ON DECK FOR TUESDAY, APRIL 28th

KEY POINTS:

- Spiking oil prices are in the driver’s seat this morning

- Yen, JGBs shake off mixed BoJ communications

- Canada’s fiscal update: spending out the good luck…

- ...while still being poor forecasters of deficit and issuance

- A Canadian SWF — facilitator and/or competitor?

- US consumer confidence — jobs versus prices

- BCCh expected to hold

Oil markets are in the driver’s seat again this morning which is a wonderful thing if, oh, let’s say you’re about to talk about Canada’s fiscal situation. WTI and Brent futures are both up by about $3–4+. Sovereign bond yields are higher everywhere but particularly in the Eurozone—given its large importer status—with yields up between about 4–10bps across maturities and countries. Stocks are mixed with US futures down, TSX futures flat, and European cash markets slightly positive on balance. The dollar is stronger against all majors.

Oil is higher as the US administration evaluates Iran’s proposal to reopen the Strait of Hormuz while deferring talks on its nuclear ambitions. That’s unlikely to fly and as Marco Rubio put it, there are “questions about whether the person submitting it had the authority to submit.” Managed irresolution. Continue to keep that term front and center.

Among the considerations are the BoJ’s communications, some US data on tap, Canada’s Spring fiscal update, thoughts on Canada’s sovereign wealth fund and Chile’s pending rate decision.

YEN, JGBS SHAKE OFF BOJ COMMUNICATIONS

Markets shook off the Bank of Japan's communications. Pricing for the next several meetings was unchanged with markets pre- and post-communications expecting an unchanged two-thirds probability of a hike at the next meeting in June. JGB yields were little changed. So was the yen, independent of broad dollar strength this morning.

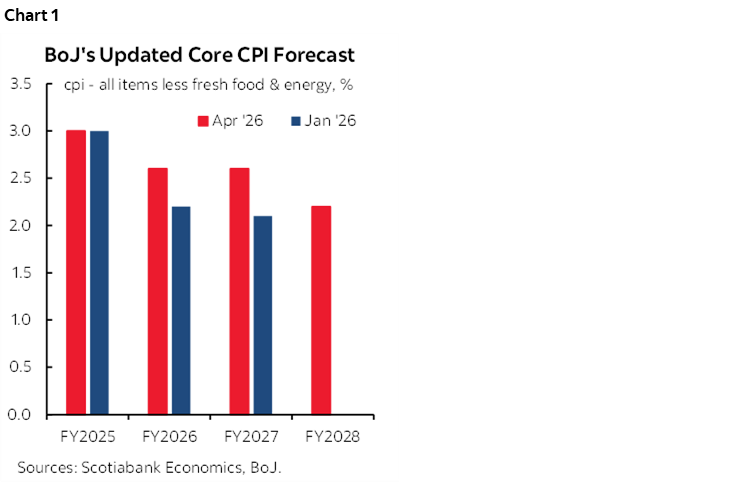

That's because the communications were rather mixed. On the hawkish side of things, three out of nine Board members dissented in favour of a hike at this meeting, which is fairly high. Forecasts raised the core inflation outlook to 2.8% this year and raised the next year’s forecast with the addition of FY2028 forecasts expecting sustained achievement of 2%+ inflation goals (chart 1). The criteria for a continued hike bias was lowered to be conditioned on "developments" in the economy rather than "improvements" that may not happen because of the commodity-driven supply shock to Japan as a large net importer.

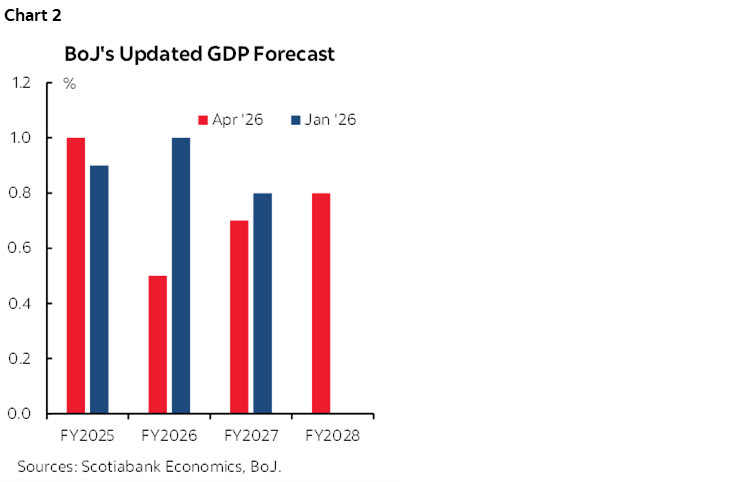

On the dovish side, growth was cut in half to 0.5% in the current fiscal year and slightly downgraded for next year (chart 2). This backed the uncertainty expressed by Governor Ueda who said the number of dissenters "reflects the situation of a negative supply shock, with the economy weakening while prices rise. In that environment, deciding the appropriate course of monetary policy becomes extremely challenging.” Indeed, for a large commodity importer without such offsetting riches.

