ON DECK FOR TUESDAY, FEBRUARY 17TH

KEY POINTS:

- Markets kick off shortened trading week with some apprehension

- Canadian CPI—one of two before March BoC & pick your core measure!

- BC kicks off Canada’s provincial budget season

- UK job market updates add slightly to BoE March cut pricing

- GDP disappointments in Japan, Colombia, Thailand

- Global Week Ahead: US Growth is Strong — Don’t Blow It! (reminder here)

Global markets are starting a shortened trading week in Canada and the US with some apprehension. Sovereign bond yields are broadly lower by 1–3bps or so across most yardsticks. Equities are mixed with N.A. futures slightly in the read versus European cash markets that are slightly in the black. The yen is recovering this morning after getting hit by GDP to start the week, but otherwise, most currencies are little changed versus the dollar with the notable exception of pound sterling post-jobs. Gold is down US$50 or so, oil is mixed with Brent flat and WTI up 1.5%.

What you may have missed while out yesterday (a trio of GDP disappointments plus minor Canadian data) is recapped below along with overnight developments (UK jobs).

The main thing on the docket today is Canadian CPI and then the start of Canada’s provincial budget season.

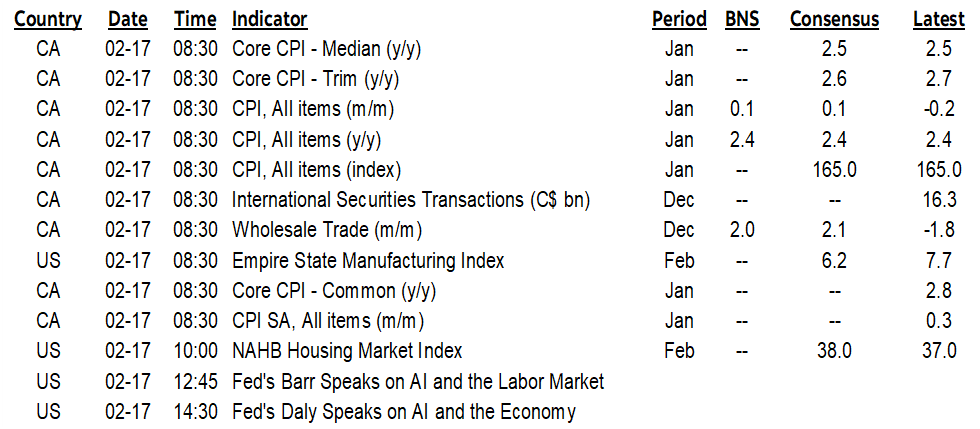

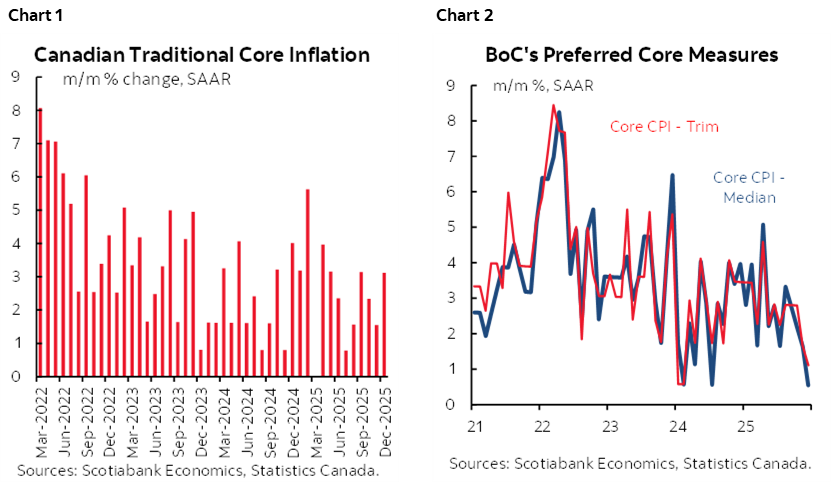

CANADIAN CPI — SIT THIS ONE OUT

Canada updates one of two CPI readings before the next BoC decision on March 18th this morning (8:30amET). January’s reading is expected to be up by only 0.1% m/m NSA and unchanged at 2.4% y/y. See my preview in the week ahead article.

Key will be the various core readings. Monitor each of them since they have recently offered conflicting signals. Chart 1 shows traditional core CPI that excludes food and energy commodities and how it picked up and has generally been more resilient of late. Chart 2 shows the trimmed mean and weighted median gauges that have been waning. The BoC keeps flip-flopping between which measure(s) it prefers and lacks consistent clarity on the matter. Onto the data.

