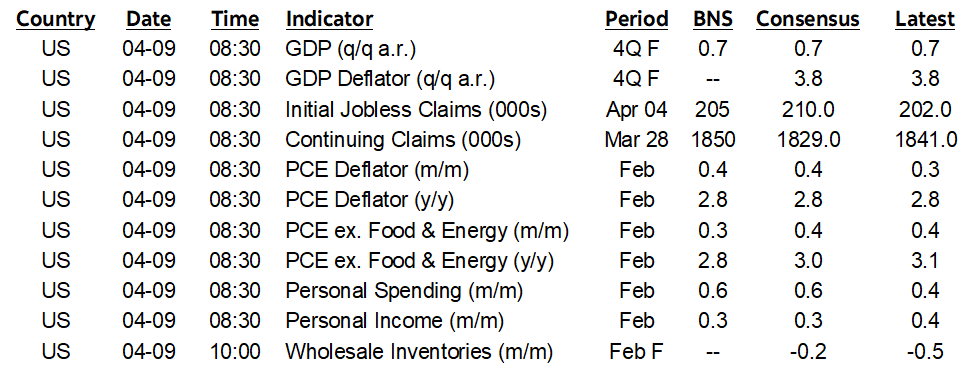

ON DECK FOR THURSDAY, APRIL 9th

KEY POINTS:

- Global markets had their fun, return to reality today

- Here’s the evidence behind how the fragile ceasefire is already in tatters

- US releases income, spending, PCE and GDP revisions

- Mexican CPI to jump ahead of Banxico minutes

- BCRP expected to stay on hold

- Germany’s mixed readings

Markets had their fun yesterday. Today it’s back to reality. Position covering drove exaggerated market responses to the fragile US-Iran ceasefire yesterday. It was only a matter of hours before doubts crept back into markets.

Oil is up about US$4–5/barrel. Stocks are broadly but gently lower with N.A. futures down about ¼%, European cash markets down by -¼% to 1¼% after Asian equities backpedalled. Currencies are mixed. Sovereign bond yields are higher by single digits across gilts and EGBs as US Ts and Canadian govies hold firm.

A Fragile Truce Became Imperilled Only Hours After Agreement

What doubts are driving these market moves? Maybe pour another coffee, the list is long.

Iran’s Speaker of its Parliament declared the ceasefire over in yesterday’s post just hours after it began. Iran insists upon the right to enrich uranium as indicated by the Speaker’s remark and by comments by the head of the Atomic Energy Organization of Iran. Trump delivered another high schoolish post. Israel keeps bombarding Lebanon and Israeli PM Netanyahu insists upon the right to continue hitting Hezbollah which violates one of Iran’s demands even if that’s a.o.k. in the minds of others. US VP Vance declared Lebanon isn’t part of the agreement. The Strait of Hormuz isn’t unblocked as of yet as ship captains say ‘you first’ to each other amid reports the Strait has been mined. Iran reportedly approached Russia about restarting nuclear research. Trump whined about NATO again, repeating his line it’s never there for the US despite having been there after 9/11 and fighting side by side in Afghanistan, despite the fact Article 25 wasn’t triggered this time, and despite the argument that NATO isn’t designed to behave like groupies on a hegemon’s world tour with next feared stops being Greenland, Cuba, Canada, etc, and despite the lost goodwill with allies on multiple counts.

Well, there you go, it’s all going just peachily. If you want evidence of next moves, then once again, watch Polymarket for the corrupt actions of insiders as per yesterday’s fresh evidence while regulators drag their heels on what to do about it.

All the while Russia lurks in the background. It has been an agitator during the conflict. Putin’s economy is driven by war and oil with the latter funding the former and therefore anything that keeps oil prices high but without causing a global recession is likely very desirable to him. Putin's whole modus operandi is to destabilize the west, NATO, the US economy and political system etc. I don't really think Iran has fundamental interest in peace, nor does Israel, and all it takes is a false flag planted by Putin to blow it all open again while Trump treats him as a trusted friend for reasons we may never know.

US Macro Readings on Tap

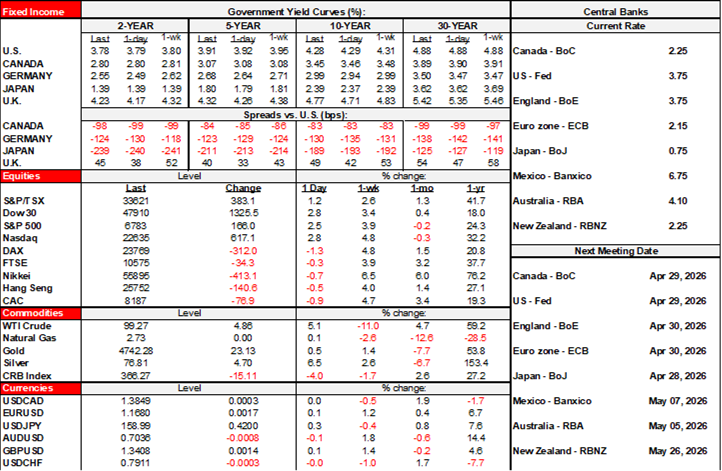

Stale data is very likely to play a backseat role to developments in the Iran war. Data might marginally matter by tomorrow when we get US CPI for March as a first indication of the war’s effects and Canadian jobs for March.

