ON DECK FOR WEDNESDAY, APRIL 22nd

KEY POINTS:

- Markets are keeping it together after Iran boycotts talks

- US consumer spending put in another weak quarter…

- …as government rebound will be the main thing buoying US Q1 GDP

- Key takeaways from Warsh’s hearing

- UK markets ignored core CPI

- BI holds with slightly hawkish warning on inflation, rupiah

- Turkey expected to hold, but the lira and oil could motivate a hike

- SARB expected to hike later this year after core CPI surprises higher

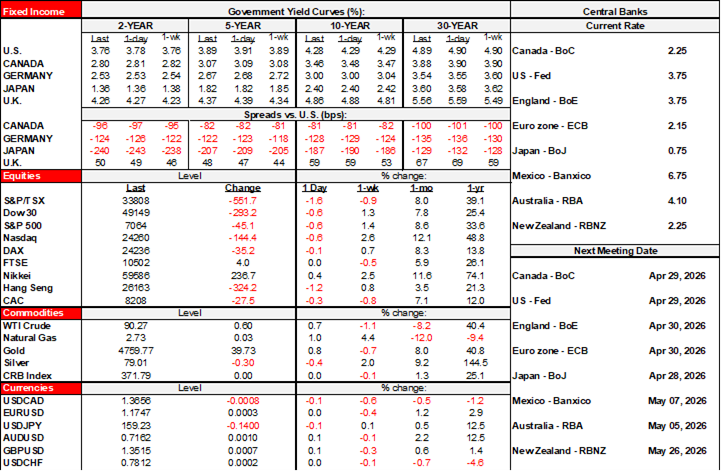

Markets are keeping it reasonably together this morning, all things considered. Oil is up by about a buck. US and Canadian equity futures are up by about ½% or so but European cash markets are mildly lower. Sovereign yield curves are little changed across N.A. and Europe after Antipodean curves cheapened by about 5bps across maturities. The dollar is little changed against most major crosses with outliers including a firmer NOK.

The ‘all things considered’ part was a reference to the break down of talks between the US and Iran, the ongoing US earnings season and light overnight developments ahead of a blank canvas in N.A. today. It doesn’t get richer than shooting most of the Iranian regime and then proclaiming they’re fractured as Trump did last evening.

I’ll also explain weakness in US consumer spending, expectations for Q1 US GDP next week, and important takeaways from Warsh’s testimony. First, the overnight stuff.

MARKETS SHAKE OFF UK CORE INFLATION

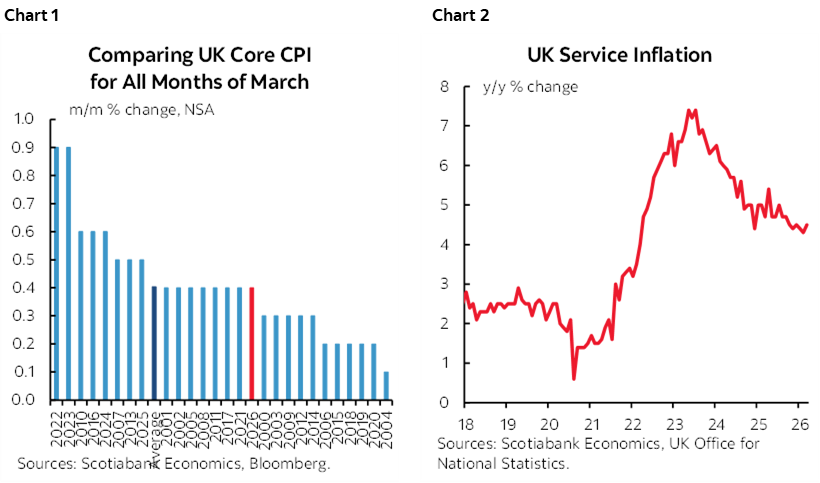

UK markets largely ignored CPI for the month of March. Headline CPI was up 0.7% m/m NSA (0.6% consensus) and core was up 0.4% m/m NSA. The core reading was in line with a typical month of March (chart 1) which resulted in the y/y rate coming in a touch lighter than consensus (3.1%, 3.2% prior and consensus). Services CPI was firmer at 4.5% y/y (4.3% prior); chart 2.

EM Central Banks and Inflation

Bank Indonesia held its policy rate unchanged at 4.75% as widely expected. The rhetoric noted a willingness to take whatever action is necessary to contain inflation and preserve the rupiah. The rupiah fell overnight but before the decision and on the heels of the breakdown of US-Iran talks.

