ON DECK FOR THURSDAY, APRIL 30th

KEY POINTS:

- Yen takes flight on stronger intervention signal

- ECB — Waiting for June

- BoE holds, delivers three scenarios ranging from no hike to +150bps

- Canada to update Q1 GDP tracking

- US Q1 GDP growth was probably strong due to government rebound

- Eurozone economy stalls

- Eurozone CPI inflation lands on expectations

- China’s PMIs softened, led by services

- BanRep to hike

- BCB cut

- Apple earnings in the after-market

- Why the cut ship has sailed for the BoC

The yen is the star pupil this morning as it’s leading a wave of anti-dollar sentiment across the majors. The driver is Japan’s FinMin Katayama who said the window “for taking bold steps is now nearing” in reference to intervention—perhaps coordinated—against yen weakness. Longer dated JGBs are underperforming in bear steepener fashion but partly because Asia-Pacific markets in general followed yesterday’s N.A. rates sell off that was driven by oil, inflation worries and the Fed.

Oil is treading water for the most part this morning after yesterday’s surge. Markets are waiting for clear signs on next steps as Iran and the US dig in. Sovereign yields are under downward pressure in the US, UK and Eurozone with the ECB pending after the BoE held. Equities are mixed with a sea of small gains and losses across N.A. futures and European cash.

MORE CENTRAL BANKS—A CUT, A HIKE, AND TWO HOLDS

We have four central banks to consider in chronological order with more views offered in last Friday’s weekly (here).

Brazil’s central bank cut the Selic rate by 25bps as expected last evening. The statement flagged recent upside to inflation measures and

The Bank of England held Bank Rate at 3.75% as widely expected in an 8–1 vote with Chief Economist Pill dissenting in favour of a hike at this meeting (statement here). The central bank abandoned base case projections in favour of three scenarios that indicate varying amounts of potential second-round effects of higher commodity prices into broader prices. Those scenarios imply anywhere from no hikes to 150bps of tightening. Clearly the message is that the BoE is watching for second-round effects in addition to assessing the longevity and magnitude of the commodity shock. Markets reacted by pushed the 2-year UK yield down a few basis points and trimming a little from June hike pricing that is now roughly two-thirds priced for +25bps.

The ECB is next up with an expected and priced hold at 2% (8:15amET) followed by President Lagarde’s press conference at 8:45amET. This meeting should have a air of waiting for June around it. Having just produced forecasts in March, the next opportunity to issue fresh projections will come at the June meeting by which point greater information will be available.

Colombia’s BanRep is then expected to hike by 50bps to an new overnight lending rate of 11.75% (2pmET). A minority thinks BanRep could hike by 75bps.

ON TAP IN NORTH AMERICA

A blast of macro data across all three countries then gives way to Apple’s earnings in the after-market (Q2 EPS US$1.96).

Mexican Q1 GDP is expected to contract by -0.6% q/q SA nonannualized, making it two drops in the latest three quarters.

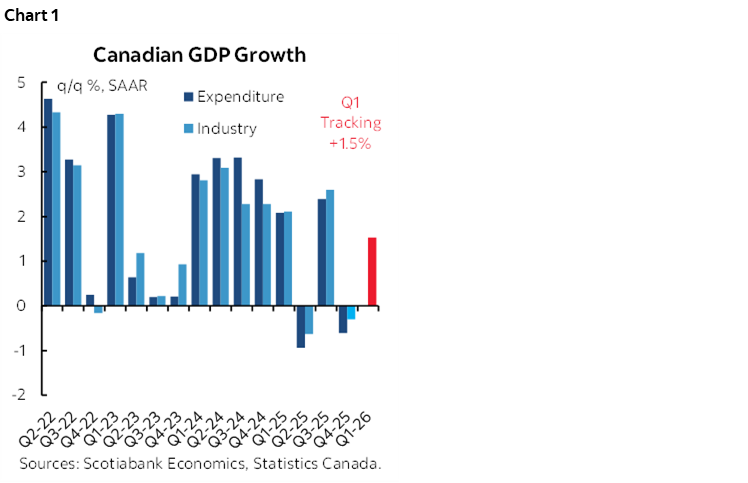

Canada’s economy likely posted modest growth in February (0.2% m/m SA) given advance guidance from StatCan and our tracking, and we’ll get sector details (8:30amET). Key, however, may be March GDP for which there has been very little data and which serves as an important contribution to tracking Q1 overall and to hand-off math into Q2 GDP. Q1 GDP is tracking 1.5 to as much as over 2% q/q SAAR (chart 1).