US CONSUMER CONFIDENCE—JOBS VERSUS PRICES

US consumer confidence will be updated with the April reading at 10amET. It may deteriorate further in light of persistent upward pressure on commodity prices including gasoline but that critically depends upon how consumers feel about the job market. This measure is more driven by labour market conditions by contrast to the UofM sentiment gauge that is more driven by cash flow and markets. After nonfarm's gain in March and ADP's tracking in April, the job market could be setting a nearer-term floor to sentiment. Watch inflation expectations and jobs plentiful readings.

Weekly ADP private payrolls (8:15amET) could be worth a peek given the prior week's surge to a four-week moving average of about 55k w/w which implies a monthly change of over 200k in April.

Repeat sale house prices have been on the rise for several months now with another gain in February expected (9:00amET).

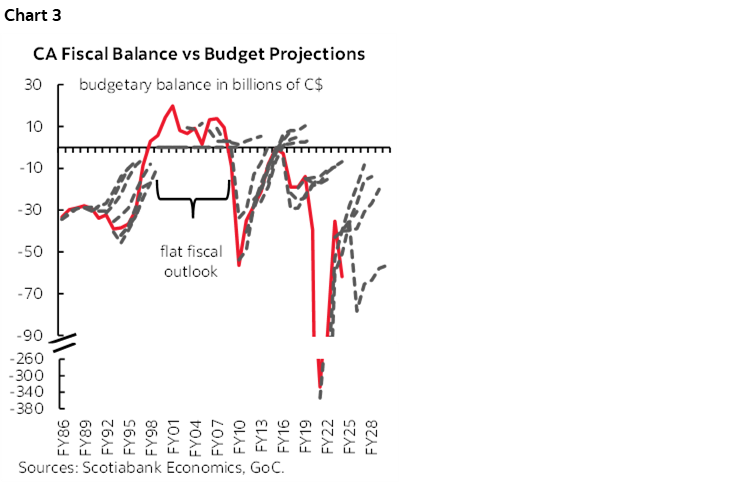

CANADA'S SPRING FISCAL UPDATE

Canada’s Spring economic statement and fiscal update is due after the close today. The cottage industry of those who obsess over government will whir to life for a short time and my, there are a lot of them in this country.

Additional stimulus measures, the closing deficit for FY25–26, guesstimates on future deficits and issuance, and details behind plans for a small SWF will be key. Never take the deficit and issuance guidance seriously; Finance’s track record is very poor on magnitudes and missed inflection points (chart 3). So is the analyst community's track record. That’s because surprises—like commodity booms—come along, politics gets in the way by doing things like spending unexpected improvements and because the economy doesn’t always perform to expectations whether good or bad. It’s a tough business. Tougher than the strident talk that too often surrounds anyone’s projections.

In this case, however, they may hit their deficit for FY25–26 or come in lower by spending all or most of positive surprises. Higher prices are definitely helping the government since they tax all the booming commodities and the relevant price deflator isn’t CPI—it’s the broad GDP deflator that guides nominal GDP as a driver of the fiscal position. The domestic economy may be performing better than feared. Rolling out the government’s spending initiatives is fraught with uncertainty because fo the sheer enormity and complexity of the varied programs. Additional spending measures are likely but they've pre-announced a lot as well.

CANADA’S SWF—FACILITATOR OR COMPETITOR?

The Carney administration’s announcement that it would introduce a sovereign wealth fund called the Canada Strong Fund will be followed up by important details to be shared as part of the government’s Spring economic and fiscal update after today’s local market close. Additional details will follow over the coming months. It would have been helpful to have all the details on announcement, but the process appeared to be hurried.