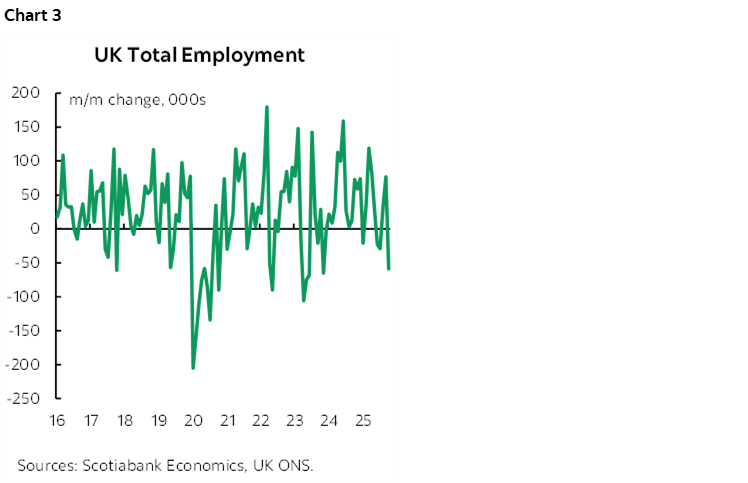

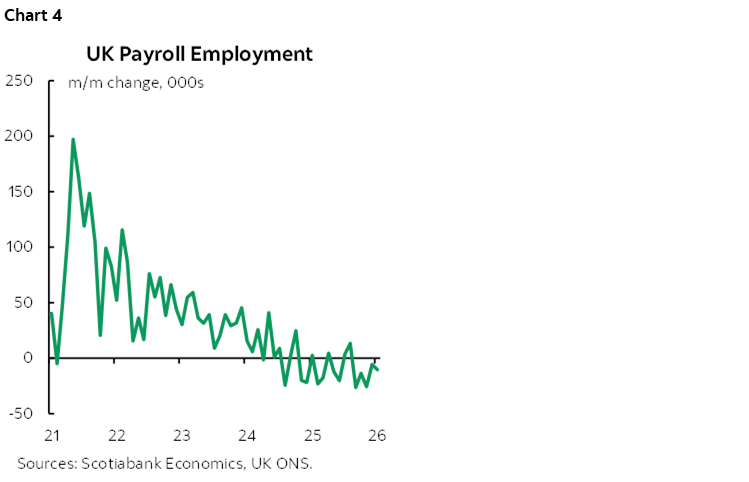

UK JOB MARKET READINGS BARELY IMPACT MARKETS

UK job market readings prompted slightly lower UK two year yield and a small depreciation of pound sterling to the dollar. The probability of a Bank of England cut on March 19th increased a bit to about 80%. The overall effects were minor.

- total employment fell by 59k m/m in December. After surging up to June, employment has been largely treading water (chart 3).

- Payroll jobs fell another 10.6k but the prior month was revised to a dip of only 6k instead of 43k (chart 4).

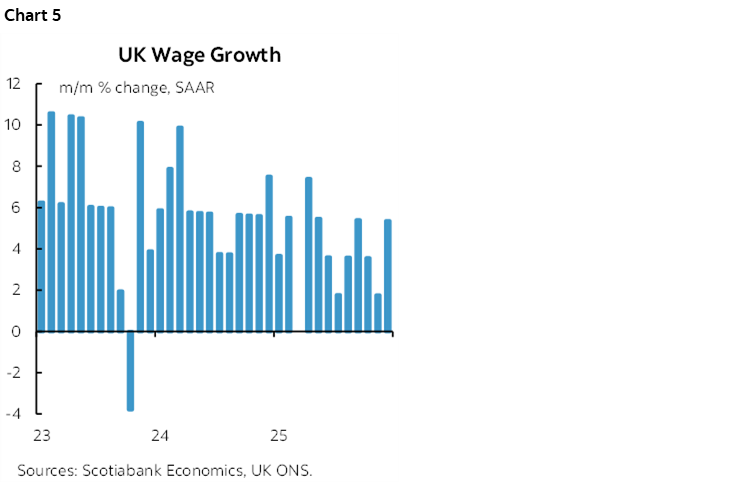

- wage growth accelerated to 5.4% m/m SAAR in December (chart 5). The three-month moving average is running at 3.6%.

- jobless claims picked up to 29k in January but the prior month was revised down to about 3k from 18k.

- job vacancies fell 10k in January. They remain slightly above the long-term average (chart 6).

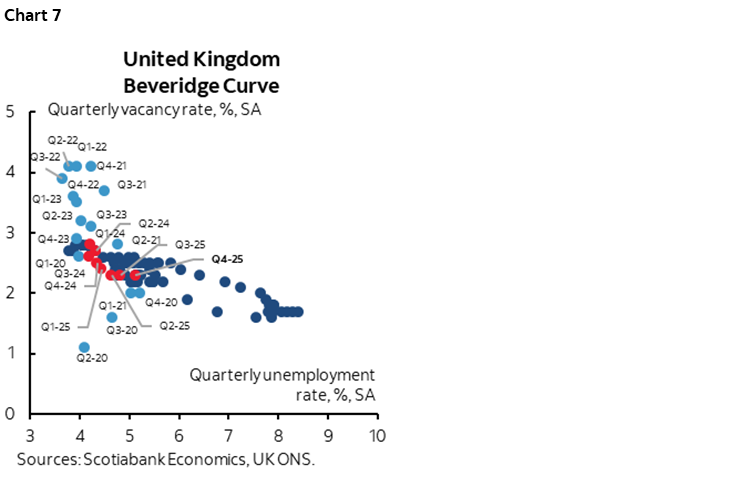

- So where does this leave us in terms of how the BoE may view the overall state of the UK labour market? Chart 7 shows the balance between job vacancies and unemployment.

