ON DECK FOR MONDAY, APRIL 6th

KEY POINTS:

- Rumours and unglued threats dominate thin market activity...

- ... as most markets remain shut...

- ...and haven't even reacted to nonfarm as yet...

- ..that was an entirely weather-driven gain

- US ISM-services, Canadian PMIs on tap

- Global Week Ahead highlights

Most global markets remain shut for Easter Monday. US and Canadian equity futures are flat to very slightly positive after the Nikkei posted a mild ½% gain overnight. Sovereign bonds are little changed with a mild cheapening bias that has Canadian govies underperforming US Treasuries partly as they catch up to US payrolls after Canada was shut on Friday. Oil prices are slightly lower by 1% or less. Most major currencies are appreciating a touch versus the USD. Europe is closed.

Many global markets have yet to be able to react to Friday's stale and distorted US nonfarm payrolls report (recap here); they'll get a first crack at doing so tonight into the Asian market open and into Europe’s open.

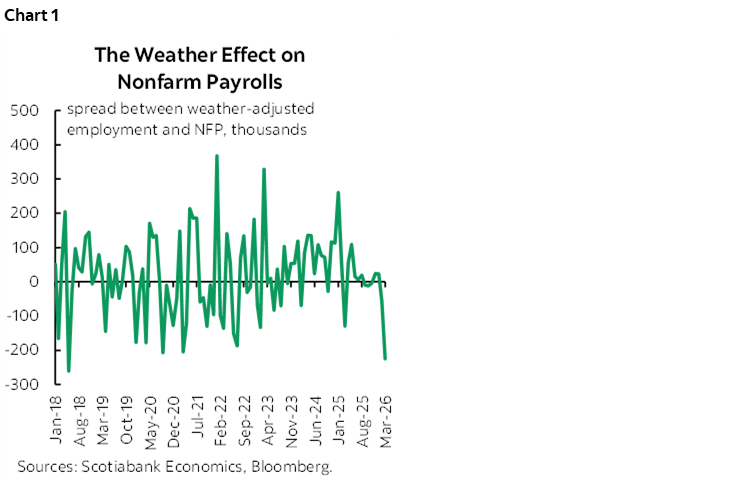

Stale is obvious, but why distorted? The folks at the San Francisco Fed estimate that the 178k gain would have been a loss of 47k if not for weather effects (here). Chart 1 shows that this 225k weather effect was among the largest estimated weather effects in history and follows a positive weather contribution to February's payrolls of over 50k. Underlying hiring in the US economy remains in a troubled state.

In the context of thin global market activity this morning alongside lagging reactions to nonfarm and no useful macro reports, what we’re left with to consider are threats, deadlines and the rumour mill that is swinging sentiment in the few markets that are trading this morning.

This and this are hardly PG friendly from America's President. I wish I could say nothing shocks me about this man by this point. After cutting through the vulgarities that at one time were beneath a President what we're left with is the threat around tomorrow evening's deadline for Iran to open the Strait of Hormuz or else civilian infrastructure will be bombed. What’s good for the goose is good for the gander is the obvious concern in reverse. Trump speaks again today at 1pmET.

Absent a rumour, start one. Axios is doing so with a plant by those always trustworthy 'anonymous'' sources about a low probability chance at a deal to avert further escalation of the war with Iran. That’s why oil is off a bit this morning. Iran countered by saying “A ceasefire means creating a short pause to regroup and commit crime again and no rational personal would do that” and went on to demand “assurance that this cycle will not repeat.” Iran then launched more missiles at Israel this morning. If deescalation is in order, then it would probably have to be in the form of another fake deadline set by Trump.

MINOR DATA ON TAP

The US releases ISM-services for March this morning (10amET). Consensus expects a softer reading (54.9 from 56.1 prior). Watch the prices paid measure that is likely to skyrocket as a first take on the war’s effects.

Canada updates S&P PMIs for Mach (9:30amET). The manufacturing PMI was released last week and dipped a point to 50.0. This morning’s releases will include the services and composite gauges.

GLOBAL WEEK AHEAD HIGHLIGHTS

Here are highlights of what to expect this week In lieu of a formal week ahead publication because I was meeting with clients in London, Paris and Lisbon last week.

CANADA—A Jobs Rebound?

The main focus in Canada will be upon Friday's jobs report for March.

Consensus sits at a gain of 15k (Scotia 30k) with the unemployment rate’s prior reading of 6.7% facing a divided perspective as the median call is for an uptick to 6.8% (Scotia 6.6%). Many estimates have yet to be inputted into Bloomberg’s survey.

UNITED STATES—A First Take on March Inflation

In a mixture of predominantly stale data one report may stand out a tad more than the others.

US CPI (Friday) will offer a very tentative take on how the war against Iran by Israel and the US impacted inflation during March. CPI is estimated to rise by 1% m/m SA and 3.4% y/y (2.4% prior). Core CPI is estimated to rise by 0.3% m/m and 2.7% y/y (2.5% prior).