On tap into the N.A. session will be several US readings all at 8:30amET.

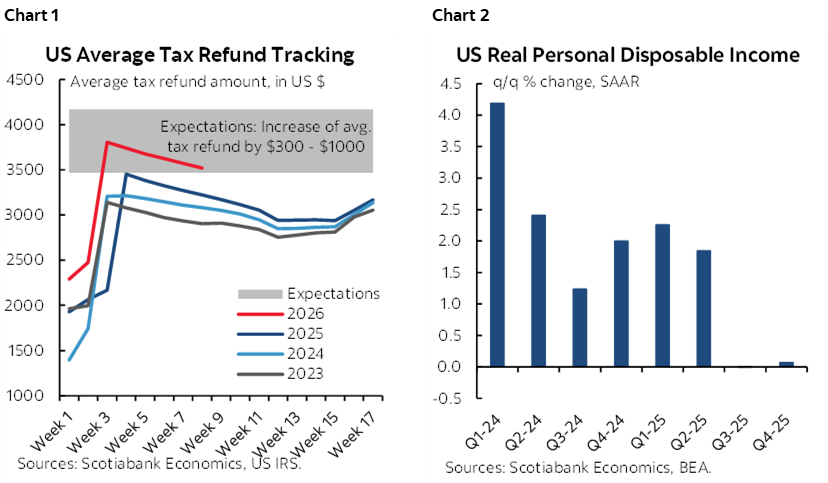

- US personal income (February): A decent gain of 0.3% m/m is expected. Being February, there won’t be much effect from tax refunds that continue to track at the low end of the range of expectations (chart 1). The figures will also aid our ability to update Q1 tracking of income growth after the US economy posted zero income growth in Q3 and Q4 (chart 2) while nonfarm payrolls ex-health trended lower.

- US personal spending (February): Spending probably surged given that we already know that the retail sales control group that feeds into the report was up 0.5% m/m and that spending on services probably offered an additional boost.

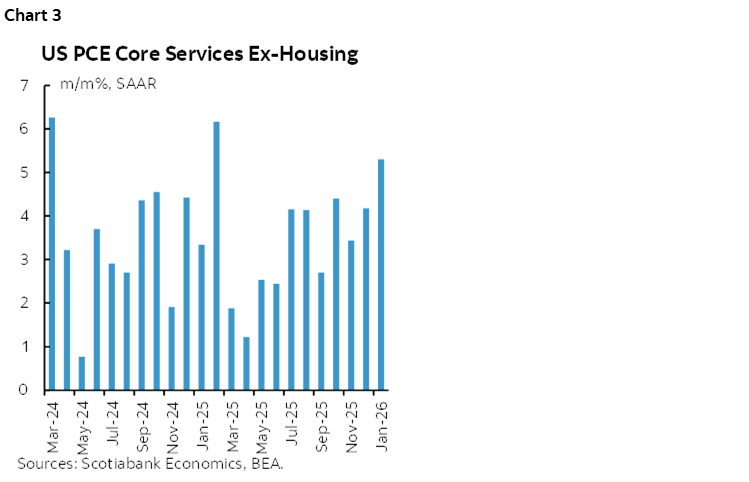

- US PCE (February): I went with a rise of 0.4% m/m for headline inflation and 0.3% for core PCE inflation ex-food and energy. Markets will likely fade it as pre-war nostalgia. Still, it remains valid to observe that the US had not licked its inflation problem before the war (chart 3) and that the war only compounds the challenges.

- US weekly initial/continuing claims are likely to continue to be reasonably well behaved into the start of April.

- US Q4 GDP-r 3rd estimate: No change to the prior weak estimate of 0.7% q/q SAAR is expected but the risk is focused upon translating the quarterly services spending report from the Census Bureau into what it means for services GDP.

- US Q4 core PCE 3rd estimate: No change is expected to the prior 2.7% q/q SAAR estimate and if you think February PCE is stale on arrival then this one has that beat.

Other Data

German data was mixed as exports soared in February (3.6% m/m, consensus 1.3%) after upward revisions, and industrial production whiffed (-0.3% m/m, consensus 0.7%) albeit largely due to upward revisions. Spanish factories also disappointed (-0.1% m/m, consensus +0.2%) with negative revisions.

LatAm markets will get a couple of things to consider today. Mexican CPI (8amET) is expected to spike in the early read on the war’s effects on prices during March. Minutes to Banxico’s meeting that led to the controversial 25bps cut on March 26th will be released at 11amET. Then Peru’s central bank is widely expected to stay on hold at 4.25% this evening (7pmET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.