ON DECK FOR WEDNESDAY, APRIL 29th

KEY POINTS:

- Oil continues to surge on US-Iran stalemate

- BoC may deliver a hawkish hold…

- ...as surging commodities and Ottawa’s spending add to rate hike risk

- FOMC to bide its time…

- …and bid adieu to Chair Powell

- US updates durables, trade and housing

- Aussie rates overreact to CPI

- EGBs largely ignored German, Spanish CPI

- Chile, BoT held…

- …BCB expected to cut

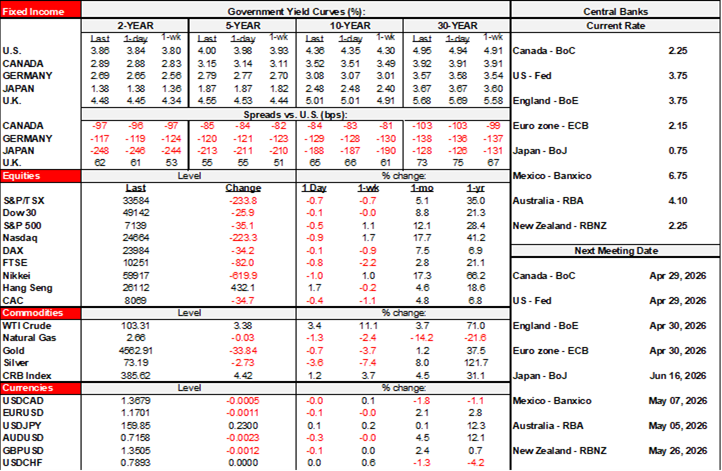

Oil is once again in the driver’s seat, posting further gains of $3+/barrel this morning. Sovereign bond yields are higher across US Ts, EGBs, gilts and Canadian bonds after Australian yields fell because of a slight miss by Q1 trimmed mean CPI (0.8% q/q, 0.9% consensus). Stocks range from flat across N.A. futures to down ½% or so across European cash markets. The dollar is broadly firmer except against the petrocurrencies like the krone and CAD.

Then it’s onto a pair of holds by the BoC and FOMC as the day’s main focus following some light US data. There is likely greater risk around the BoC’s bias and guidance than the Fed’s in Powell’s final press conference.

BOC—HAWKISH HOLD

My weekly sank a tonne of effort into providing a detailed explanation of our BoC view. There isn’t much more to add at this late stage so let’s just bring it on. The statement, MPR including fresh projections, and Governor Macklem’s written opening remarks arrive at 9:45amET and will be followed by the press conference at 10:30amET.

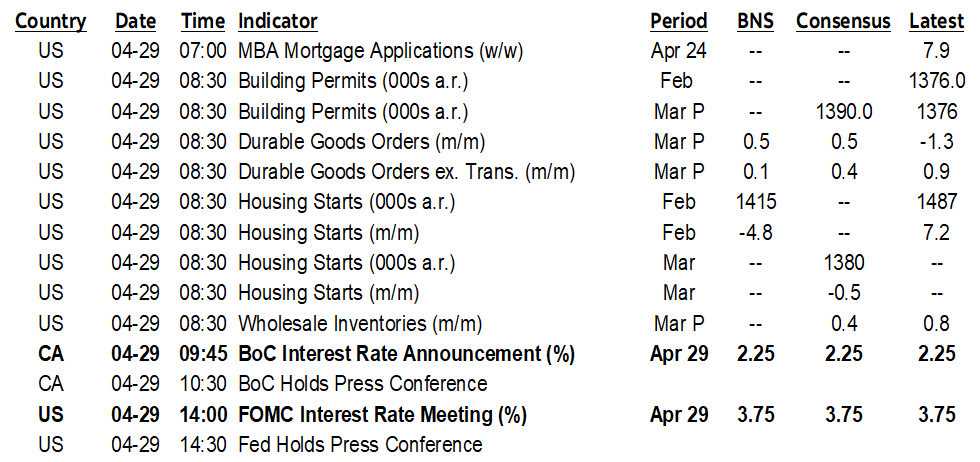

My weekly included how the BoC may adjust its forecasts in this MPR, the possible bias, the explanation of why we had hikes in our 2026 forecast dating back to last November and hence before the war and commodity shock, the added influences of the commodity shock on that view, why a risk management and insurance approach needs to be taken this time instead of waiting until the BoC has all the answers on inflation risk, and risks to the BoC’s balance sheet plans on timing GoC gross bond purchases. Doing nothing is doing something by way of passively easing as the real policy rate has sunk deeply into negative territory using any of the BoC’s expected inflation survey measures (chart 1) that haven’t even incorporated full effects of the commodity surge which is curious for a commodity-producing country in a positive commodity price shock environment.

