ON DECK FOR TUESDAY, APRIL 21st

KEY POINTS:

- Markets tread water ahead of tomorrow’s Iran negotiation deadline

- Warsh’s testimony may be a raucous affair

- Canada’s confirmation bias

- The Bank of (Central) Canada has a regional problem

- US nominal retail sales expected to be strong

- UK jobs, wages motivate higher BoE hike pricing

- NZ CPI pushes RBNZ pricing closer to hiking

- German investor sentiment hits lowest since ‘Liberation Day’

Sovereign bonds are under mild cheapening pressure concentrated toward the front-ends in the US, Canada, Eurozone and especially the UK post jobs. The dollar is broadly firmer with a notable exception being the kiwi dollar post cpi. Equities are in the black with mild gains across N.A. futures and European cash. Oil is treading water, watching and waiting to see if someone blinks on negotiations ahead of Trump’s latest deadline set for tomorrow night before it’s allegedly ‘bombs away’. Tacos for lunch tomorrow anyone?

Global market risk will focus upon Iran, Kevin Warsh’s testimony and US retail sales. Regional market risk was driven overnight by UK jobs and wages, plus NZ inflation. Canada will be quiet. Ditto for LatAm.

Warsh’s Raucous Testimony

Kevin Warsh’s confirmation testimony before the Senate Banking Committee will start with reading his written testimony at 10amET. Then the sparks will fly in what is bound to be a raucous affair.

Warsh’s written remarks were leaked yesterday (here). They failed to impress. Take, for instance, this remark:

"I do not believe the operational independence of monetary policy is particularly threatened when elected officials—presidents, senators, or members of the House—state their views on interest rates. Central bankers must be strong enough to listen to a diversity of views from all corners . . . humble enough to be open-minded to new ideas and new economic developments . . . wise enough to translate imperfect data into meaningful insight . . . and dedicated enough to make judgments faithfully and wisely. Simply stated, Fed independence is largely up to the Fed. "

This is weak and he'll be grilled on it. What he says is partly true, and it’s encouraging that he says “monetary policy independence is essential” but saying “I do not believe the operational independence of monetary policy is particularly threatened when elected officials—presidents, senators, or members of the House—state their views on interest rates” is very weak. When the President crosses the line with threats of firing and overt interference, a prospective Chair should blooming well stand up to it in unapologetic fashion. It’s your job and Warsh faces a lot of justified scepticism toward his chameleon ways including having gone from being relatively hawkish to feeding the impression he’d say anything in order to get the job.

Had the Board not pre-empted Trump by extending terms of the regional Presidents by 5 years, then the administration would have sought to mess with the regional board committees to effect change. That's a concern well beyond merely having a leveraged real estate President always preferring lower rates and higher inflation.

Warsh also appears to defer to the administration on other matters: “Fed officials are not entitled to the same special deference in their stewardship of public monies…or in bank regulatory and supervisory policy….or in areas affecting international finance, among other matters.” And “…the Fed must stay in its lane. Fed independence is placed at greatest risk when it strays into fiscal and social policies where it has neither authority nor expertise.” There is a lot of truth in that—including all the talk about fully-inclusive maximum employment that clouded Powell’s judgement in the pandemic and led to the massive surge of inflation—but there is a lot of mistruth as well. The Fed should have a say in bank regulatory and supervisory policy, for one.

There is nothing in his written testimony that offers an updated hint toward his policy stance or much of anything else for that matter. Warsh deferred to Trump’s view that US growth and real take-home pay will accelerate while ”economic growth potential is rising”, without saying how and why he believes this.

So onto the grilling we go and if the Senators do their jobs, then these are among the topics they’ll explore:

- Key will be any updated hints that he provides about his stance on monetary policy. He may be cagey and demure given that he’s not in office yet, but then again, he has hardly been cagey and demure to date during his attacks on the Fed’s policy stance, operations and management.

- He may repeat his bias that AI will be disinflationary and that this provides room for easing, but he will be grilled for evidence that probes further than simply being a Greenspan-esque view expressed on a lark at a Fed that has become much more transparent and Committee-driven today.

