ON DECK FOR FRIDAY, FEBRUARY 13TH

KEY POINTS:

- Risk-off ahead of US CPI, metals prices falling on tariff reversal

- Multiple studies confirm that Americans are paying for Trump’s tariffs…

- …confirming what we’ve argued all along…

- …and now the pressure is on to roll them back…

- …with movement afoot to reduce metals tariffs

- US CPI could be complicated by revised seasonal adjustments

- China’s home prices remain in freefall

- Chinese credit growth got off to a decent start

- Peru’s central bank held with neutral bias

- Russian central bank cut, reduced forward guidance

- Early bond close in Canada ahead of long weekends in Canada, US

Equities are broadly lower across N.A. futures, European cash markets, and overnight Asian markets as the Nikkei fell 1.7% and continues to consolidate initial euphoria over Japan’s election results. Sovereign bond yields are slightly outperforming in Europe relative to little change in the US and Canada. The dollar is broadly firmer. Aluminum and steel prices are somewhat lower in the wake of tariff headlines as explained next which is welcome news to consumers.

Trump Administration Possibly Moving to Reduce Metals Tariffs

As evidence mounts to confirm the understanding that it would be US companies and US consumers who would bear the brunt of Trump’s tariffs—not foreign companies as the administration claims—there is mounting evidence on the Trump administration to reverse its tariffs. Having been allegedly elected to manage affordability concerns, the administration is polling poorly as companies take offsetting steps to manage costs by trimming payrolls outside of healthcare and as prices rise.

Enter the latest example of the administration backing down. The FT reported earlier this morning that the administration is working to roll back some tariffs on steel and aluminum goods (here). Recall that the administration applies a 50% tariff rate on imported steel and aluminum and derivative products. It’s a frank admission by the administration that it got it wrong as every economist outside of the White House said they would.

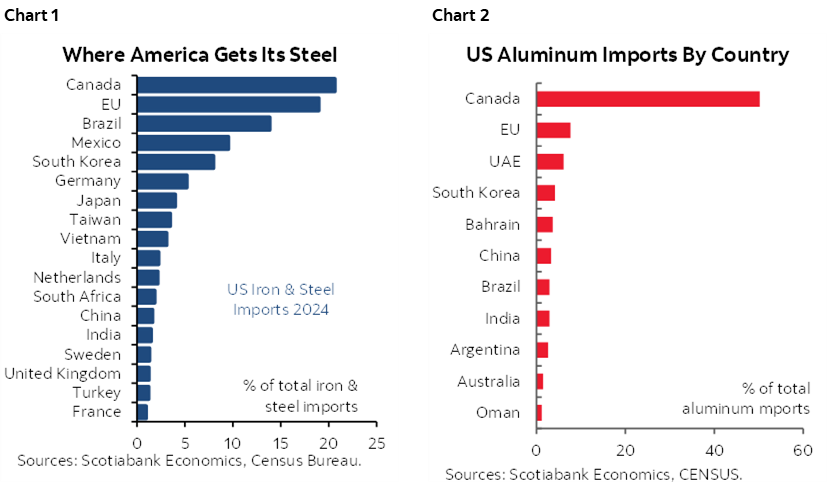

Who would be affected by the reduced tariffs pending details on which ones? Chart 1 shows where America gets its steel and chart 2 shows the same for aluminum. Canada is #1 on both charts.

As for the studies showing that it’s Americans paying for Trump’s tariffs, here’s one produced by the New York Federal Reserve’s economists. Here’s another produced by the Tax Foundation in the US. Here’s another from the Kiel Institute for the World Economy (a German think tank). Here’s the analysis of the budget lab at Yale. Here’s the US Congressional Budget Office’s take. The CBO’s forecasts and analysis include Box 2–1 which says 70% of tariffs will be paid by consumers, 30% by US businesses and 5% by foreign exporters. The estimates across the studies vary a little but are all generally in the same ballpark.

And nobody needed these groups to tell you this. Economics 101 would have done so. Tariffs are a tax on Americans paid for by Americans and negate the advantages of last year’s tax reductions through the ‘big beautiful bill’ impacting this year’s tax refund season. Further, tariffs disproportionately impact mainstreet while the tax cuts flow disproportionately to upper income individuals with lower marginal propensities to consumer out of an added dollar of after-tax income.

US CPI One of Two Before March FOMC

How do you top nonfarm…er…Wednesday? Why US CPI Friday of course! And it’s Friday the 13th just in case we have any superstitious traders around here.

US CPI for January will be the main event to close out the week (8:30amET), at least in terms of calendar-based risk. See the preview in my weekly.

