ON DECK FOR MONDAY, APRIL 27th

KEY POINTS:

- Markets largely shake off Iran headlines…

- …ahead of an onslaught of central banks this week

- Canada to announce creation of sovereign wealth fund …

- ...and the pros, pitfalls, and cautions need details

- German consumer confidence sinks to three-year low

- Global Week Ahead — The ‘B’ Crew Won’t Lend Confidence to Central Bankers (reminder here)

Markets are bracing for a week that will be jam-packed with central bank meetings and top shelf data. Oil is up by only about a buck or so after volatile developments over the weekend. The dollar is broadly weaker as higher beta and commodity crosses like the krone, CAD and antipodeans lead the way. Sovereign bonds have a very slight cheapening bias in the US, Canada and European longer-ends. Equities are a little higher in Europe, while treading water in N.A.

Developments on Saturday sounded like a who-broke-up-first argument between high school kids. Iran’s Foreign Minister split Islamabad and then Trump said he was pulling his ‘B’ team, then saying it was up to Iran to call and make up. This is the stuff of international relations these days, folks. Iran’s Foreign Minister visited Putin in Moscow. Unconfirmed reports indicate new Iranian proposals but mixed in with Iran’s red lines that still appear to be inadequate to the US depending upon who you believe.

There were no other notable overnight developments. German consumer confidence slipped again and sits at its lowest since early 2023. Canada will hold two press conferences I’ll explain below. The US only updates the Dallas Fed’s manufacturing index (10:30amET).

CANADA TO ANNOUNCE CREATION OF A SOVEREIGN WEALTH FUND

Canada’s Carney administration will announce a new sovereign wealth fund in a press conference at 9:15amET in Ottawa. FinMin Champagne will follow up with a press conference at 10amET in Montreal. The announcement is ahead of tomorrow’s Spring economic statement including updated fiscal numbers and plans after the close. It’s also ahead of a September investment conference that the Carney administration is putting on which is aimed at attracting global investment to Canada.

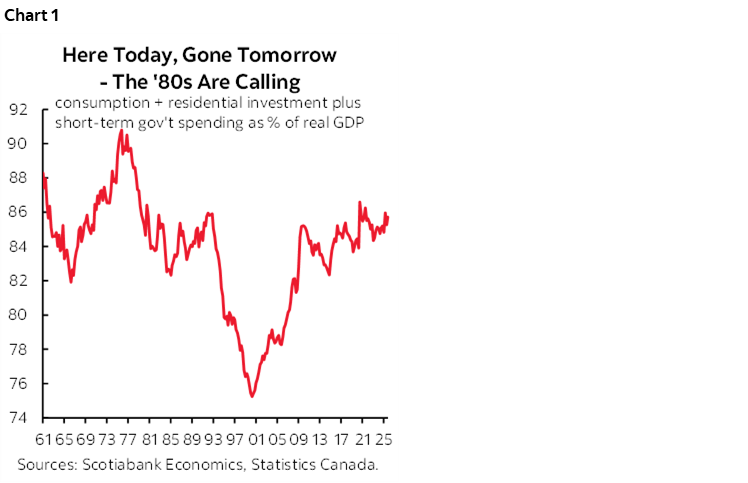

The devil will be very much in the details. In principle, I like anything that may lean toward policy emphasis upon saving and investment to motivate higher future productivity and living standards versus too many years of propping up here-today-gone-tomorrow spending. I’ve long advocated this policy pivot from high shares of the economy going toward household spending, current government spending and housing investment (chart 1). The signals from the Carney administration have nevertheless been mixed on this issue including an aggressive housing plan and albeit limited nearer term tax cuts and transfers like expanded GST rebate cheques and the fuel excise tax suspension.

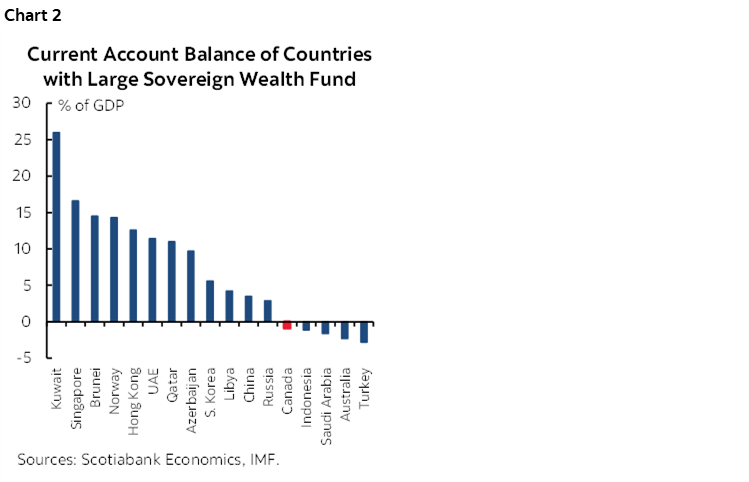

One immediate observation is that usually countries with sovereign wealth funds are net savers (chart 2). Canada is, well, not. The current account is the net two-way balance on exports and imports and investment income. When it’s positive, it means that the country is generating more receipts from abroad than it is paying out and the flip side is a negative capital account balance which means the country is a net exporter of savings.

