ON DECK FOR THURSDAY, APRIL 23rd

KEY POINTS:

- Risk off sentiment on war, earnings, PMIs

- PMIs warn of stockpiling, inflation surge

- Philippines’ central bank hikes

- Canadian producer prices to continue signalling higher core CPI

- Canada has the edge in trade negotiations with the US

Stocks are broadly cheaper and bonds are treading water while the dollar is broadly gaining with a notable exception being that CAD is right up there with the dollar. Oil is volatile and slightly higher. US and Canadian equity futures are down by about ¼% to ½% and European cash markets are mostly in the red by up to 1% except for the little changed CAC40.

As for catalysts, developments concerning the US and Israeli war with Iran continue to deteriorate. There are no signs of negotiations, Iran continues to fire at ships in the Strait of Hormuz and the US continues to intercept ships. They’re in a stalemate, risking persistent supply disruptions across commodities. President Trump and Israel started a war that Trump can’t finish in a midterm election year without ruining the GOP and the evil Iranian regime knows this.

Global PMIs may also be contributing to market concerns given warnings contained within them (see below). The US releases its PMI later this morning. So may earnings as Tesla’s after-market earnings release failed to impress but partly on higher cap-ex. Intel releases in today’s after-market.

Canada brings out industrial prices that lead consumer inflation. One central bank hiked overnight. And I’ll reiterate my bias regarding key points concerning Canada-US trade negotiations.

GLOBAL PMIS WARN OF SUPPLY SHORTAGES, STOCKPILING & LOOMING INFLATION

A wave of global purchasing managers indices for the month of April broadly signalled more order front-running and stockpiling in anticipation of higher prices being passed through alongside supply shortages. Price guidance accelerated across markets to between the fastest inflation since the pandemic or on record depending on the country. Here’s the round-up behind charts 1–3.

- Australia’s composite PMI moved up by 3.5 points to 50.1 and was primarily driven by services (50.3, 46.3 prior) but manufacturing also edged higher (51.0, 49.8 prior). S&P noted “lead times lengthening at the most-marked rate seen since mid-2022” and fuel and freight “pushed cost inflation to its highest in just under four years.”

- Japan’s composite PMI slipped 0.6 points to 52.4 as services decelerated (51.2, 53.4 prior) but manufacturing accelerated by 3.3 points to 54.9. S&P explained that manufacturers “boosted output due to concerns and uncertainty surrounding the war….and the potential for further supply chain disruptions” and there was “the steepest rise in composite selling prices on record.”

- India’s composite PMI moved up by 1.3 points to 58.3 because of gains in both services (57.9, 57.5 prior) and manufacturing (55.9, 53.9 prior). S&P noted “firms are building buffer stocks to manage the uncertainties around the longevity of the supply-side shock” and on rising input costs “firms passed through part of the increase via higher selling prices.”

- The Eurozone’s composite PMI fell by 1.9 points to 48.6 as services decelerated (47.4, 50.2 prior) but manufacturing picked up (52.2, 51.6 prior). The composite PMIs for both Germany and France fell and other countries will release later on. S&P’s write-up emphasized advance order building to get ahead of price increases in manufacturing and warned “this is the biggest surge in cost pressures that we have recorded since 2000” outside of the pandemic.

- The UK composite PMI gained 1.7 points to 52.0 because both services (52.0, 50.5 prior) and manufacturing (53.6, 51.0 prior). S&P cautioned that faster growth may be due to a rush to secure purchases before widespread price increases and supply shortages and commented that “prices have spiked higher at a rate not previously seen by the survey out of the pandemic” and warned of faster inflation than forecasters anticipate.

- The US updates its composite PMIs at 9:45amET.

Philippines’ Central Bank Hikes with More to Come

BSP faced an evenly divided consensus between a hike and a hold going into its decision and decided to hike its overnight rate by 25bps to 4.5%. Guidance was hawkish, as Governor Remolona stated “Once we start raising the policy rate, we’re likely to raise it again. That’s a better strategy than raising it just one time and making a big hike instead of a small hike.” Markets are priced for the policy rate to move up by another 100bps or so into 2027.

