ON DECK FOR MONDAY, FEBRUARY 2ND

KEY POINTS:

- Commodities taking it on the chin

- Crypto stabilizing after weekend sell-off

- RBA on deck tonight with hike risk in the air

- India’s budget hits stocks

- US, Canadian manufacturing data on tap

- Light overnight data, US T borrowing estimates on tap

- Global Week Ahead — Mellow Metal’s Mess (here)

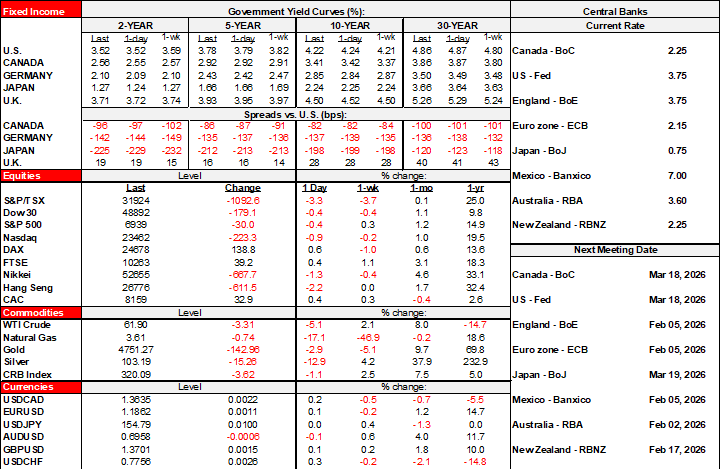

Risk appetite is mixed across global markets to kick off the first week of February. Commodities are selling off with declines led by oil (futures down ~5%) and gold (-3%); so much for month-end rebalancing driving weakness versus broader forces. US equity futures are in the red by roughly ½% to 1% with TSX futures little changed. European cash markets are mildly higher. Asian equities fell across all major bourses with losses led by Seoul (-5¼%), Mainland China (-2½%) and the Nikkei (-1¼%). Bitcoin is off another 7% since Friday as crypto currencies took it on the chin throughout weekend trading, while tether has stabilized and inched back closer to the requisite parity to the dollar. Sovereign bonds are rallying a touch across the US and UK long-ends. Currencies are divided against the dollar.

There is very little by way of fresh developments to consider. India’s Budget early Sunday morning (ET) drove a sell off in local stocks yesterday that is since moderating; the main issue was a tax hike on equity derivative trades.

Overnight data was light, including German retail sales volumes that barely grew (+0.1% m/m) in December. Chile’s economy soared in December, posting a 0.6% m/m SA gain in the volatile monthly economic activity index (a GDP proxy) that consensus expected to fall. Peru’s January CPI (+0.1% m/m SA) that was on the screws and Indonesia’s CPI that was slightly softer than expected.

Key, however, will be tonight’s RBA decision (10:30amET). A majority within consensus expect a 25bps hike that markets attach almost 75% odds to. See my weekly for an outline of the cases for and against a hike at this meeting.

On tap into the N.A. session is modest data risk on the N.A. manufacturing sector and US Treasury quarterly borrowing estimates (3pmET).

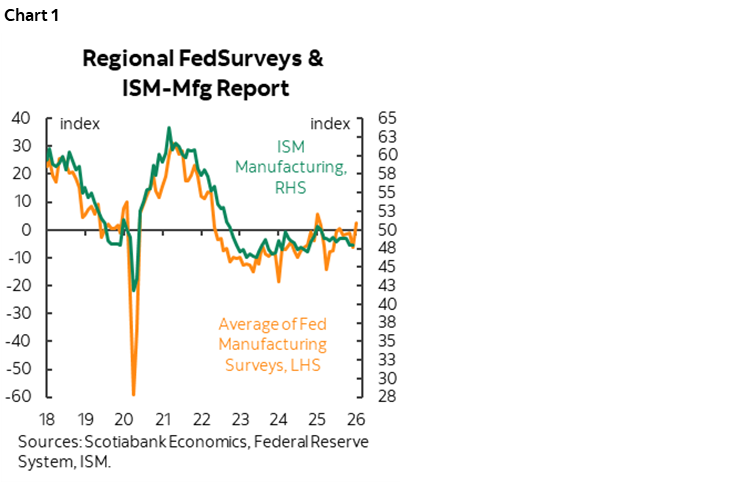

Canada updates the manufacturing PMI for January (9:30amET). The US will refresh ISM-manufacturing for January (10amET). The US gauge is expected to improve a touch partly on the back of regional manufacturing indices (chart 1).

Overall, however, markets will continue to consider the gulf between what Fed Chair nominee Warsh promised to get the job, and what he can and will deliver which in my opinion is ginormous. Warsh’s Senate confirmation testimony—assuming it arrives given stonewalling by Senate Tillis—may extend the over promising. Friday’s payrolls—with a side order of Canadian jobs—will also captivate markets.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.