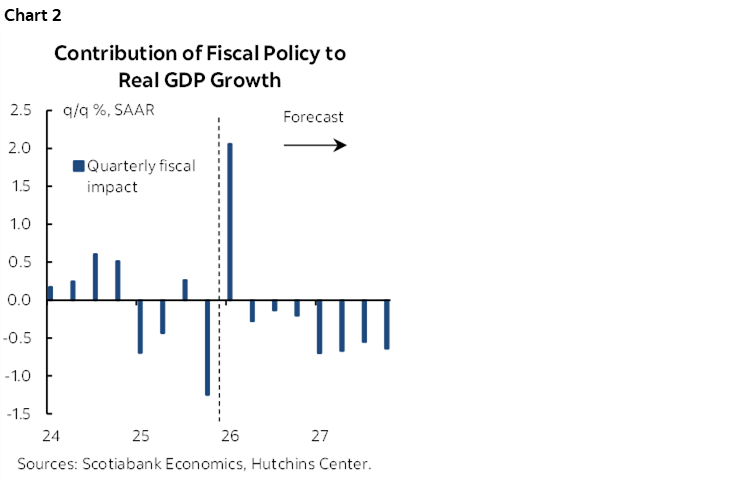

The US economy probably posted strong headline growth but weakness under the hood. Q1 GDP is expected to be up by 2.3% q/q SAAR (Scotia 3%) largely due to the rebound in government from the prior quarter’s shutdown (8:30amET). Excluding what could be around a two percentage point contribution to GDP growth from government (chart 2), the rest of the economy including the consumer was probably quite weak.

The US also updates consumer spending and incomes as well as the Fed’s preferred inflation measures during March. Nominal spending is expected to be strong with a gain near 1% m/m SA based on prices and retail figures, while income growth is expected to be more muted (0.3% m/m, Scotia 0.5%). Core PCE inflation is estimated to have risen by 0.3% m/m SA after a string of 0.3–0.4% nonannualized readings that were tracking in the 4–5% m/m SAAR range.

Employment costs could also garner some attention. The US Employment Cost Index for Q1 is estimated to rise by 0.8% q/q SA nonannualized (8:30amET).

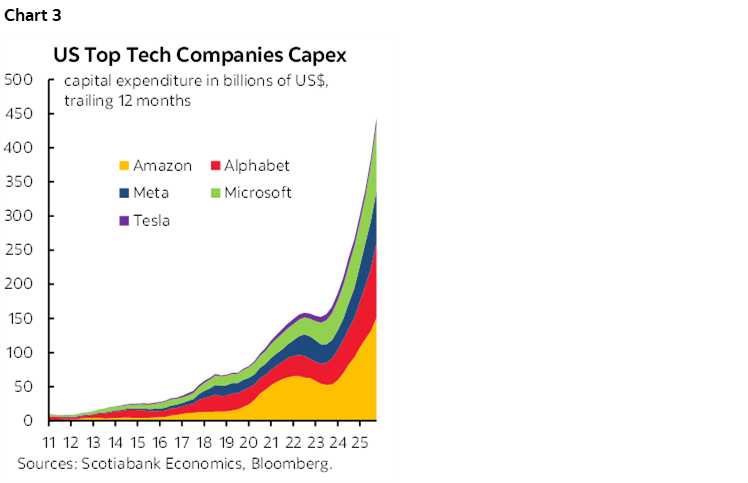

Watch for Apple’s tech spending to be added to chart 3 that incorporates updated cap-ex plans from the other tech players that released earnings last evening.

OVERNIGHT MACRO REPORTS

China’s state PMIs were little changed with the composite reading dipping by 0.4 to 50.1. That was due to a 0.7 decline in the non-manufacturing PMI to 49.4 and hence mildly tip toeing into contraction territory. The manufacturing PMI remains above the critical 50 threshold at 50.3.