South African core inflation was a bit firmer than expected (0.8% m/m NSA, 0.6% consensus) which drove the y/y rate up two-tenths to 3.2%. The whole South African rates curve moved higher with yields up by 4–12bps in bear steepener fashion overnight. SARB is priced for a hike or two later this year.

Turkey’s central bank delivers a fresh policy decision shortly after publication of this note (7amET). It’s expected to hold at 37% but some expect a 300bps hike to contain inflation risk and to address persistent lira depreciation.

ANOTHER WEAK QUARTER FOR US CONSUMER SPENDING

Yesterday’s US retail sales figures continued to showcase a weak quarter for consumer spending.

Retail sales volumes were up by 0.8% m/m SA which means over half of the 1.7% m/m nominal rise was due to higher prices and particularly gasoline.

For the quarter as a whole, retail sales volumes were up by just 0.7% q/q at a seasonally adjusted and annualized rate. This follows -0.4% q/q SAAR in Q4. This is after applying some interpolation to account for missing data in October due to the US government shutdown.

The US is definitely in the midst of a material consumer slowdown. American consumers are spending more on what they must (higher prices for essentials and higher prices in general) but the volume of spending has ground to a virtual standstill.

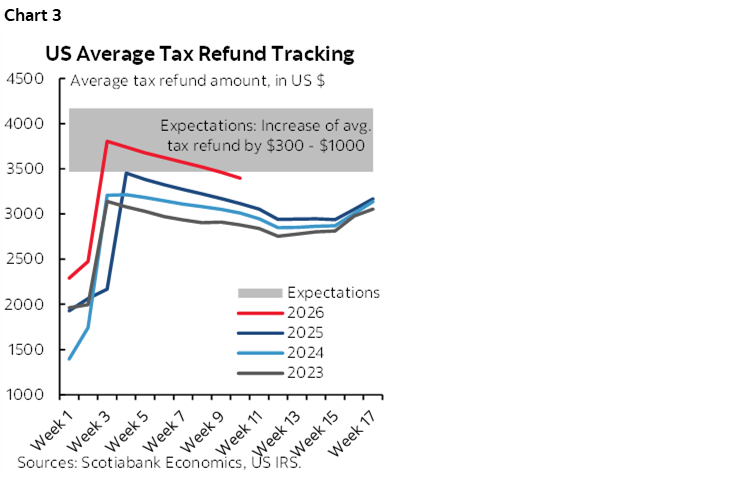

Why? No income growth over H2 will do that. A weakening trend in private payrolls ex-health that has long been in existence since before the 2024 election isn't helping. Tax refunds are disappointing (chart 3). Risk aversion would merit more precautionary saving. There is a disconnect between the data and some of the rhetoric coming out of the US these days.

Chart 4 shows the correlations with real retail sales and real total consumer spending which leads to the next point.

US Q1 GDP—STRONG ONLY BECAUSE OF GOVERNMENT

Q1 US GDP growth is tracking a rise of 3% q/q SAAR by our tracking. Don’t be fooled by illusory gains.

The reason for saying this is that Q1 GDP growth may be strong only because of the effects of the government shutdown. The Hutchins Center at the Brookings Institution estimates that fiscal policy will make a weighted contribution of over two percentage points to q/q SAAR Q1 GDP growth (here).

Beyond that there won’t be much else. We figure that Q1 consumption was up by just 1.2% q/q SAAR which makes a weighted contribution of around ¾%. Net trade is tracking a modest positive contribution as much of the weighted impact of export growth was offset by the weighted impact of strong imports. Inventory effects look to contribute a small positive to growth. Ditto for broader investment.

What this leaves us with is emphasis upon private final domestic demand by excluding government, inventory and net trade effects (ie: just consumption and gross private investment) to show an economy that is rather weak. This measure grew by just 1.8% q/q SAAR in Q4 with GDP up by only 0.5% q/q SAAR as government dragged growth lower. Clearly the US economy lost momentum over the past six months.

Key Takeaways from Warsh’s Testimony

Here are what I thought were the key takeaways from Kevin Warsh’s confirmation testimony before the Senate Banking Committee yesterday.

1. Markets couldn’t have cared less

Stocks moved broadly lower after his opening remarks. The US 2s yield edged a touch higher. And the dollar was slightly firmer. That was all driven by the coincidental surge of oil prices post-10am because the US boarded another Iranian ship and Hezbollah and Israel exchanged fire. Later in the day Trump’s deescalation by abandoning his deadline threats motivated market reversals.