- How exactly does he see his ability to steer 11 other sceptical Committee members toward a quorum on monetary policy? Is he concerned about a perceived lack of credibility on the Committee? Will he be a lone dovish voice? Has his view changed because of the war or something else? Or will he behave very differently once in office and come under immediate attack by the President?

- His current stance on the US economy and risks to the dual mandate will figure prominently. He’ll be asked to put some meat on the bone when it comes to his optimistic take on the outlook for the US economy.

- He’ll be grilled on his views toward a potentially new Fed-Treasury compact. What variation of the 1951 compact may he pursue? How will he protect Fed independence from an intrusive administration?

- He may be asked under what conditions he would consider QE, if any, given his outspoken opposition that led to his resignation after the GFC.

- His finances and lack of full disclosure will be one issue.

In short, his outspoken ways to date and apparent willingness to say anything to get the job will put him on the hot seat. And then there are the unanimous Dems who wished to have the hearing delayed plus opposition by GOP Senator Tillis due to Trump’s petty, vindicative pursuit of Powell. Needless to say, the path forward appears to be rather complicated.

BoC — Confirmation Bias and Inflation Expectations

It feels like Canada has a wicked case of confirmation bias whereby people don't want to see or believe any evidence of inflation. I see that across the street and across the local media. This clouds their judgement. They can't read the data for what it's worth in objective fashion.

Take yesterday’s inflation report for one. My take pointed to clear signs that Canada may be emerging from a temporary soft patch on core inflation. TM and WM core inflation accelerated to the 2–3% range in m/m SAAR terms which is just one month but tentatively fits the concern that the prior few months of softer readings were temporary even before the war, like early 2024. Core industrial price pass through has long been flashing warning signs on core CPI. Traditional core CPI was held back by one main category in March—clothing and footwear—and after controlling for this the reading was considerably stronger. Breadth of price increases remains elevated. And these are all pre-war readings. What everyone else was looking at was a mystery to me as they focused on gas, headline, and the year-over-year trimmed mean and weighted median measures that turn at glacial speed relative to higher frequency measures. They were amazed that headline was weaker than they expected when the reason for that was simply because they went too high with their estimates!

