ON DECK FOR FRIDAY, APRIL 24th

KEY POINTS:

- Tech earnings fail to lift broad risk appetite

- Gilts underperform on firm retail sales and BoE survey

- Canadian consumers are tentatively tracking a rebound

- Russia’s central bank cut as ruble strength mitigates energy pass through

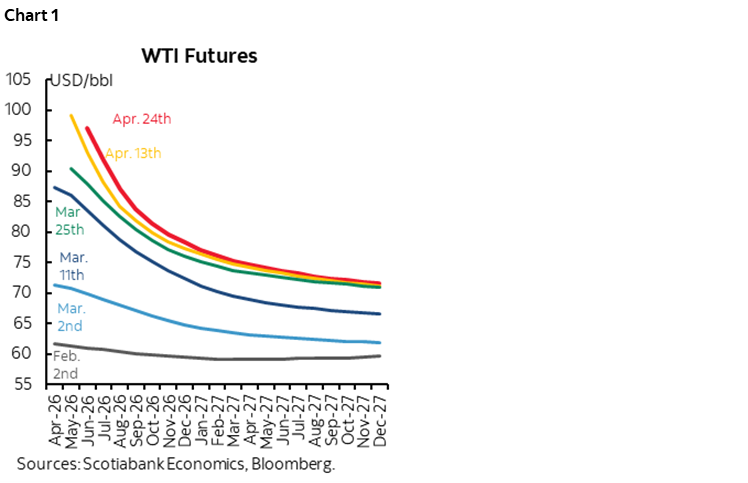

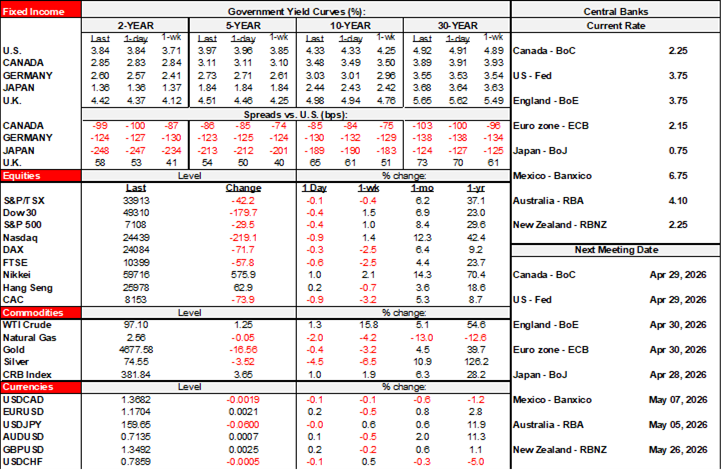

Oil is up again, this time by up to US$2/barrel with WTI approaching the early April peak and the commodity futures curve still parked in the US$70s range throughout 2026–27 (chart 1). The driver is more hot air driving developments in the war with Iran. Intel’s blowout earnings report last evening isn’t so much helping the broad market tone this morning. US equity futures are flat on the S&P but up 1% for Nasdaq futures as TSX futures are little changed on the red side and European cash markets are broadly lower by up to 1%. Across sovereign bonds, the gilts curve is underperforming others post-retail sales and a BoE survey of inflation expectations. Across currencies, the USD is broadly softer.

The rest will be kept light to get onto a tonne of other work today particularly around expectations for the onslaught of central bank meetings that are due out next week. The only real highlights are updates on consumer spending in Canada and the UK and Russia’s rate cut. The US calendar will be quiet today with just UoM sentiment revisions.

