ON DECK FOR THURSDAY, FEBRUARY 19TH

KEY POINTS:

- Bonds and stocks cheapening on monetary policy doubts, Iran

- Fed Hikes? Don’t hold your breath

- Fed Cuts? Don’t hold your breath

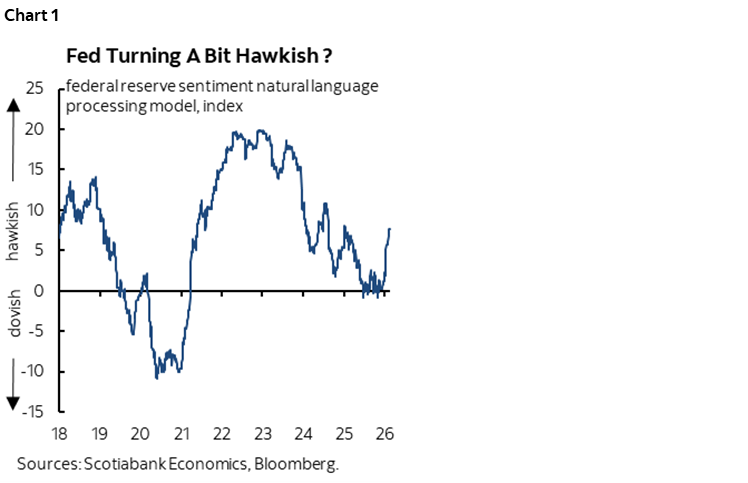

- Aussie jobs add to RBA hike pricing

- Murmurs of a Canadian Spring election call make no sense…

- …as assessing Liberal majority prospects will take months

- Canada, US to update trade figures that could inform Q4 GDP tracking

- BSP cut with little impact on local markets

- BI held with a cautious bias

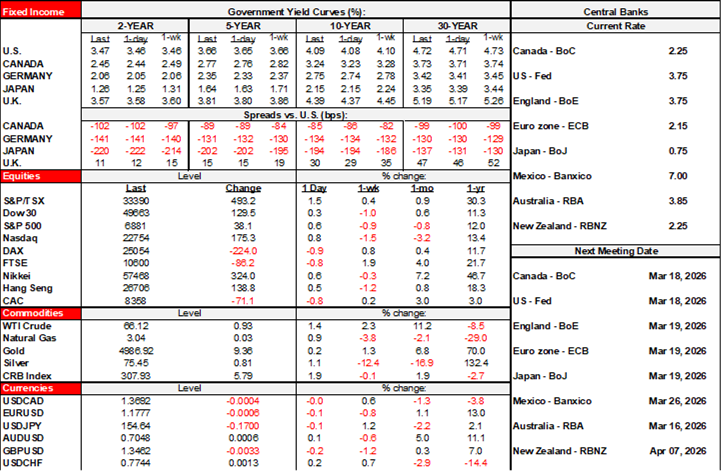

Bonds and equities are both cheapening this morning. By far the biggest rate moves are Down Under after jobs data (see below). The rest of the bond and equity complexes might be a little disturbed by yesterday afternoon’s FOMC minutes and headlines about potential Fed hikes (see below) plus risks around Iran as oil prices move up a buck. Equities are also moving lower across NA futures and European cash. Other than the stuff of salacious gossip, former Prince Andrew’s arrest might put in play court proceedings that reveal a few degrees of separation from the conduct of others in high places.

