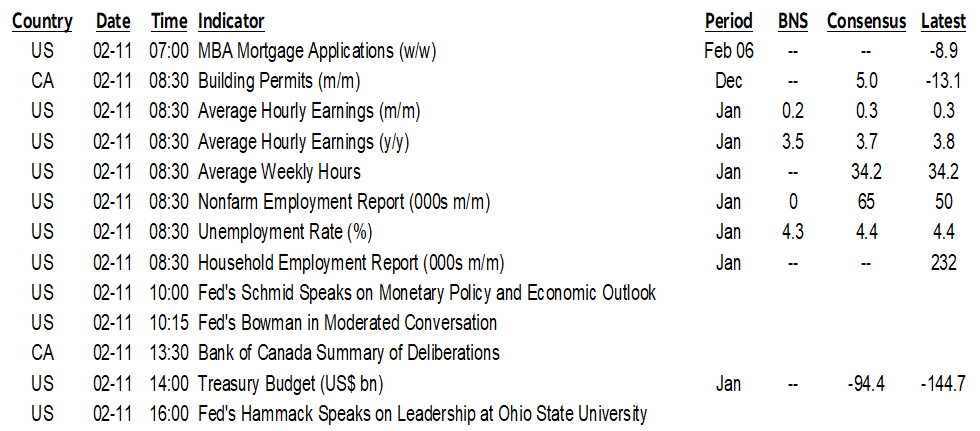

ON DECK FOR WEDNESDAY, FEBRUARY 11TH

KEY POINTS:

- Markets on cautious footings into nonfarm

- Nonfarm payroll expectations…

- ….and it’s clear that tariffs and broad policy uncertainty have quashed US job growth

- The GOP’s performative tariff vote will be quickly vetoed

- Rumoured USMCA withdrawal is a baseless negotiating ploy

- China’s core CPI signals persistently low inflation

Finally. Welcome to nonfarm…err…Wednesday?! The delayed report lands this morning as the dominant meaningful development.

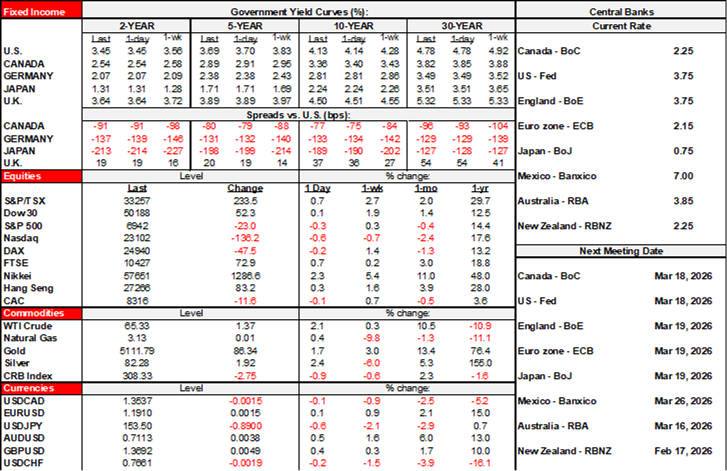

Markets are going into the reading on cautious footings. Stocks are flat to lower across US futures and European cash markets with just Toronto and London the exceptions. The dollar is broadly softer against the majors but CAD got dented by the USMCA rumour (see below). US Ts are little changed and ditto for most bond markets with the notable exception of the antipodeans. Cyber currencies are tumbling. Gold is up by over 1%, silver 6%, and oil over 1%.

PAYROLLS—EXPECTATIONS AND POLICY DRIVERS

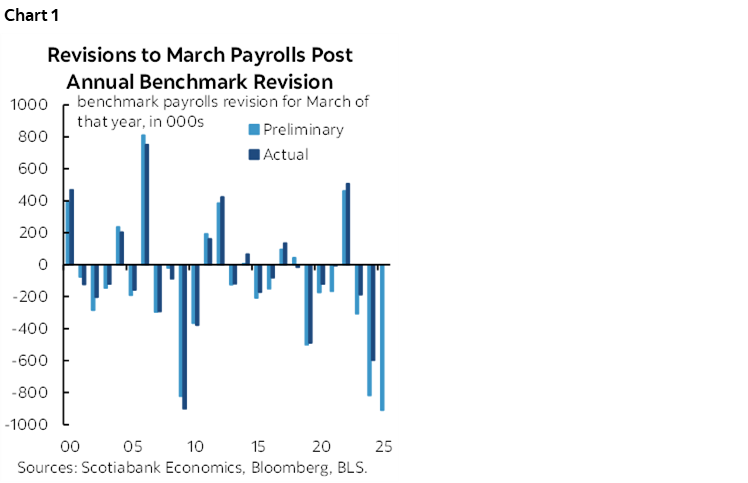

Estimates for nonfarm payrolls for January (8:30amET) are clustered within 30k to 100k or so and with a few outliers in the upper and lower tails. I’m one of them at 0k and the opposite tail has votes over 100k. The 90% confidence band on the estimated change in payrolls is about +/-136k. I won’t go over the ingredients to the murky soup again. See here and here for detailed views. Recall that this one will officially incorporate final annual benchmark revisions to last March’s payrolls after last September’s preliminary -911,000 markdown; the final revisions can deviate (chart 1). This one also includes tweaks to birth-death models.