JAPAN’S ECONOMY DISAPPOINTS

Japan’s economy disappointed expectations and the yen kicked off the week as the worst performing major FX cross to the dollar while JGBs bull steepened after GDP was updated on Monday morning. GDP grew by only 0.2% q/q SAAR versus 1.6% consensus. The disappointment came despite a mild upward revision to Q3 that saw GDP shrink by 2.6% instead of 2.3% as originally reported.

Consumption was soft at a nonannualized growth rate of just 0.1% q/q SA with a mild upward revision to 0.4% in Q3 (from 0.2%). Business spending grew by only 0.2% after previously shrinking by -0.3%. Net exports were flat after a -0.3% drop in Q3 as both exports and imports shrank -0.3% implying no export contribution and less of an import leakage drag effect. Inventories dragged only -0.2% points off of Q4 GDP after a -0.1% drag in Q3.

Overall, Japan’s economy was posting moderate growth over 2024Q3 to 25Q2 but the wheels fell off over the last half of 2025 and the trends across the components suggest it’s not just because of global trade turmoil. Tightening monetary policy has been a contributing factor as well. Somewhat related was yen appreciation until last Spring.

Thailand’s economy sharply exceeded expectations with Q4 GDP growth of 1.9% q/q SA (0.6% consensus) and a mild upward revision to -0.3% in Q3 (from -0.6%). Construction was the fastest growing sector in Q4.

OTHER MINOR CANADIAN UPDATES

A pair of reports was issued on Monday morning when domestic and US markets were shut. Federal agencies didn’t get Family Day which is a provincial holiday and didn’t care to adjust their release schedules.

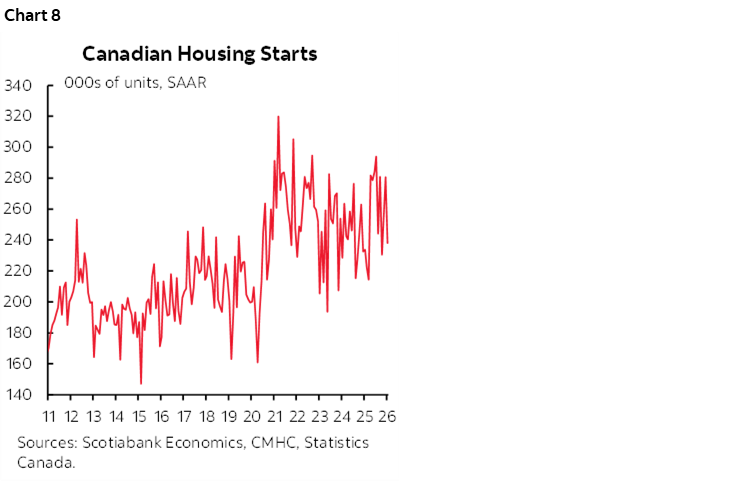

Canadian housing starts weakened to 238k SAAR in January from about 281k the prior month. That was a little weaker than my guesstimate (255k). All of the slowdown was in multiples (184,8k from 234.6k) as they overshot in December, while singles increased 15.8% m/m in January. Singles carry more economic value-added than multiples. Canada continues to post elevated readings for housing starts over about the past five years (chart 8).

Canadian manufacturing sales increased 0.6% m/m SA in December which was in line with Statcan’s earlier flash guidance. Volumes were up 1.8% which reverses most of the -2.1% drop in November. The inventory-to-sales ratio slipped to 1.69 months from 1.72 previously and has been cruising around little changed readings since a post-pandemic run-up until 2022.

OTHER UPDATES

Germany ZEW investor confidence slipped in February’s reading. The expectations component fell but remains close to the highest reading since mid-2021. At least the German analyst and investor community remains upbeat for what that’s worth.

Colombia’s economy disappointed expectations for Q4 GDP that grew by only 0.1% q/q SA (0.5% consensus).

The US calendar will be very quiet today with just the Empire regional manufacturing gauge for February (8:30amET) that kicks off another month of readings on the path to the next ISM-manufacturing report.

BC BUDGET TODAY

BC will kick off provincial budget season this afternoon with its 2026 budget at about 4:30pmET. Mitch Villeneuve shares his thoughts.

In its budget last year, BC forecast fairly sizeable deficits and a debt burden doubling from 17% of GDP in 2023–24 to 34% in 2027–28, earning ratings downgrades from S&P and Moody’s. Its fiscal updates since then show that the deficit for this year isn’t growing much further than initially planned, but the government will hope to make better progress in shrinking deficits going forward. The government has signalled that today’s budget will announce stronger spending restraint, though also that the large spending categories of health, education, and public safety will be protected—significantly limiting the scope for spending reductions.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.