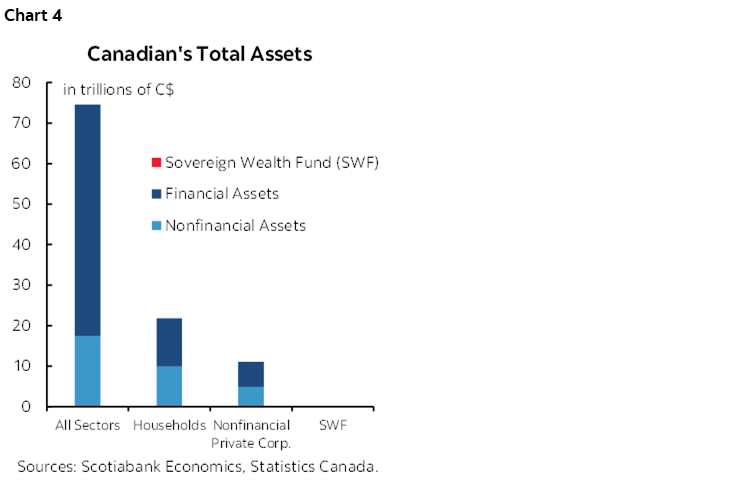

A few principals need to be laid out in addition to comments in yesterday morning’s note about some of the pros and cons. One is that it’s small change at C$25 billion to be achieved over three years which gets lost in the axis on chart 4. This is a C$3.3 trillion economy in nominal GDP terms that has about C$75 trillion of assets as at 2025Q4 (of which nonfinancial $17.5T, financial assets $57T). Small means the announcement is attracting over-hyped attention both in terms of broad pros and cons.

That said, while it will be small for many years to come, it won’t necessarily be small in relation to its role as a potential competitor to specific financial industry products offered by particular types of financial institutions which I’ll come back to.

Another is that it is debt financed. That’s an oddity in the world of sovereign wealth funds where SWFs are more commonly financed by surplus savings. By debt financed, I mean Finance Minister Champagne’s hint (see below) and talk of a retail debt product.

Third is that we start with a clean slate in seeking comparisons to other SWFs around the world because there is no comparator. Quebec’s Caisses? Not really, since the Canada Strong Fund will be mandated to invest exclusively at home whereas despite the hype, over 80% of Quebec’s fund is invested outside of Quebec with less than 20% invested in Quebec which is nevertheless a huge overweight position. SWFs in saving nations like Norway, UAE, Singapore, China etc are also bad comparisons because Canada doesn’t save. Alberta’s Heritage Fund has a history of bad management and political interference so definitely forget that comparator. So, the Canada Strong Fund is an interesting opportunity to do something uniquely Canadian compared to the rest. Hopefully unique turns out to be a good thing.

But the point about it being a debt-financed SWF in a country that is not a saving nation with persistent current account deficits reliant upon capital inflows is key. That’s because it means the modest size of the Canada Strong Fund will be put directly into competition within the existing savings marketplace. Some will win, some will lose. The winners will be the asset management community, which is why they’re fist-pumping. The losers may be more traditional financial institutions.

How so? Carney’s comment yesterday that the retail product they have in mind is “something consistent to buying a government bond, but has the upside, the additional return, when these projects realize their potential” makes it sound like a convertible bond or a bond with some form of equity kicker or performance kicker. The initial release said “As the Canada Strong Fund succeeds, investors will be able to share in the upside, while their initial invested capital will be protected.”

Sound familiar? Enter the equity-linked GICs offered by many financial institutions. A market-linked GIC often offers principal guarantees, a guaranteed minimum return and the modest potential to earn more, and it’s not for everyone. It’s for relatively risk-averse investors with the upside capped but for those who want a little fixed income and a little equity in a combined product. If put in an RSP or TFSA, then an equity-linked GIC is tax-advantaged either through the deduction or the tax-sheltered income and so if today’s retail SWF product is tax advantage then it will also compete against products that go into TFSAs and RSPs. Managers of products like that at traditional financial institutions should be somewhat on guard. An equity-linked retail product to fund the Canada Strong Fund would presumably be higher risk, mind you, since it the equity kicker would be driven by specific long-tailed, illiquid resource and infrastructure projects.

The SWF could grow rapidly if well managed. By comparison, Norway's fund was originally of a similar size that is being targeted by Carney (US$23B in 1998). Today it’s around US$2T. A key caveat, however, is that Norway's fund was blocked from investing domestically and must invest on prudent person standards outside of the country. That's not what this is, which may mean a much lower cap and shallower trajectory for the assets. Carney noted that over time it's possible funds like this outgrow their domestic markets like Singapore's Temasek did but that "The ultimate impact will benefit younger Canadians and their children." In other words, be patient.

We learned nothing yesterday on contribution limits, specifics around what type of retail product they are targeting although principal protection seems to be offered, target returns, how the government will fund the seed money, in which projects the SWF will invest, etc. Some of those details may arrive at 4pmET today but others will take weeks, months and maybe longer to emerge.