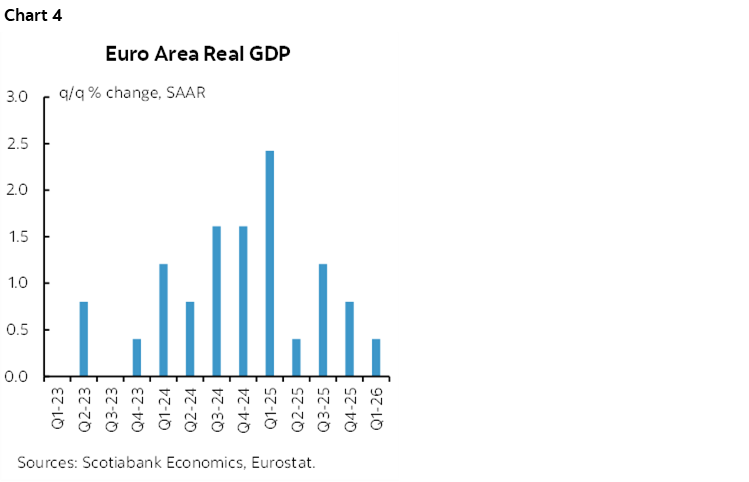

Eurozone GDP disappointed and nearly stalled out in Q1 ahead of further downside risk that lies ahead (chart 4). GDP was up by 0.1% q/q SA nonannualized (0.2% consensus), bringing the year-over-year rate down to 0.8%. France’s economy dragged the region down (0% q/q, 0.2% consensus) while Spain (0.6% q/q SA, 0.5% consensus) and Germany (0.3% q/q, 0.1% consensus) continued to outperform. Italy grew by 0.2% q/q.

Germany’s fortunes are poorly positioned into Q2 from a consumer standpoint. That’s because retail sales volumes fell by 2% m/m SA in March, far below expectations for a nearly flat reading. That’s a weak hand-off that exerts a downward bias on tracking second quarter growth.

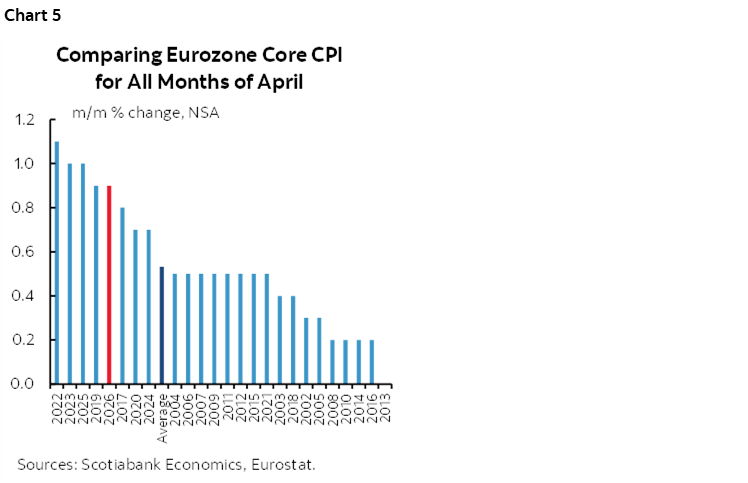

Eurozone inflation was on the screws in March, matching consensus at 3% y/y. Core CPI also matched expectations at 2.2% y/y. The month-over-month core reading in NSA terms was among the warmest on record (chart 5).

WHY THE CUT SHIP MAY HAVE SAILED FOR THE BOC

There are many reasons why the BoC shouldn’t have even been talking about rate cuts yesterday (recap here), but one that’s often missing from the debate. In a market sense, to cut 25bps would actually translate into effectively cutting by 100 or more in a heartbeat which would also sink the currency. That’s because cutting 25bps would also reverse over 60bps of priced hiking this year for a total swing factor of over 85bps. Given that markets would also likely price in further cuts after the first one, the cumulative market easing relative to pricing would amount to well over 100bps of cutting, giving it the label of the biggest quarter point cut in history. Even if you do nothing on the policy rate this year, then you’ve cut by at least 60bps and probably more because if you do nothing then markets would think you’re leaning toward easing.

The currency impact to effectively delivering over 100bps of easing would torpedo CAD, pushing it perhaps to the 1.45+ USDCAD range, raising import price inflation risk.

Easing financial conditions by this much wouldn’t make a whole lot of sense in a country that produces multiple commodities that are all on fire and without having incorporated more federal spending into BoC projections and with all of the other reasons for tightening. If you want to cut, you’d better have maximum, off-the-charts conviction that it’s the right thing to do given the turmoil and consequences that would be sparked in financial markets that the BoC too often fails to understand. Macklem’s cut scenario also violates many of his speeches on trade that speak to supply damage as well as demand hits from trade turmoil. I also still find that the pressure will be upon the Trump administration to deal on USMCA more than in Canada in a scenario marked by cautious optimism. And then there is the retaliation angle; should the US raise tariffs and torpedo USMCA, Canada would almost certainly have to respond in kind this time, thereby raising import price pressures.

Overall, I think the main reason Macklem mentioned a cut scenario as an offset to their hike scenario was to avoid markets pushing them too aggressively in the nearer term. Absent even a low credibility cut view, talking hikes would have probably pushed markets to pricing hikes starting in June.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.