I think the market fully gets that a Fed Chair is not as influential or capable of steering decisions today compared to long ago. It's a jury of 12 (sometimes) angry men and women. We'll see if it ends the same way as the movie with one holdout seeking to change the votes of the rest of them after a long, tedious an arduous debate. Ergo markets are fading his guidance in the following points.

2. He Wants to Change Inflation Measures

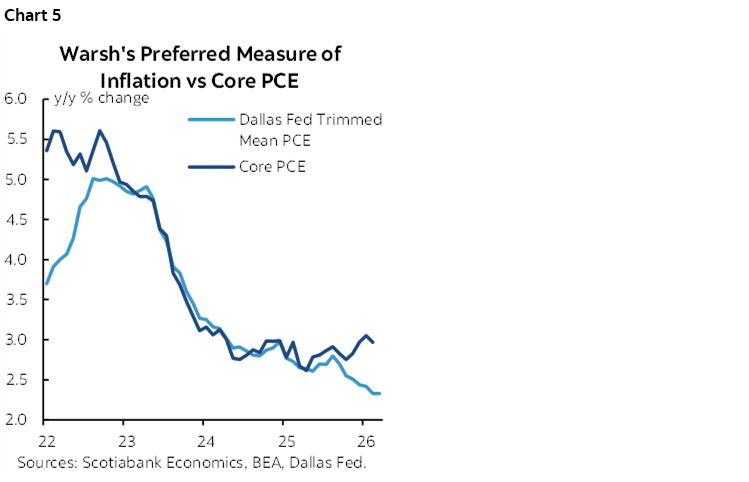

He prefers a different measure of core inflation which just so happens to be lower than traditional core PCE inflation. Golly, imagine that for a hawk turned dove midstream in the interview process. Warsh said he would launch a review of what is the best measure of underlying inflation and pre-judged the outcome by stating that "The measures I prefer look at trimmed averages ...."

Fed District banks already calculate trimmed measures. The Dallas Fed calculates trimmed mean core PCE that weeds out 24% of the lower tail of the weighted distribution or prices and 31 percent of the upper tail in the basket. Their current estimate is 2.3% y/y compared to core PCE at 3.2%. Chart 5 showcases the recent wedge between these measures.

The Cleveland Fed measures trimmed CPI which removes the top and bottom 8% of the distribution of prices for a total of 16% of prices that are weeded out. Their estimate is 2.6% y/y.

Ergo, this is a backdoor way by which Warsh could be more dovish, by shifting the goal posts on underlying inflation. There may be refinements and differences to how the District banks calculate the trimmed measures in terms of whatever is adopted by the Fed. Going forward, Warsh may be inclined to fade not just the food and energy components driven by the war with Iran, but the more limited part of the sample that would involve pass through into core and may be more likely to be weeded out of the trimmed mean measures.

Warsh must, however, convince the rest of the Committee that they should use his preferred measure of core inflation. For instance, here is Waller's speech from 2021 that served as an example of scepticism toward omitting parts of the basket. Waller said “...we may be led to "falsely" dismiss certain price movements and risk being misled as to the true inflation rate."

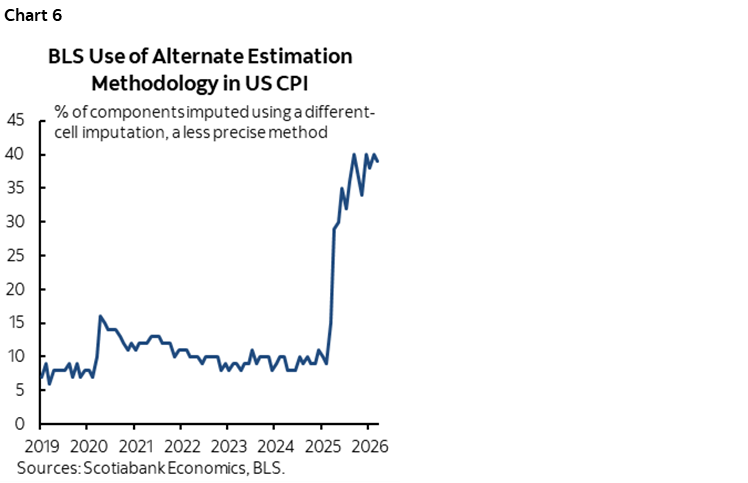

The other point to make about trimmed mean PCE or CPI is to be cautious not to over emphasize those measures when the underlying data is of such poor quality. About 40% of the basket is estimated by proxy methods because of budget cuts to the BLS and its failure to pivot toward other data collection methods (chart 6). When you start weeding out the tails you may be magnifying your reliance upon the low and falling quality of the distribution of prices because of the heightened sensitivity around small deviations that could be fake.