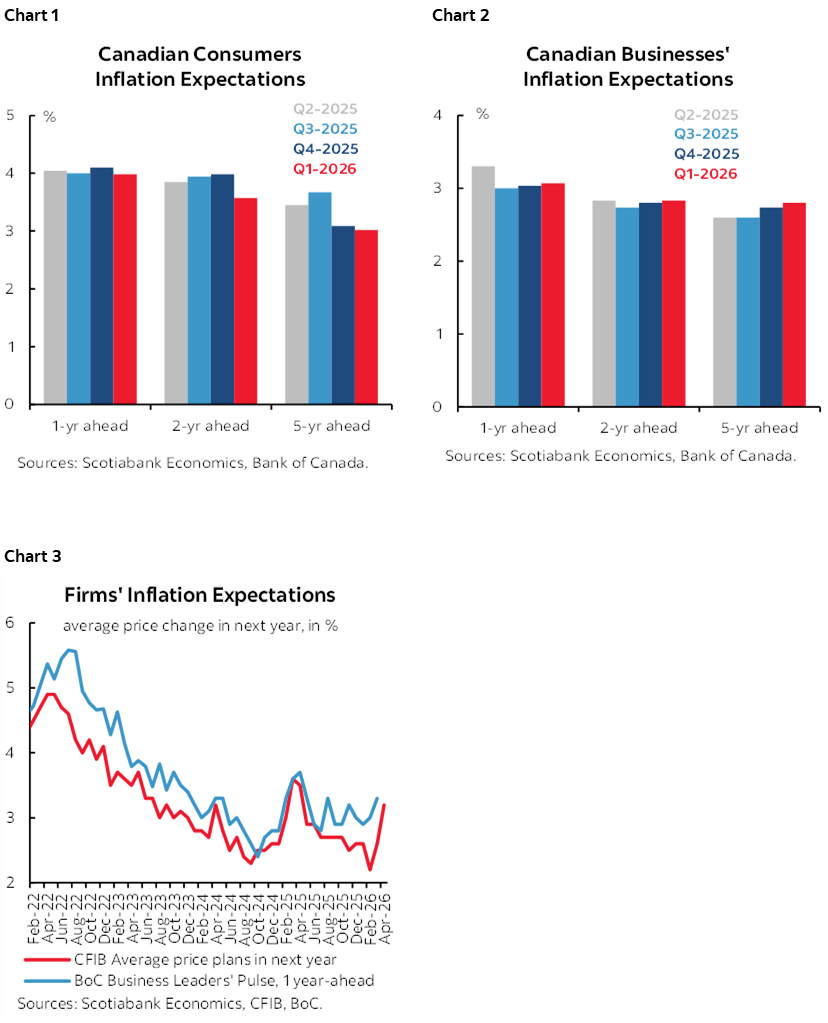

Then take the BoC’s lagging surveys (here, here). They preceded the war’s effects since they are sampled during February. And yet they are elevated across all measures in a way that Governor Macklem said would concern the Bank. Macklem said on Friday that elevated medium- and longer-term inflation expectations would concern them. They got that in the surveys that include measures out to five years and less so in the CFIB's fresher but short-term measure (charts 1–3). All of these measures show medium- and longer-term inflation expectations above the inflation target. They are not great gauges to be sure, as businesses and households often have a poor understanding of inflation, but we can’t dismiss the fact they were elevated even before the war. Wait until the next survey readings in…..July, and lagging once again by being sampled in May.

There is high uncertainty toward the path forward. There is, however, no excuse for filtering out evidence people don't wish to see and yet so much of the coverage is doing so. This is very reminiscent of the early days of the pandemic when the street and the press had horse blinders on and only saw what they wished to see.

US Macro Readings

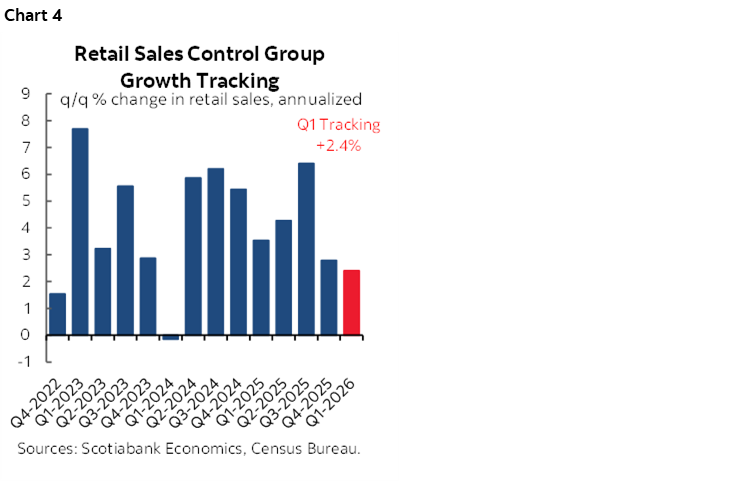

US nominal retail sales during March (8:30amET) should post a strong headline gain where I’m above consensus given estimates for vehicle volumes and prices, gasoline price effects, and core sales (where I’m ranked #1). I don’t get how consensus can have headline and ex-autos being equal given that new vehicle sales were up by almost 4% m/m SA; maybe it’s just a sample quirk. Sales are tracking slower but ok growth in Q1 to date (chart 4).

Other minor gauges include ADP’s weekly private payrolls estimate (8:15amET) that will be watched to see whether the prior week’s jump to 39k—or 157k at a monthly rate—was just a flash in the pan. Pending home sales during March are coming off the first gain in three months (10amET).