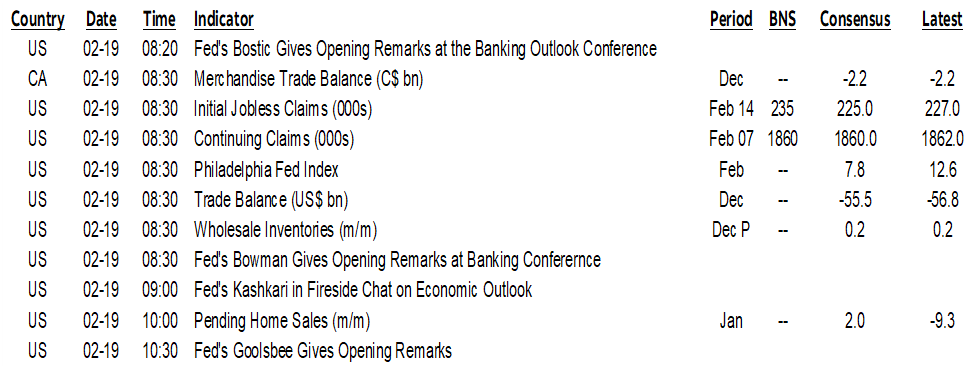

Fed Hikes? Don’t Hold Your Breath

Yesterday afternoon’s FOMC minutes were a generally bland affair except for one line that has driven hawkish headlines as hawkish sentiment takes over (chart 1). Here it is:

“Several participants indicated that they would have supported a two-sided description of the Committee’s future interest rate decisions, reflecting the possibility that upward adjustments to the target range for the federal funds rate could be appropriate if inflation remains at above-target levels.”

First up is a reminder that the minutes are not vote-weighted. I don’t hear any of this year’s voting FOMC members even remotely entertaining serious thoughts about hiking.

Second, ‘several’ is not quorum in the way the Fed uses language to indicate the degree of plurality of opinion.

On the flipside, the Committee is in no rush to deliver more cuts either. ‘Several’ participants indicated openness to further easing “if inflation were to decline in line with their expectations” while “some” participants indicated a preference to hold the policy rate steady for some time to assess incoming data. “A number” of the latter participants said easing “may not be warranted until there was clear indication that the progress of disinflation was firmly back on track.”

I still think the Committee is curiously taking an overly rosy view of the labour market after they said downside risks to employment had moderated in recent months. If the job market continues to disappoint—excluding narrow health sector hiring—then the Committee might swing back toward expressing concern about the job market.

RBA Hike Pricing Edges Up After Jobs Report

Australia’s job market continues to crank out gains (chart 2). January’s 18k increase followed the prior 69k rise. Full-time job creation dominated both times with a gain of 57k in December and then about 51k in January. The A$ is the class leader this morning while Australia’s rates curve was hammered in bear flattener fashion as the 2s yield increased by 7bps. Markets have the RBA holding on March 18th but upped pricing for a hike in May by a few basis points to being almost fully priced. Markets also raised cumulative hike pricing this year about 40bps, thereby leaning toward a half point hike.

Can the Talk of a Spring General Election in Canada

The main takeaway from the latest Conservative turncoat’s move to cross the floor to the Liberals is that it changes nothing by way of the math behind attaining majority status that will only be informed by Spring. Only by then will we know whether the Libs squeak out a majority without the need for another costly election.

The Libs now have 169 seats (here). There are three vacancies with by-elections pending to fill Chrystia Freeland’s seat after she resigned, Bill Blair’s seat after he was sent off to the UK, and Tatiana Auguste’s seat in Quebec after a court nulled the election outcome she won by one single vote. The one where the Libs are most vulnerable is the one in Quebec where the BQ can be fully expected to launch an all-out campaign to snag it. That last by-election cannot be held until April 6th at the earliest (here). Blair’s former riding can hold a by-election no earlier than March 23rd while Freeland’s former riding can hold a by-election no earlier than March 2nd.

There are likely to be two more by-elections in ridings that have yet to be vacated but may soon be. Liberal MP Erskine-Smith said earlier this month that he will resign his federal seat as soon as Ontario Premier Ford calls a by-election in the provincial riding of Scarborough Southwest and with sights set on becoming leader of the Ontario Liberal Party. NDP MP Alexandre Boulerice indicated he may vacate his seat and run for Quebec Solidaire in the October provincial election.

Because of the pending by-elections and how they might propel the Liberals to the 172 seats needed for a majority in the House of Commons, it would make no sense whatsoever to call a general election at least until after the by-election for Auguste’s seat.