Let’s just get the report over with after yet another delay and then onto Friday’s CPI. Then we’ll await another round of jobs and inflation readings before the March FOMC meeting. The two rounds of readings still leave the March decision in data dependent mode.

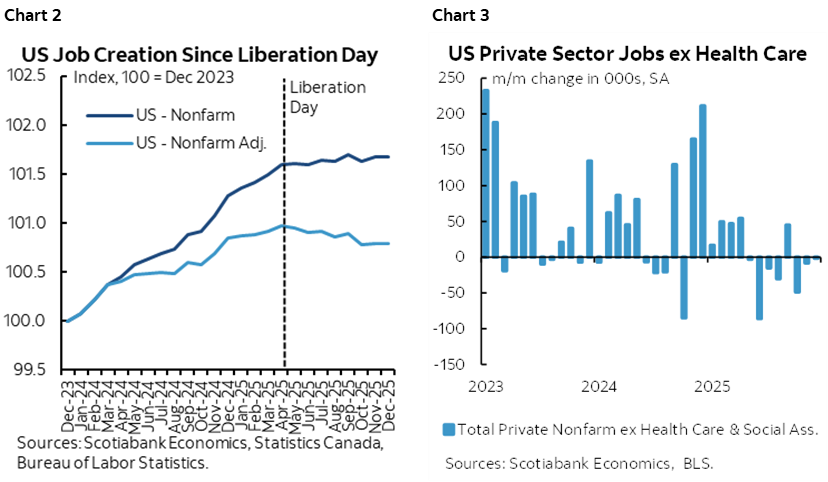

As for what is driving trend softness in nonfarm payrolls, I’ll repeat chart 2. It’s no coincidence that payrolls were on a clearly upward trend before the April 2nd ‘Liberation Day’ and then went flat. The chart also shows what incorporation of estimated revisions—including today’s March revisions and subsequently—would do to the trend by pivoting it lower. Private payrolls ex-health care have been falling in six of the past eight readings, were flat in one, and up in just one (chart 3). Take a hint—it’s the uncertainty brought on by erratic policy that has slammed hiring confidence more than any other single contributing factor.

OTHER DEVELOPMENTS

Absent a rumour, start one. Today’s is from Bloomberg that says Trump is quietly considering withdrawal from the USMCA trade pact. It’s a baseless negotiating ploy. I can think of dumber things to do when down in the polls and roiling supply chains and markets, but it’s a pretty short list. Further, he doesn’t necessarily have such powers as the chain of events to delivering a six-month withdrawal letter gets complicated in terms of pushback by the US business lobby, Congress and perhaps all the way to the Supreme Court. Treat with high scepticism in the wake of numerous other empty threats. You’re going to get a lot of this volatility on the path to negotiations.

A US House vote against Trump’s tariffs this afternoon is expected to pass with a few GOP defections—and a whole lot of complicit GOP enablers—but it’s merely a performative stunt; Trump will veto it in a hurry.

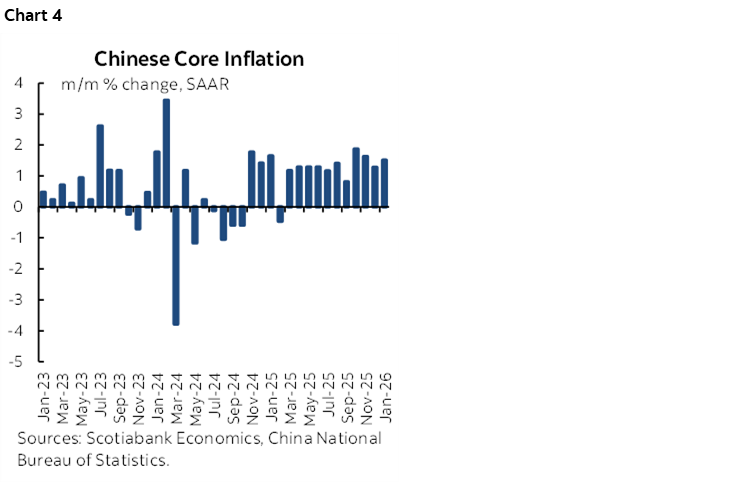

China’s CPI reading ebbed again to 0.2% y/y (0.8% prior, 0.4% consensus) with core CPI also slipped to 0.8% y/y (1.2% prior). The annualized and seasonally adjusted change in core prices is still holding around just north of 1% which is soft inflation, not deflation (chart 4).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.