It's a first stab for two reasons. One is that the fuller effects—including transmission into core inflation—will take many reports to properly assess as residual inflation pressures from an economy in excess aggregate demand still dealing with tariff pass through transitions toward evaluating how much of the diversified spike in commodity prices will be passed on. Two is that data quality issues at the BLS have lowered faith in the readings due to heavy budget cuts but also a multi-year failure by the agency to pivot toward alternative data collection tactics.

Other data is likely to be stale in a pre-war sense:

- durable goods orders (Tuesday): February’s reading is expected to drop by 1% m/m SA (-1.5% Scotia) on transportation orders but ex-transportation is forecast to rise by 0.4% m/m.

- FOMC minutes (Wednesday): The minutes to the March 17th–18th FOMC meetings will probably have little to offer markets that are pricing a hold until well into next year at the moment. That may change if the commodities shock wallops growth and nonfarm, but time and data will inform that perspective.

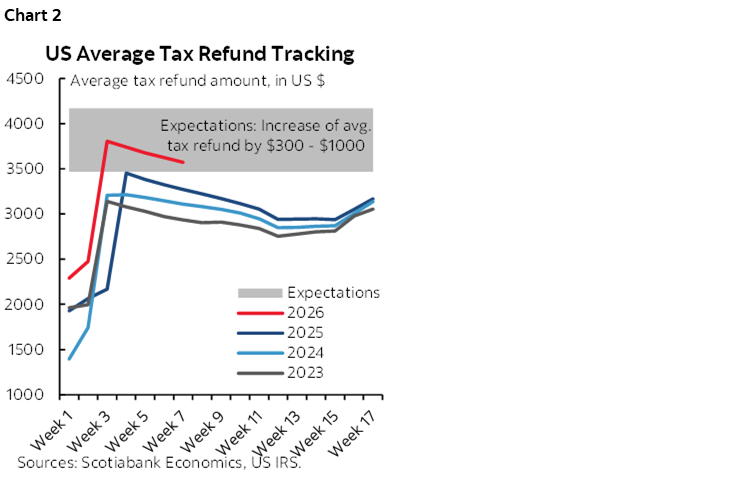

- Personal incomes and spending (Thursday): February’s income growth is likely to grow less than previously envisaged as tax refunds continue to track lower than expected (chart 2). Spending, however, could get a boost from the retail sales control group that was up by 0.5% m/m SA in nominal terms which often serves as a decent guide to total spending.

- PCE inflation (Thursday): February’s reading will take a back seat to the next day’s fresher CPI readings for March.

- Jobless claims (Thursday): Tighter rules in this cycle are expected to keep claims reasonably well behaved.

- Q4 GDP-r (Thursday): The third swing at estimating Q4 GDP growth is not expected to change the prior 0.7% q/q SAAR reading that demonstrated weak GDP growth. A fuller take on services spending is always a risk at this stage.

- Core PCE-r Q4 (Thursday): Q4’s reading of 2.7% q/q SAAR is expected to be unchanged in this revision.

- real wages (Friday): March’s reading is likely to fall as the inflation shock erodes inflation-adjusted pay.

- factory orders (Friday): February’s reading depends on Tuesday’s durables report plus estimated changes in orders for nondurable goods.

- UMich (Friday): April’s consumer sentiment print is widely expected to weaken on war effects.

ASIA-PACIFIC—RBI, BoK, Inflation Reports

Three central bank decisions are likely to stand out amid several inflation readings for March.

The RBNZ is widely expected to hold its official cash rate unchanged at 2.25% tomorrow evening. Markets agree.

The Reserve Bank of India is unanimously expected within consensus to hold its repurchase rate unchanged at 5.25% on Wednesday but markets lean toward the chance at a hike.

The Bank of Korea (Friday) is unanimously expected to hold its base rate unchanged at 2.5% with market pricing onside.

CPI reports for March will provide initial estimates of the war’s effects in the Philippines (Monday night), Thailand (Monday night), Taiwan (Wednesday) and China (Thursday).

LATIN AMERICA—Peru’s CB, Inflation Reports

A single central bank decision and a few March inflation readings could add some spice to more dominant war themes.

Peru’s central bank is unanimously expected to stay on hold at 4.25% on Thursday evening.

March CPI will offer insights into war-related price pressures in Chile (Wednesday), Mexico and Colombia (Thursday), and Brazil (Friday).

EUROPE—War Watching

European markets will mostly observe developments elsewhere this week. There just isn’t anything that will grab you on the release calendar because it’s mostly stale and second-tier data.

Mild exceptions include Swedish CPI (Tuesday) and GDP (Friday) for Riksbank watchers, and Norwegian CPI for Norges Bank watchers (Friday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.