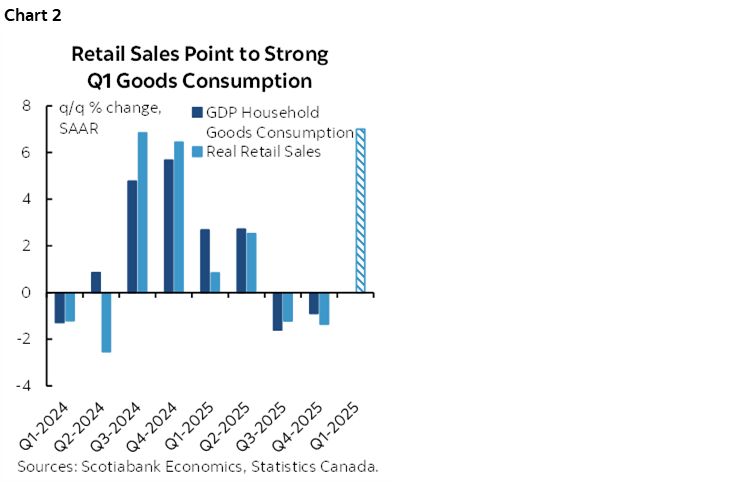

Canadian Consumer Rebound?

Canadian retail sales are expected to come in strong in nominal terms for the month of February based on prior guidance, but key will be volumes and other details. Statcan had guided back on March 20th that February’s sales were tracking a gain of 0.9% m/m SA in value terms. Stripping out prices to get volumes will be one key. Preliminary March guidance might not be so kind as new vehicle sales fell but gas prices spiked higher.

Chart 2 will be updated with the fresh numbers but so far we’re tracking a strong gain in real retail sales during Q1 that points to a strong gain in total spending on goods as a part of overall consumer spending in GDP accounts.

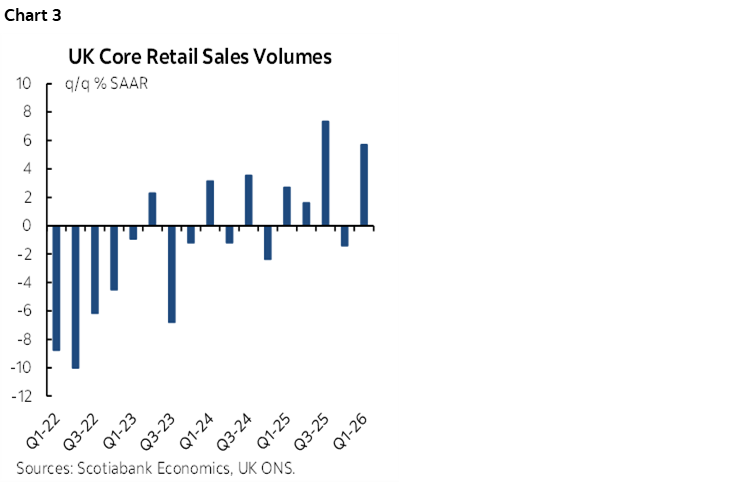

UK Consumer Spending Surprise and Higher Inflation Expectations

UK consumers were a little peppier than had been expected. Retail sales volumes were up by 0.7% m/m SA in March (0% consensus) and only partly aided by prior month revisions that took the jumping off point lower (-0.6% m/m instead of -0.4%). Sales volumes ex-fuel were up 0.2% m/m (0% consensus) and aided by revisions (-0.6% prior instead of -0.4%).

For the quarter, sales volumes were up 5.7% q/q SAAR for the second strongest quarter in the past four years (chart 3).

Higher inflation expectations also added to market reactions. A short-term 1-year ahead measure for April increased to 4% from 3.5% in March and 3% before that. The BoE’s Decision Maker Panel survey showed plans to raise prices by 4.4% over the coming year.

Russia Cuts

What to do when your economy is basically driven by oil and war with inflation still running hot? Why you cut, clearly, and guide that you might cut again. Or at least that’s what Putin’s central bank did this morning. Russia’s central bank reduced its key rate by 50bps to 14.5% in line with consensus. Inflation is running at 5.9% y/y with core CPI up 5%. The bank points to backward core inflation ebbing to 5% y/y from a peak of about double that last March. Granted, the ruble has appreciated by 14% since the low on March 19th which points to possibly less imported inflation risk as an offset to the imported income effect of higher energy prices that benefits Putin’s cronies.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.