For instance, Norway’s Government Pension Fund has assets over US$2T and Norway’s current account balance is about 14% of nominal GDP. China’s SAFE and China Investment Corporation are similarly sized with a current account balance of 4%. The UAE’s ADIA is over US$1.1T and the UAE’s current account balance is about 15%. Singapore’s GIC has assets just shy of $1T and Singapore’s current account is 17%. And so forth.

Then there is Canada’s current account deficit that is just under 1% of GDP which is better than it used to be at about four times that until the mid 2010s.

The implication of this first point is that absent net saver status, a Canadian SWF could divert savings from other savings institutions and assets without necessarily growing the pie unless Canada somehow shifts toward being a net saving economy in future. That might carry knock-on effects, some of which could be positive such as if it ups the ante on other asset managers to improve performance.

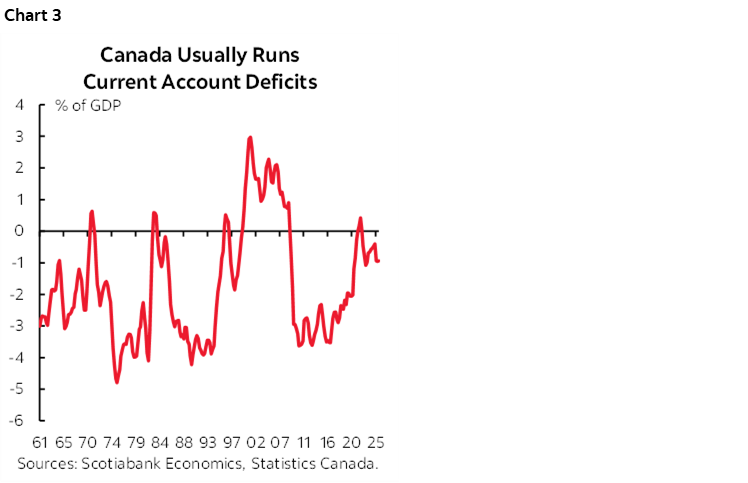

Is that possible for Canada to become a net saving economy at a very high level? Well yes, technically. Canada had positive current account balances throughout the decade of the 2000s, and marginally so at brief intervals before that (chart 3). How it could become a net saver is also key as you wouldn’t exactly declare success if it was because a weak domestic economy was crushing imports. If Canada were to finally get its act together and truly unleash its rich natural resources, then a world of positive current account balances could lie ahead. The flip side would be capital account deficits as more aggregate national saving gets invested abroad and external debt is paid down.

It would probably take a while to get there, however. In fact, building out the resource sector with assistance from a SWF would probably expand the size of the current account deficit at first as the capital stock is deepening and then pivot toward improved current account balances as the capital stock generates returns. Australia had this kind of experience. In the meantime, the first round response of a possible widening of the current account deficit could mean yet greater cannibalization of other savings by a SWF.

I’ll believe that Canada gets it many varied, competing, disorganized interests aligned toward such a goal when I see it. It’s possible, but the biggest challenge facing Carney is to steer unherdable cats toward achieving common prosperity.

There are other key details that will be vitally important. How will a Canadian SWF invest? Infrastructure and resource projects at home appears to be likely, but how will it partner or compete with private capital and on what mixture of private and public assets? Other funds like Norway’s invest abroad and are prohibited from investing at home. Funds like Alberta’s Heritage Fund and the effort to have it newly managed by the Heritage Fund Opportunities Corporation have tended to invest in Alberta in health care, education etc and has had a spending bias that has been widely criticized for poor management.

How strict will foreign investment limits be? It sounds like 100% domestic, in which case Canada could be winding the clock back to when the CPP was barred from investing abroad but did it in clandestine ways through derivatives. What will be the governance structure, who will manage it, what fees will be paid and what will be the investment mandate? Will withdrawals for other purposes be allowed and what limits will there be? Will it lend to Crown corporations? Will it be a vehicle for state directed capitalism? Will it generate income to be distributed to Canadians and how? And how will the vague guidance around allowing Canadians to contribute work in practice with what contribution limits and choices?

GLOBAL WEEK AHEAD REMINDER

Please see the Global Week Ahead—The ‘B’ Crew Won’t Lend Confidence to Central Bankers (here). Key topics include:

- US-Iran negotiations — Sending in the ‘B’ crew

- Bank of Canada preview

- The war wasn’t the catalyst for our BoC hikes…

- …but it strengthens the case

- Canadian fiscal policy — pre-spending the commodity dividend

- BoC’s gross bond buying could happen sooner

- FOMC preview: Powell to pass the baton

- BoE — A new shock compounds residual inflation

- ECB — Waiting for June

- BoJ — Hold with hawkish cues?

- BCCh — Extending the hold

- BCB — Easing off a deeply restrictive stance

- BanRep — Continued divisions?

- BoT — No follow-up

- Canadian GDP in line with BoC?

- US GDP — All about what lurks beneath

- GDP: US, EZ, Taiwan, Sweden, Mexico

- Inflation: US PCE, EZ, Australia, Tokyo, Peru

- China PMIs

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.