In general, we view our rate hike projection for +75bps over 2026H2 as conservative. If they don’t follow a risk management insurance playbook, then we may be inclined to add more hikes later. It’s an opportunity to avoid blowing inflation management like the last time.

Where there is a little something extra to offer is in terms of last evening’s spendapalooza by the Carney administration.

OTTAWA’S SPENDING ADDS TO RATE HIKE RISK

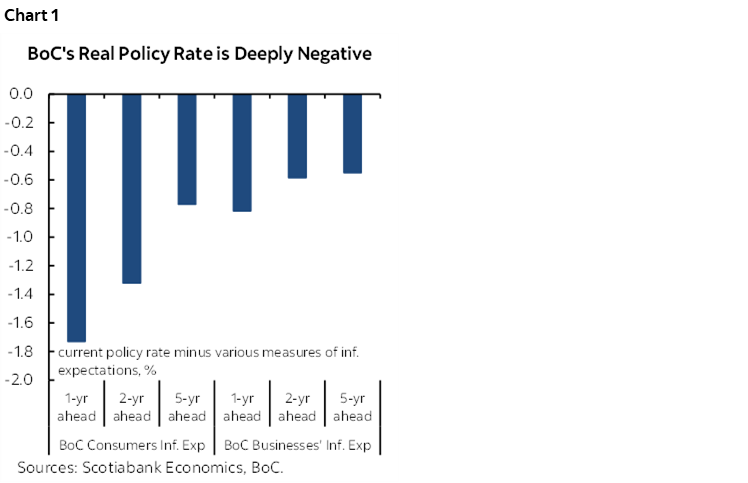

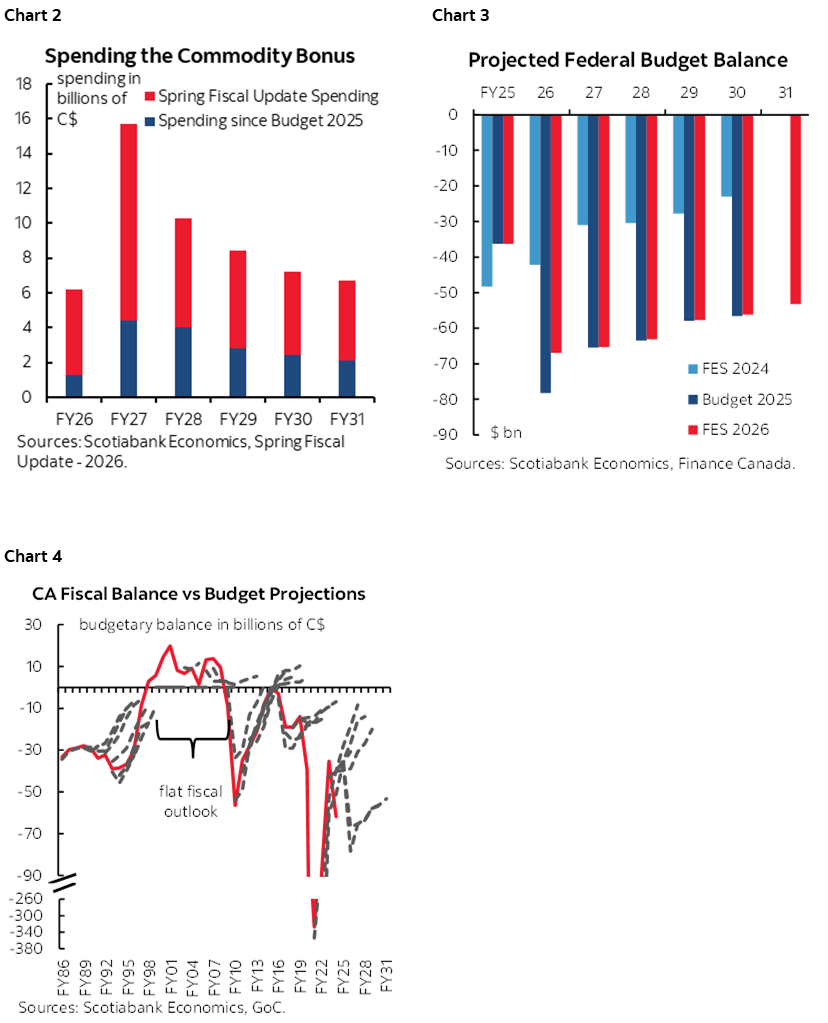

Key to the Spring fiscal update (here, here) is all of the new spending (chart 2) that slightly complicates the Bank of Canada’s policy rate path going forward in a mildly more hawkish manner. Pay little attention to the revised deficit path (chart 3) given Finance’s politicized, awful track record in terms of forecasting magnitudes and inflection points (chart 4).

Frankly, the affordability messages provided by the government were curiously inconsistent as more spending incrementally complicates the aim of getting affordability under control and risks adding to rate hike risk. It’s extra curious when the PM is a respected former central banker.

Key is that they're spending the lucky—yes lucky—bonus from commodities and a better than feared economy. A total of C$37.5 billion of new measures was added. In FY 2026–27 they're adding $11.3B of new measures on top of the $4.4B they added since the Fall Budget but before yesterday's announcements. In FY2027–28 they're adding $6.3B of new initiatives on top of adding $4.0 since the Budget but before today.

This is meaningful. We need time ourselves to crunch through the complete effects on GDP growth, potential GDP growth, multiplier effects, inflation etc. The back-of-the-envelope math provided in client chats yesterday, however, shows that incremental spending as a share of NGDP from our prior forecast round equates to 0.5% of NGDP this year and 0.3% next year.

The government is recycling the lucky fiscal dividend from commodities. This is the terms of trade impact upon fiscal policy as part of the trickle down effect on the economy. They've spent it straight through to 2030–31 with a diminishing profile, until they spend more later. It’s fiscal policy easing that could add to the merit of monetary policy tightening. The revenues they are spending are not like past tax hike effects as the revenues are being derived significantly from an imported positive income shock.

