Trump would lash out repeatedly against them if the decision were to be unfavourable to the administration.

2. As noted in my weekly, the Court has been transitioning toward providing most of its opinions in June and then splitting town so to speak.

The same two-pronged argument applies to why it would be surprising if SCOTUS ruled next Tuesday or Wednesday that are also opinion days.

KEY US READINGS ON TAP

The US updates Q4 GDP that is expected to be another strong quarter but with weaker hand-off effects into Q1 through higher frequency readings (8:30amET). Consensus expects growth to land at 2.8% q/q SAAR but with a very wide dispersion of readings from about 1½% to 4¼%. The Atlanta Fed’s nowcast fell to 3% from a peak of 5½% at one point. Consumption should add about two percentage points in weighted terms.

US personal income, spending and inflation readings for December are also due (8:30amET). US PCE inflation is a lagging reading due to the shutdown as it’s for December whereas we already have January CPI and then next Friday we’ll get January PPI to help inform expectations for the next PCE reading. PCE and core PCE measures of inflation are expected to rise by about 0.3% m/m SA.

New home sales during December will also be released (10amET).

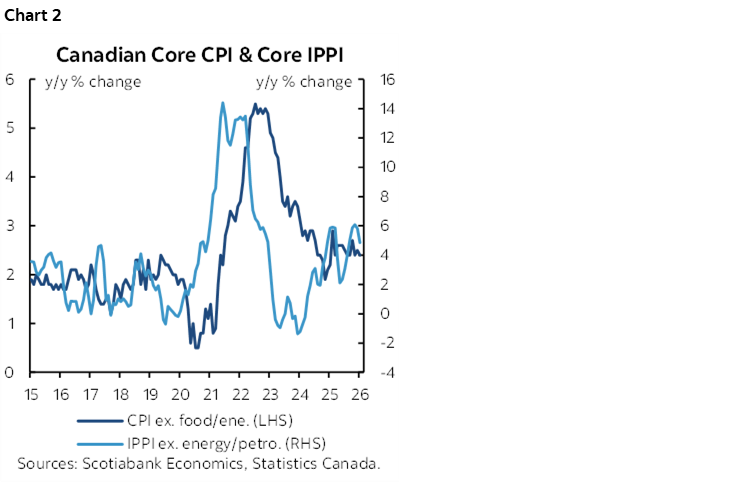

CANADIAN CONSUMER AND INFLATION TRACKING

Canada updates producer prices in January this morning (8:30amET). They’ve been ripping higher with correlated potential pass through into consumer prices ahead (chart 2).

Retail sales are expected to be soft for December based on earlier guidance (-0.5% m/m SA), but the preliminary flash estimate for January’s sales may matter more (8:30amET). Harsher than usual winter weather could be a downside risk.

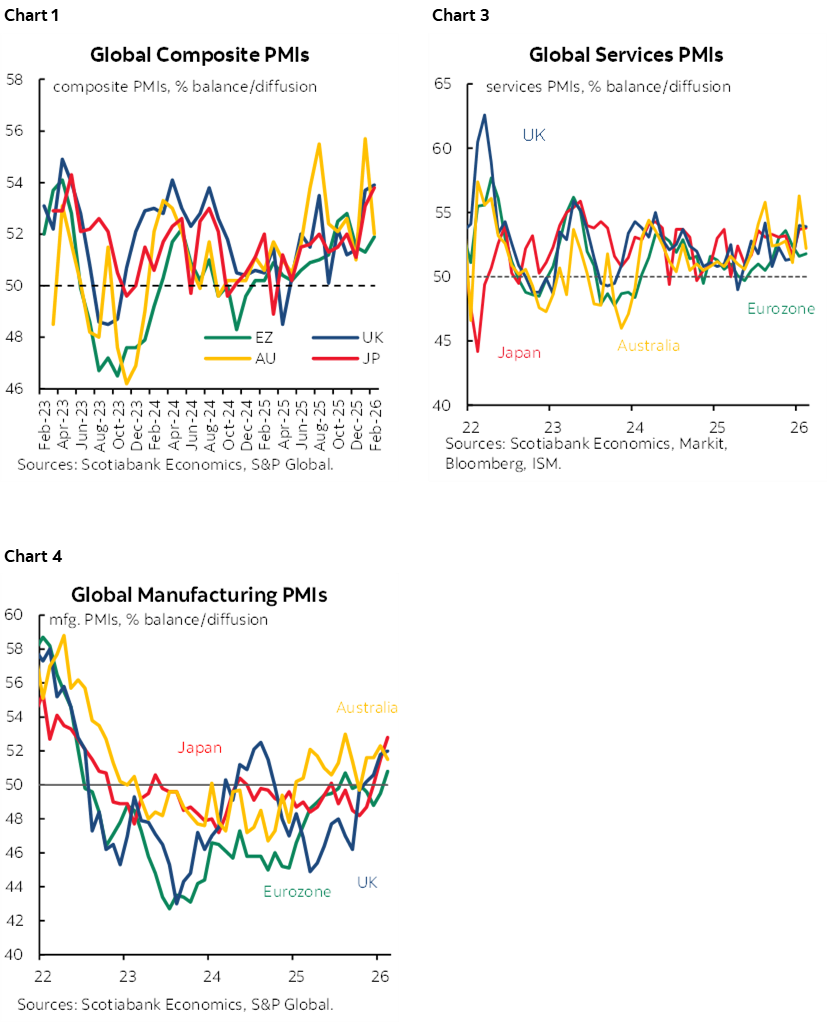

MIXED GLOBAL GROWTH SIGNALS FROM PMIS

Global purchasing managers indices (PMIs) signalled quicker economic growth in Japan, the Eurozone and India, unchanged growth momentum in the UK and cooler growth in Australia (charts 1, 3 and 4). The divergences in data contributed to differential effects on markets as, for example, Aussie bond yields fell by about 5bps across the curve to outperform most other benchmarks.

The A$ fell and dragged the kiwi dollar with it as Australia’s composite PMI fell 3.7 points to 52.0, signalling softer economic growth. Most of the deceleration came through the services PMI (52.2, 56.3 prior). Manufacturing also eased but by eight-tenths to 51.5.

Japan’s composite PMI increased seven-tenths to 53.8, signalling broader growth driven by a pick-up in the manufacturing PMI as the services PMI was essentially flat.

The UK composite PMI was basically unchanged (53.9, 53.7) including across services (53.9) and manufacturing (52).

The Eurozone’s composite PMI edged a little higher to 51.9 (51.3 prior) mainly due to an acceleration in manufacturing (50.8, 49.5 prior). Germany’s composite PMI moved up a full point to 53.1 with gains in both services and manufacturing. France’s composite PMI edged higher but not enough to escape a sub-50 contraction signal at 49.9 with both manufacturing and services hovering in contraction.

India’s composite PMI increased to 59.3 from 58.4 as manufacturing accelerated (57.5, 55.4 prior) and services were little changed at 58.4.

UK CONSUMERS CHARGED INTO THE NEW YEAR

UK consumers embraced the new year with a spending frenzy. Retail sales volumes were up by 1.8% m/m in January and 2% ex-fuel versus consensus expectations for gains of only about ¼% in both measures.

Japanese national core CPI decelerated to 2.6% y/y from 2.9% and a tick beneath consensus.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.