Regardless, the Fed would not be a pathbreaker if it adopted trimmed inflation as a preferred core gauge. They would follow in the footsteps of the BoC, RBA etc. An important caution is that there is a vibrant debate around what is the best core measure for Canada and some believe—including our group—that traditional core (ex-f&e) is best as a guide to achieving the headline inflation target and in its connection with the output gap measure of capacity pressures, in which case former Governor Poloz overcomplicated core inflation. The BoC itself is revisiting this issue in its five-year inflation renewal agreement project that is due by the end of this year.

3. He loathes forward guidance

Warsh was pretty direct on this point: "I don't believe in forward guidance" and "I don't believe people show up with rehearsed scripts, instead we have that family fight. I'm not one for pre-deciding what rates should be."

Warsh said decisions should only go meeting-by-meeting. What’s curious here is how he balances this anti-guidance preference with his view that AI is disinflationary and could motivate easing which is the penultimate form of multi-period forward guidance!

This anti-guidance stance will be tested and feels a bit naïve. It’s an obvious departure of the Fed's efforts on communications strategies to avoid game day surprises. Other FOMC members may well provide such guidance in one form or another, but Warsh may not. The stature of the other eleven FOMC members may rise in the lead up to the meetings. It’s all fine and well for, say, an EM central bank like Bank Indonesia to relish market surprises, but you’re the Fed. The Fed is the world’s single most important central bank. Fomenting greater volatility and uncertainty with surprise stances that could be destabilizing carries a greater burden.

Further, there may be times when forward guidance is vital. Say there’s a crisis between meetings or in blackout. Explicit forward guidance may be vital to calm markets. They may wish to influence market pricing directly in blackouts or indirectly through clandestine methods in the press that they’ve previously used.

4. A Bias Toward Juicing the Economy?

Warsh said more than once that "we have a window in which the economy is improving but I would say more improvement is possible." Does this imply a bias toward juicing growth and how is this reconciled with the dual mandate?

5. Backed Down on the Balance Sheet

Warsh has previously indicated a bias toward substantially shrinking the balance sheet that has made some folks in the markets a tad nervous. He backed down somewhat in his testimony by stating “That kind of regime change would have to be deliberate, well orchestrated, well choreographed and well described, so that unnecessary upset are not done to financial markets as we go to a policy regime change much more focused on interest rates.” Warsh repeated his view that the policy interest rate is the key tool which most folks would have already agreed with. He also noted “It took 18 years to create this balance sheet problem, and we won’t be able to fix it in 18 minutes. And so that’s why I think deliberation here is important.”

Warsh’s views on the balance sheet level and composition will be informed by market funding pressures. Push it too far and you’ll have another funding spat on your hands. His pledge to work with Treasury on the matter opens up a grey area. The details to the balance sheet plans and any potential compact with the Treasury will be key but Warsh will need to convince the Committee and markets and won’t be able to act alone.

6. No CBDC

Warsh clearly stated that the Federal Reserve under his leadership would not pursue a central bank digital currency. He said he agrees that the Fed has no right to issue a CBDC and that it would be a bad policy choice.

7. Miscellaneous

Warsh playfully said that as a Prof he gave everyone an 'A' because otherwise he'd get summoned by the Dean. I was surprised to see that no one went after him about whether that would be his style with Trump. I flatly don’t believe that Trump didn’t set expectations for Warsh’s stance on the policy interest rate during the interview process as Warsh claimed.

Warsh was accused of not answering questions on repeated occasions during his testimony with the implication being that he would not be a good candidate. On the contrary imo: not answering questions he is asked is a key skill for a top central banker! They are at least as much politicians as anything else.

Warsh said that "inflation comes about when the central bank prints too much." Really. There is a fair debate around that! Federal Reserve balance sheet expansion around the GFC and thereafter did not spark inflation for ages. Why? Because one has to consider velocity, money multipliers, whether expansion of narrow money is merely offsetting destruction of broad money like shadow money in a balance sheet driven recession, and other contributing factors.

Overall, it’s my impression that Mr. Warsh sounded much like what one would expect him to sound like—an idealistic young man who will need to learn a lot on the job and will see any preference for large changes being disciplined by markets, FOMC members and Fed staffers.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.