Canadian Industrial Inflation Points to Looming Core CPI Inflation

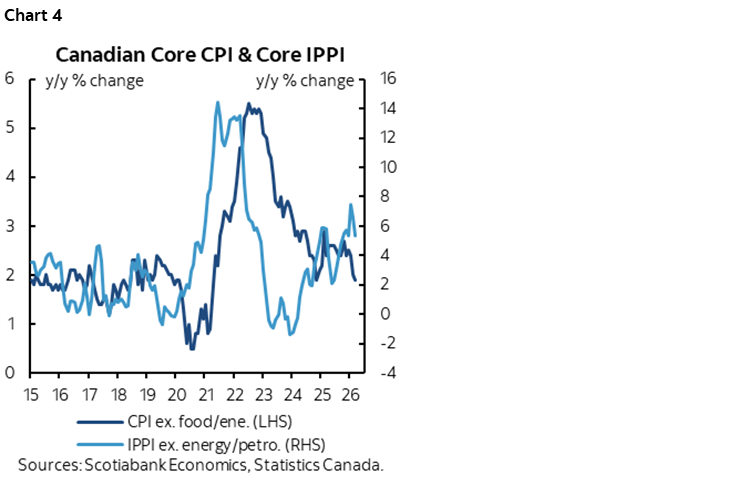

Producer prices during March posted large gains. Core industrial prices ex-energy have been soaring for a while and this matters because this measure tends to lead core consumer price inflation (chart 4).

This is one reason why we faded the soft patch on underlying core inflation and had a bias toward hiking in our forecasts before the war.

The longer-run drivers of persistently higher inflation were another part of the narrative to remove last Fall’s two insurance cuts that violated a Taylor Rule approximation of what the policy rate should be. The shocks to border frictions across supply chains over the past ten years have been profound, starting with Brexit, then Trump 1.0, then the pandemic, geopolitical conflicts, and Trump 2.0. The liberalized trade order is dead. Just-in-time inventory management is dead in favour of stockpiling and running fatter inventories to avoid lost sales or outright bankruptcy in the next supply shock. The associated costs get passed onto a variety of stakeholders including consumers.

You don’t evaluate long-wave inflation risk like this in the context of a handful of inflation reports. To show how ridiculous doing so could be, go back to the reverse circumstances after China gained entry to the WTO in 2001. Was there no disinflation coming from China’s aggressive push into manufactured exports because it didn’t show up in a handful of near-term inflation reports??

Canada Has the Edge in Trade Talks with the US

My guidance on the trade talks between Canada and the US and the associated risks hasn’t changed.

I see nothing new in the recent headlines. They’re talking about the same irritants that were in the mid-December USTR letter to Congress on demands from Canada (see p.10 for demands from Canada).

Negotiations with the Trump administration never offer concessions up front, only demands, then negotiate and only in earnest toward the end of the process. Expect plenty of headline volatility but trade talks with the US are a highly exaggerated shock to Canada. Why?

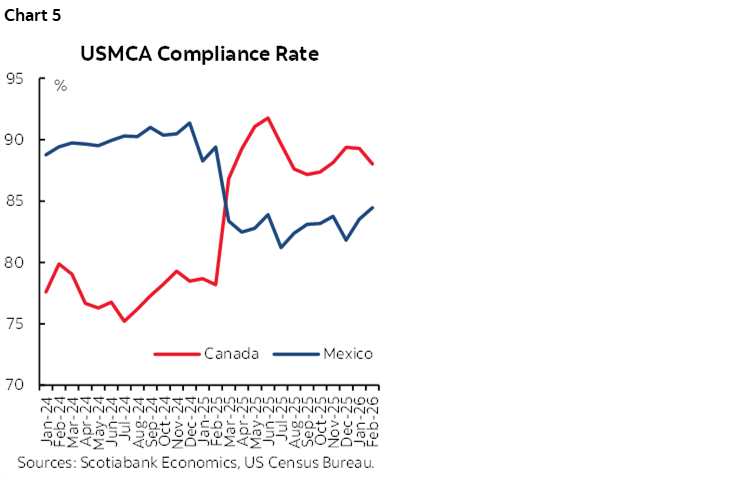

- Almost 90% of exports bound for the US are CUSMA/USMCA compliant (chart 5).

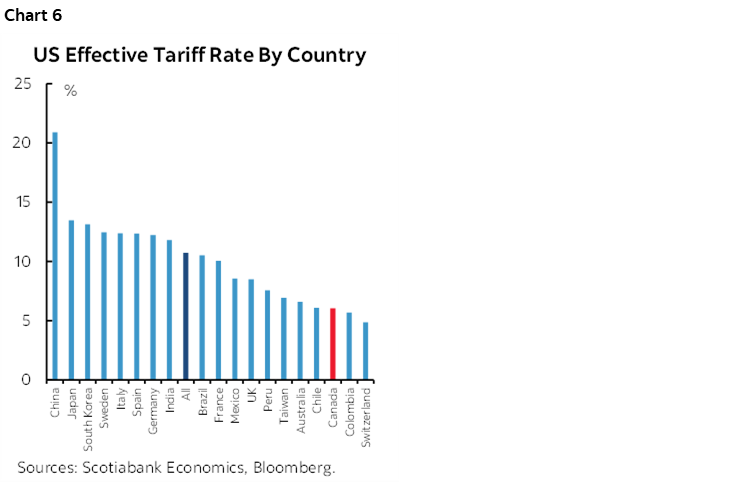

- Canada has the lowest imposed effective tariff rate of any of America’s trade partners especially after isolating narrow sectors like metals (chart 6). Its trade competitiveness versus America’s other trade partners gets a boost.