As for financing the $25B, FinMin Champagne may have alluded to how to fund the seed money. When asked where is the money coming from, he touted Canada’s AAA and borrowing advantage and ability to borrow to invest at higher returns. Fully consolidated financial accounts of the government including this new Crown corporation would include the debt it issues through retail channels.

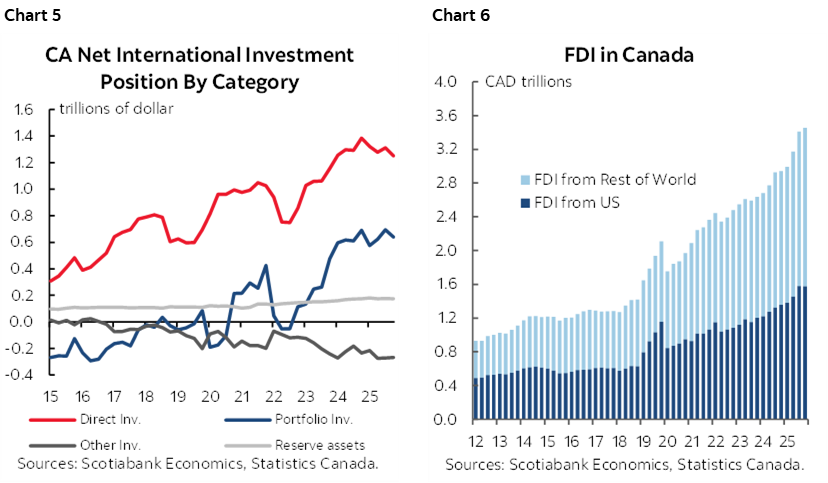

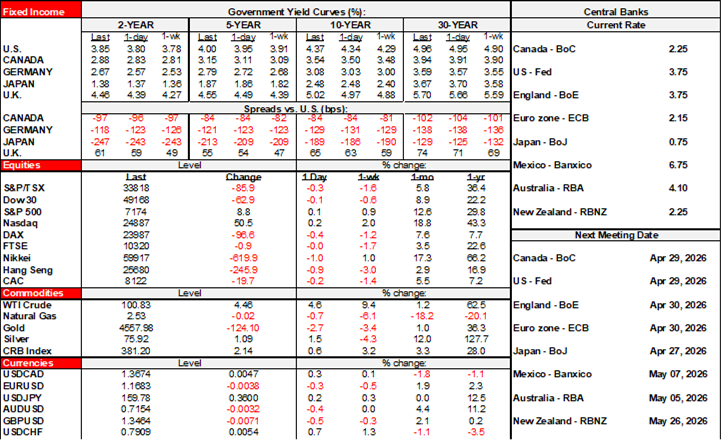

Still, the world is in love with Canadian investments these days. Chart 5 shows the large positive surplus of foreign direct investment into Canada net of Canadian foreign direct investment abroad along with the similarly defined balance for portfolio investment. Much of the FDI inflow into Canada is increasingly coming from countries other than the US; Canada has been diversifying away from reliance upon US investment since at least 2020 (chart 6). America, be careful what you wish for in shunning Canada as one of your very biggest trade partners.

I thought I heard Carlos Leitao—a Liberal MP, former Quebec Finance Minister and former jovial colleague—mention ‘Victory Bonds’ as an option during FinMin Champagne’s press conference. We’re not at war, which shouldn’t be trivialized to suit today’s challenges and politics, and those bonds did not back assets as opposed to funding spending behind the war effort.

In fact, I would hope that the portion funded with retail debt will be low. That’s because the government may be biased toward funding higher risk projects best financed via equity instead with principal guaranteed, potentially tax advantaged fixed income instruments for political reasons. Why? They may not want to risk these investments blowing up into the next election although they would also cut off the prospect of being buoyed should they outperform.

The press conference made it unclear who chooses the projects backed by the fund. On the one hand, we’re told it will be managed on an arm’s length basis through a separate crown corporation with a clear investment mandate. Then we were told by PM Carney that “it doesn’t have to be, we’ll consult” in response to a question on whether investments will go to projects that the government chooses. So, some will, some won’t?

Chile's Central Bank to Hold, ECB’s Inflation Expectations Soar

BCCh delivers a policy decision after markets shut today (6pmET) and is expected to hold.

The ECB's 1- and 3-year measures of inflation expectations soared to 4% (2.5% previously) and 3% (2.5% prior) respectively in April. The direction would surprise no one outside of the limited consensus.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.