ON DECK FOR WEDNESDAY, APRIL 8th

KEY POINTS:

- It’s the (almost) everything rally after US-Iran ceasefire agreement

- Iran’s 10-point plan is a rather rich set of demands. Here it is.

- Trump backed off yet another threat but this is a welcome, near-term positive…

- …while nevertheless achieving little to nothing and raising longer-term risks

- Oil futures remain highly skeptical

- FOMC minutes to discuss alternative scenarios, symmetrical bias

- RBNZ holds with hawkish bias that reinforced hike pricing this year

- RBI held with neutral bias in defence of the rupee

- Japanese Shunto wage growth posted another strong year

- Japanese real wages accelerate

- German factory orders disappoint

- Taiwan extends undershoot of March CPI expectations across small markets

Trump stood down from yet another threat and agreed to a two-week ceasefire with Iran last evening that is to result in negotiations starting on Friday to end hostilities. Trump’s announcement on social media last evening is here. The announcement by Iran’s Foreign Minister is here. The state media broadcaster followed up by saying this doesn’t mean the end to war and that distrust will prevail. Iran’s President Pezeshkian boasted that “acceptance of Iran’s general principles is the fruit of the blood of our martyred leader, the great Khamenei.” Iran continued to attack neighbours overnight including waves of drone and missile attacks on Kuwait and UAE. There remain many questions and uncertainties on the path forward.

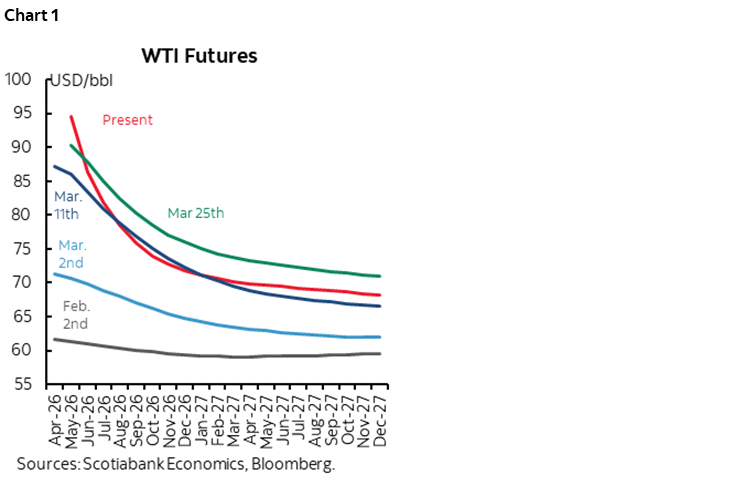

But for now, it’s the everything rally—except for commodities. Position covering may be amplifying the swings and driving somewhat of an overreaction. Oil prices are volatile but sharply lower by double digit percentages although the futures curve remains elevated at sustainably higher prices throughout 2026–27 than the spot prices back at the start of the year (chart 1). That clearly signals market concern toward a) the possible fragility of the ceasefire amid uncertain negotiations, and b) the longer-term damage to geopolitical risk premia and infrastructure. Stocks are broadly higher with NA futures up by about 2–3%, European stocks are up by 3–5%, and Asia-Pacific benchmarks rallied by 3–7% across the main benchmarks. Sovereign bond yields are broadly lower with EGBs outperforming via declines of 20–30bps across maturities and countries, while US Ts are rallying by ‘just’ 5–7bps, and Canadian govies are dearer by 10bps at the front end in a bull steepener. The dollar is broadly weaker albeit with CAD slightly underperforming other crosses due to lower oil.

Trump accepted Iran’s 10-point plan as a starting point for negotiations. Here it is:

- A guarantee that Iran will not be attacked again

- A permanent end to the war, not just a ceasefire

- An end to Israeli strikes in Lebanon and against Iranian allies

- The lifting of all US sanctions on Iran

- Iran agreeing to reopen the Strait of Hormuz

- A $2 million fee per ship transiting Hormuz

- Revenue from shipping fees to be shared with Oman

- Funds to be used for reconstruction of war-damaged infrastructure

- Establishment of safe passage protocols through Hormuz

- A broader framework to end regional hostilities

That’s an ambitious wish list and colour me highly skeptical. Iran should know that Trump’s guarantees are worthless. Iran should know that the US cannot control Israel. Lifting all sanctions against Iran is a stretch to say the least. We’ll see if the Saudis and UAE agree to Iran controlling the strait and charging fees to be shared with Oman while Kuwait demanded this morning that free navigation must be guaranteed. The impact of the fees on the price of oil is likely to be de minimis but perhaps slightly more for lower valued commodities transiting the strait. Using the funds to rebuild Iran—if agreed upon—would need serious guardrails against going into the armed forces and nuclear research program or being pocketed by a regime that has only become more corrupt than even before.