- CAD has depreciated from USDCAD 1.2 a few years ago to the upper 1.30s. It’s a flexible currency that offsets some trade risk which China by contrast does not have given its dirty-managed yuan peg to the dollar.

- Canada’s export price competitiveness has therefore improved for the vast overwhelming majority of its exports to the US.

- As long as Canada maintains the CUSMA carve-out then trade negotiations are more like a potential micro shock, not a macro shock.

- despite the rhetoric from Trump, his administration has never toyed with that carve-out. They can’t. He’d cripple his own country’s supply chains if he did. You have auto industry execs on both sides of the border warning their industry would shut within a week as one example.

The USTR letter to Congress in mid-December laid out the exact same issues that are now making headlines. They are not new and they are not insurmountable issues. They are micro issues on things like alcohol bans that would likely get lifted once there is a deal but that may remain in practice for a long time thereafter. Dairy marketing is a thorny issue with complicated Quebec politics but there are solutions or maybe you give more in other areas. The Alberta-Montana electricity dispute? Come on now, you’re just being silly. The media laws where the US tech bros are in the wrong and never want to pay their taxes or be told what to do? Well welcome to Canada, you can’t rip off other folks’ content and pay your taxes.

There is a path to a deal and none of these factors should hold it up in a big picture sense. The security angle is equally important with Canada spending more on defence, possibly including the Golden Dome white elephant.

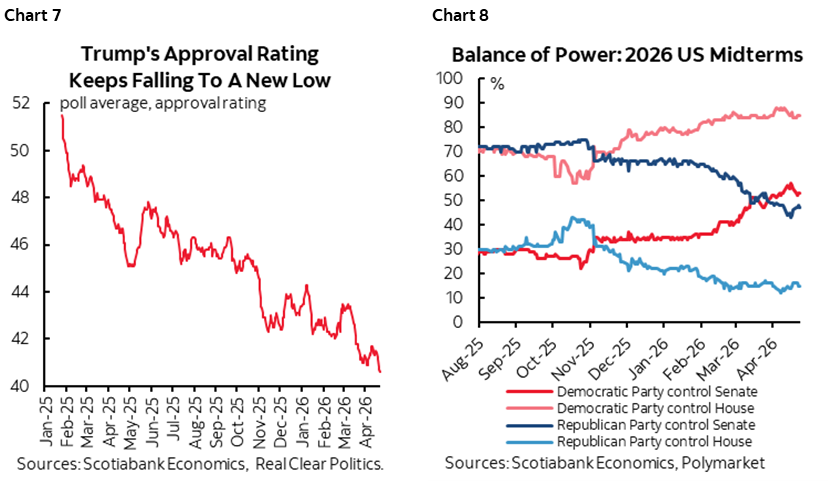

And politics favours Canada by a country mile. The Canadian government’s (stolen) majority means it doesn’t have to face voters until 2029–30. The US has elections every two years. Trump’s polling is in his boots on affordability, tariffs, war etc (chart 7). He’s going to lose at least one chamber, possibly two on November 7th and when the new Congress convenes in January (chart 8). In that context, I can think of politically dumber things to do given this starting point than for Trump to derail CUSMA but it’s a very, very short list!

The Trump administration may wish to strike an agreement on CUSMA/USMCA before the new Congress convenes in January after the November midterms. Otherwise, Trump is left negotiating on trade with the Democrats come January. They’re neither friends of his nor Canada’s and Mexico’s on trade. Biden shot down Keystone XL and maintained Trump 1.0 tariffs. Harris voted against TPP and the USMCA/CUSMA deal as a Senator. The far-left wing faction within the Dems—AOC, Sanders, Warren, Mamdani etc—would risk putting trade talks on ice in a stalemate and maintaining the agreement as is. In that scenario, Trump fails to deliver a freshened trade agreement and is left threatening executive orders to be challenged by courts, his own business lobby, markets and perhaps Congress. If the Dems take both chambers, Trump is in deep trouble for a whole host of reasons….