Further, even if a general election were to be eventually called should the Libs fall short of a majority, it’s not clear how voters would behave in the multiple ridings that elected a Conservative only to see him cross the floor. They used the Conservative brand and Conservative resources and voters thought they were getting a Conservative. Voter retribution cannot be ruled out. Nor should it be.

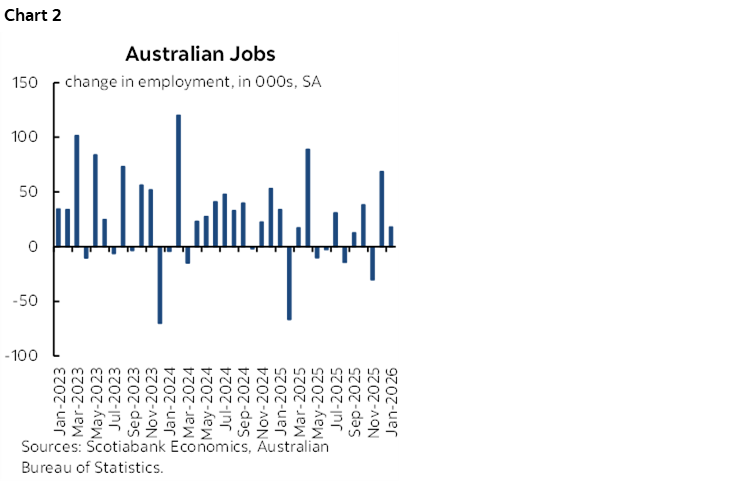

US, Canadian Trade on Tap

Canada and the US will update trade figures for the month of December this morning (8:30amET). We have little to go by in terms of estimates for either of them. The US normally releases the merchandise portion before the total balance but this time is releasing it simultaneously as data releases continue to catch up from the federal government shutdown.

For Canada, the things to watch will be revisions and how December data informs tracking of trade contributions to growth. We already know that Q3 contributions to GDP growth will likely be revised up in next Friday’s GDP figures after mapping monthly trade tracking onto the GDP account estimates (chart 3) but we don’t know the potential offsets, like whether stronger than initially guessed exports in the absence of Canada-US trade data came at the expense of inventories that may have been overestimated, or production that was underestimated.

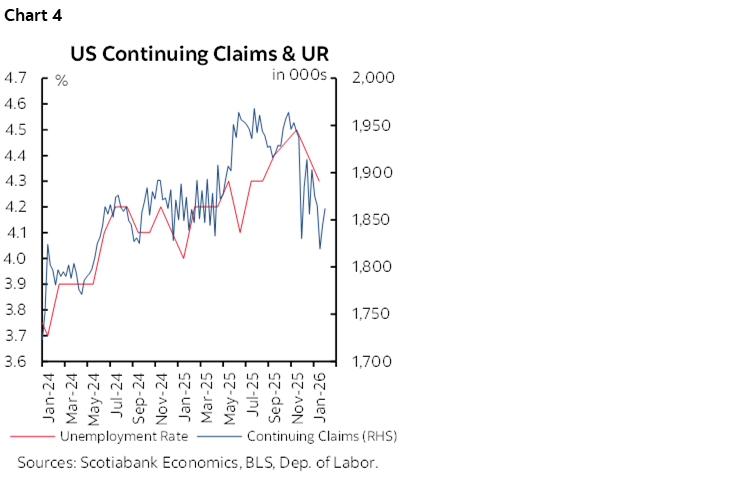

The US also updates weekly jobless claims (8:30amET) with continuing claims possibly informing expectations for February’s unemployment rate (chart 4) and pending home sales for January (10amET).

BSP Cut, while BI Held

Bank Indonesia held its policy rate unchanged at 4.75% as widely expected. BI retained an open bias toward further easing but with a cautious eye on the rupiah and recently higher than expected inflation.

Bangko Sentral ng Pilipinas cut its overnight borrowing rate by 25bps to 4.25% as generally expected. The bias was conditional upon further data. The peso depreciated a touch while base rates were little changed.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.