Also note what’s not in the 10-point plan. There was no mention of handing over enriched uranium stockpiles, ending its nuclear program, and submitting to international inspections. Trump said this morning that they will address nuclear stockpiles and enrichment but a) that assumes the US knows where Iran moved and hid it all, and b) assumes that Iran will comply and honour any such agreement after not submitting to the demands in its 10 points. Trump also noted that tariffs of 50% would be applied against countries supplying weapons to Iran, but a) Russia is already penalized and couldn’t care less, and b) Iran will get back to work building more drones and missiles of its own.

All of which leads one to question exactly what was accomplished from war. The Iranian regime is in tatters but still in place. The nuclear stockpiles and program remain and it’s not at all clear what happens to them going forward. Iran may have actually managed to strengthen control of the Strait of Hormuz. Long-term damage to regional energy and broader infrastructure will take months to years to repair. The geopolitical risk premium attached to multiple commodity prices is probably permanently higher. The whole region is much more divided than previously. The Trump administration and broader US reputation among allies and foes has suffered a further erosion of any credibility it may have still had. Frankly, it’s hard not to see Iran as the victor and I worry that a brutal Iranian regime and its terrorist network will rebuild and become a greater and angrier threat within an even more divided region and abroad.

There is also a repeated lesson that is portable across other fronts too—standing up to Trump bears more fruit than cowering and giving in. I've always been of that mindset on trade. The Europeans and Japanese were novices in dealing with Trump on trade matters and unwisely capitulated. China did not. Canada and Mexico should not either.

But the clear positive is that major escalation with unknown risks including outside of the region was averted. The market aftermath to a major escalation could have been disastrous. Attacking civilian infrastructure in Iran could well have ended the Trump presidency and ultimately led to a trip to The Hague.

OTHER DEVELOPMENTS

Clearly the truce dominates market attention but there were a few other notables on the overnight docket into today’s line-up.

Minutes to the March 17th–18th FOMC meeting arrive at 2pmET. A recap of the decision and communications is here. Watch for discussion of alternative scenarios to the base case Summary of Economic Projections that Chair Powell referenced in his press conference. Also watch for discussion around the possibility of a rate increase after Powell noted that the vast majority did not have that as their base case and that’s why they did not introduce a more clearly symmetrical policy bias; clearly the signal is that at least one was pushing for openness toward hiking.

The RBNZ held at 2.25% as universally expected but delivered a hawkish sounding bias that motivated markets to add a little more to pricing for a July hike with ¾% of cumulative hikes priced by year-end. Governor Breman flagged discussion of “a relatively early” rate increase but downplayed the prospects while the RBNZ’s forecasts raised the inflation outlook. The statement noted:

“If the increase in near-term inflation is largely temporary, the Committee envisages gradually moving the OCR to more neutral levels as activity recovers and near-term inflationary pressures dissipate. However, any signs of significant second-round inflationary effects or increases in medium-term inflation expectations would require decisive and timely increases in the OCR to re-anchor inflation expectations. The Committee is vigilant to these risks.”

The RBI held at 5.25% as universally expected. The broad tone shifted toward a neutral stance away from a previously dovish slant and focused upon stabilizing the rupee in the face of an inflation threat.

Japanese real wages jumped to 1.9% y/y in February (1.3% consensus) and were revised sharply lower the prior month. The preliminary estimate of Shunto spring wage negotiations yielded a gain of 5.3% y/y this year which extends the multi-year pattern (chart 2).

German factory orders grew by much less than expected at 0.9% m/m (3% consensus) following the massive 11.1% m/m drop the prior month.

Taiwan’s CPI inflation came in softer than expected in March (1.2% y/y, 1.6% consensus) which extends the small country pattern from the prior day.

Chile CPI for March will arrive at 8amET and is expected to jump by 0.9% m/m.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.