So overall, go back to the playbook during Trump 1.0. Trump talks a lot. Threatens a lot. Headline risk will flare. Canada has every reason to repeat what it did during Trump 1.0 and to be patient, hold out and play the long game because you don’t want to rush into a bad deal you’ll be stuck with for years. Time is on Canada’s side in that sense. I’ve argued this point throughout Trump 1.0 and 2.0.

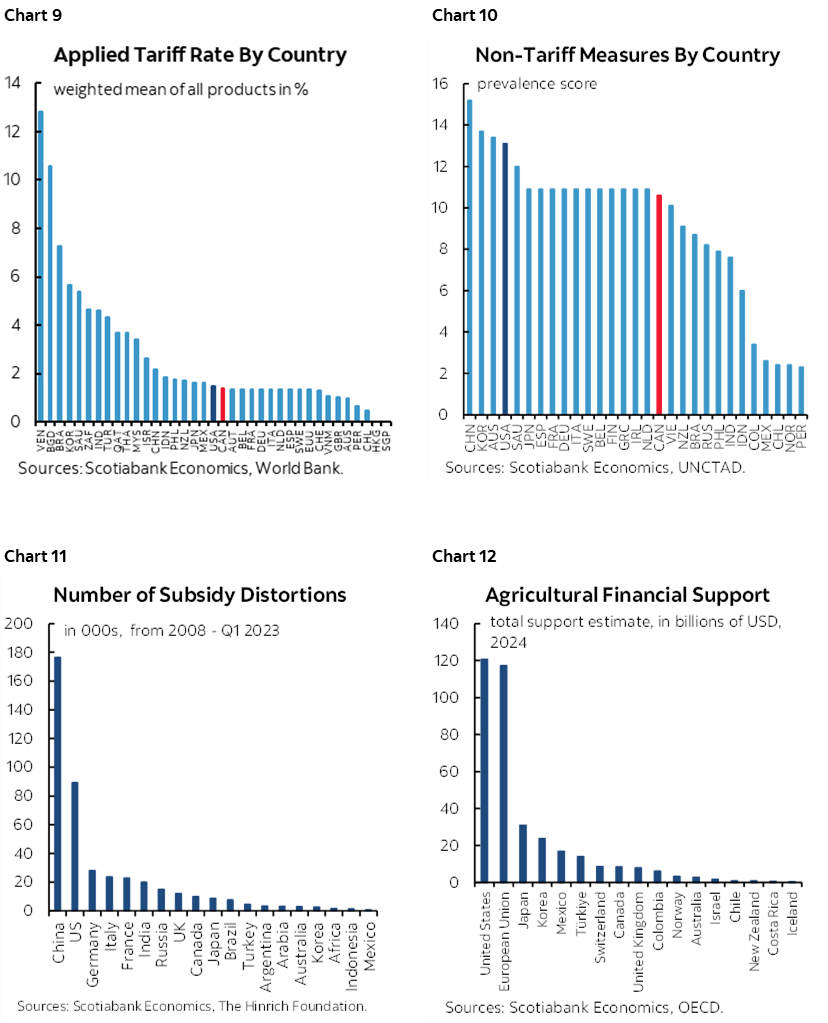

And on trade distortions, can the rhetoric that the US is some paragon of free trade. Hogwash. That wasn’t true on starting tariff rates before all this nonsense started (chart 9). It wasn’t true on nontariff barriers (chart 10). And it’s certainly not true on subsidies (charts 11, 12).

The US economy is a subsidy swamp. EMs have tariff and nontariff barriers partly because they don’t have the resources to fund the same massive subsidies. US and European farm subsidies and price arrangements retard economic development in poorer countries. No one subsidizes agriculture more than the Americans, not even the Europeans. The Farm Bill is welfare to corporate farms that costs American taxpayers. Tariffs cost American businesses and consumers. For years, Canada and the northern US states watched the southern and Midwest states siphon off auto investment with ludicrously rich state and local government subsidies given to domestic and foreign auto companies to locate production in their states. The US military-industrial complex is an elaborate network of subsidies and preferred procurement programs. Check out this list of subsidy recipients by company. Go back and review all of the subsidies and bailouts during the GFC. And so on and so forth.

Add to these points the total lack of understanding—or unwillingness to understand—that is behind misconstrued views on the drivers of the US twin deficits (fiscal and trade). The US has attractive investment opportunities in a dynamic, highly innovative economy with deep and liquid capital markets and part of the current account deficit reflects outflows to service that foreign investment into the US. The US spends too much—both its consumers and governments as evidenced by bloated deficits with the Trump administration persistently driving a deficit-to-GDP ratio of over 6%. Quit blaming others for the drivers of these imbalances. Just as China needs to open up its consumer market and do more for global growth, the US should curtail its multitude of distortions that would also benefit growth at home and abroad.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.