It’s also a mixed message on affordability pressures and I'll repeat a narrative I've been leaning on for a while—fiscal policy remains very much 'live' in Canada. In sequential fashion. More stimulus is being added each time they update. There will be more in the Fall Budget and probably more before then. They are somewhat straying from the initially stated goal of extending the duration of fiscal measures through less by way of nearer term measures.

And regarding details behind a new sovereign wealth fund—the Canada Strong Fund—well, there weren’t any. Why did you roll it out with haste and so little to offer on important details? They said on Monday that they’d have more details on the retail funding product they had in mind but whiffed yesterday beyond just providing more generalities like mass appeal, fixed income with principal guarantees and with an equity kicker of some sort. There was a little more provided off the record in this piece about recycling assets like airports to fund the SWF including via possible plans to privatize airports, extend their leaves, enabling development on airport lands etc.

Overall, it’s a curious set up for a sovereign wealth fund. Canada is not a net saver and therefore doesn’t satisfy the most basic criteria for having a SWF, albeit a tiny one. Selling stuff to put it in a SWF is a kid’s shell game of sorts but labelled as asset recycling. And the generalities around a retail product still sound like it will be put in competition with products already offered by traditional financial institutions. Asset managers giving advice here are trying to eat the lunch of traditional financial institutions that are offering deposit products including equity-linked GICs.

HOW WILL THE BOC REACT?

How will BoC Governor Macklem react to the Spring fiscal and economic statement? He should view it as more growth supportive and hence be slightly more concerned about inflation risk. But what he will do is unclear given his past pattern of behaviour.

Obviously the BoC can't incorporate new announcements today into their forecasts and MPR which has been put to bed for a while now. It was frankly inappropriate of the Carney administration to announce its update literally hours before the BoC weighs in.