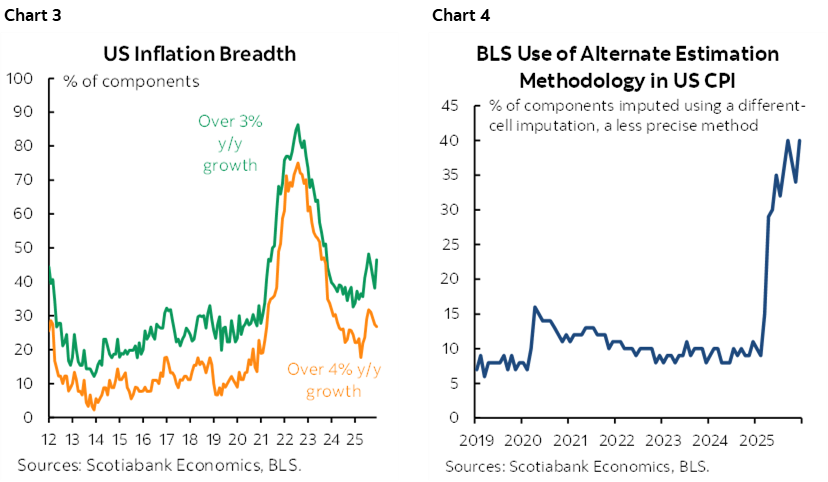

CPI is expected to rise by 0.3% m/m SA with core CPI matching that estimate. A complicating factor is that the BLS will apply updated seasonal adjustment factors in its annual exercise that stretches back five years each time they do it (here). Watch breadth as evidence mounts that more of the basket is under upward pressure (chart 3). And beware quality issues as the BLS continues to substitute proxy methods for data shortfalls with a record share of the CPI basket now being estimated by such substitute methods (chart 4).

Other Developments

Peru’s central bank held its reference rate unchanged at 4.25% last evening as widely expected. The bias sounded neutral for some time.

Russia’s central bank unexpectedly cut its key rate by 50bps to 15.5% this morning. A small minority got the call right with most expecting a hold. The central bank looked through one-off drivers of higher inflation to say “once the impact of the one-off factors fades, inflation will resume its decline.” Explicit forward rate projections indicate openness to between 100–200bps of additional cuts this year which is 50bps less than previously guided at both ends and stated it would assess the need for further cuts at following meetings. The ruble shook off the cut because of the reduced guidance.

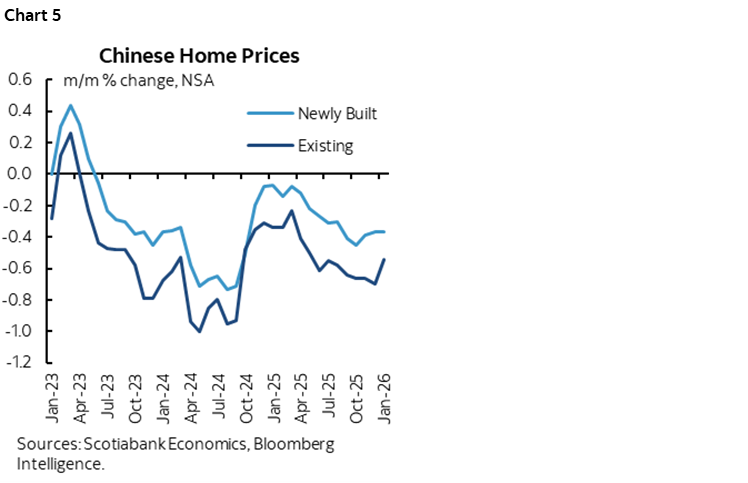

China’s house prices continued to fall. New home prices slipped by -0.4% m/m in January with resale prices down 0.5%. New home prices have fallen every single month since June 2023 with resale prices down every months since April 2023 (chart 5).

China’s aggregate financing figures for January got off to a relatively strong start compared to past months of January. New yuan loan origination was also relatively strong compared to past months of January. Comparing months of January over time is important because China tosses out its lending quotas at the start of each year and there is a seasonal rush to fill them across the individual banks. It’s too soon to tell whether this portends improved credit growth this year given one month and the seasonality.

Eurozone GDP landed on the screws at 0.3% q/q SA which drew little surprise from anyone given it was the second estimate and we already had GDP from the major economies. Jobs were up 0.2% q/q in Q4.

Canada’s bond market shuts early at 1:30pmET today ahead of Family Day on Monday. There is no official early close in Canadian equities. There is no official early close in the US ahead of Presidents Day (note plural….).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.