Macklem will not make overly strong remarks and will not critique fiscal policy. That’s not the way it works, especially in Canada.

He may offer a general opinion on first blush during the presser. A potential question could simply ask if he thinks it’s more growth supportive relative to the numbers they just published. And it is.

Or he could simply pass and defer by saying they need to look at it thoroughly and incorporate into future projections. That would be more in line with his past pattern of behaviour; didn’t see that, don’t want to, will get back to you.

FOMC PREVIEW—PLACEHOLDER AND BIDDING ADIEU

See my weekly for the FOMC preview which was relatively light this time because this meeting is frankly just a calendar placeholder at a transition time for the leadership. The statement arrives at 2pmET and Chair Powell’s final press conference will start at 2:30pmET. There will be no Summary of Economic Projections or dots with this one after presenting them in March and with the next round to have Warsh’s contributions in June.

Nothing much is expected from this meeting. The March dots showed the Committee median vote leaned toward one cut this year and one more next year. That’s unlikely to be settled for a long while yet. Powell is unlikely to be comfortable with teeing up such a move before his successor takes over and he faces eleven other voting FOMC members that are more worried about inflation at the moment.

Our forecast remains for one cut by late year and another in early 2027 which would drop the fed funds upper limit rate to 3.25% and hence still on the boundary between restrictive and neutral.

GLOBAL DATA TAKES A BACK SEAT

On tap into the N.A. session will be minor US releases including the advance merchandise trade figures for March (8:30amET), housing starts for February and March as data is still catching up to the government shutdown’s effects (8:30amET), and durable goods orders during March that are expected to rise on airplane orders (8:30amET).

Brazil’s central bank is expected to cut by 25bps from a highly restrictive stance after today’s close (5:30pmET).

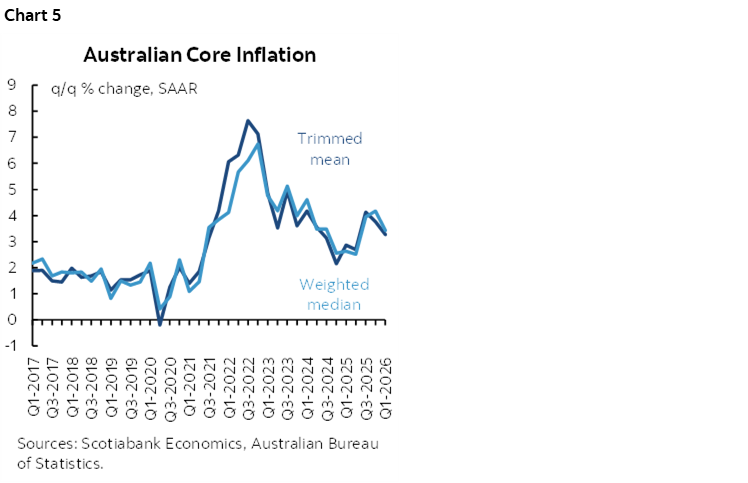

I’ve already flagged Aussie CPI and chart 5 shows the q/q annualized profile.

German states posted CPI readings that suggested national CPI would come in a touch beneath consensus. Three states posted gains of 0.6% m/m, two were up by 0.4% and one was up by 0.5%. Consensus expected 0.6% m/m for CPI and 0.8% on an EU-harmonized basis and sure enough, CPI was up by 0.5% m/m on an EU-harmonized basis.

Spanish CPI posted a rise of 0.7% m/m on an EU-harmonized basis (0.6% consensus). Core CPI was up 2.8% y/y (2.9% consensus).

The Bank of Thailand held its policy rate unchanged at 1% as widely expected following the cut at its last meeting in late February. A watch-and-wait bias was delivered around the war’s effects on oil, inflation and the baht.

Chile’s central bank held its overnight rate at 4.5% last evening as widely expected and with data dependent, hawkish concerns toward inflation risk emanating from commodities and the war.

Swedish GDP disappointed with Q1 coming in at -0.2% q/q SA (+0.2% consensus). The krona and rates ignored as backward looking in relation to concerns and partly because retail sales soared in March (+3.1% m/m).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.