UK Job Market Conditions Add to BoE Policy Tightening

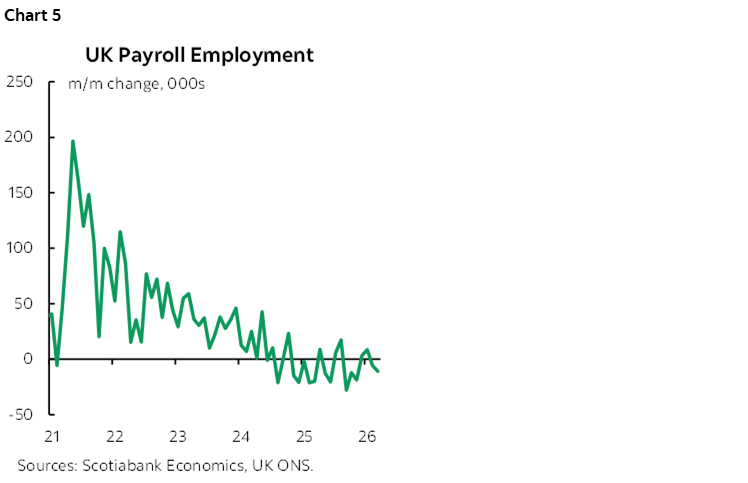

UK job market conditions were updated and the outcome motivated a mild increase in expectations for cumulative policy tightening by the Bank of England this year. Year-end OIS meeting pricing for Bank Rate moved up by 8bps to one-and-a-half quarter point hikes and a couple of points of priced tightening was added for the June meeting which is now roughly 50–50.

- Payroll employment fell by 11k in March and the prior month was revised to a 5.7k decline after two prior mild increases (chart 5).

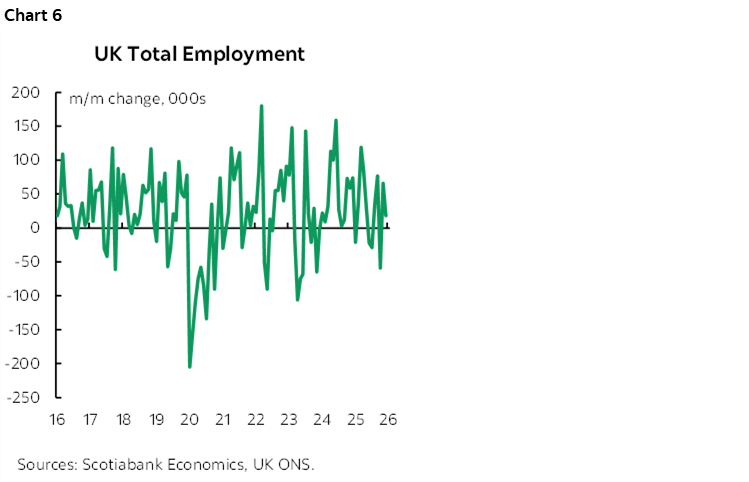

- Total employment lags by a month and was up by 18k in February after a 66k prior increase (chart 6). Total employment has been up in four of the past five months.

- The unemployment rate fell by three-tenths to 4.9% in February. That’s the lowest since August.

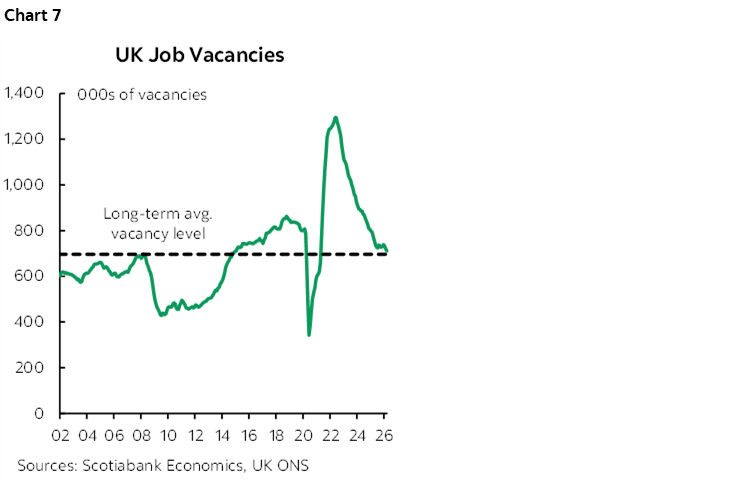

- UK job vacancies edged a touch lower to 711k in March from 721k in February and remain roughly around the long-run average (chart 7).

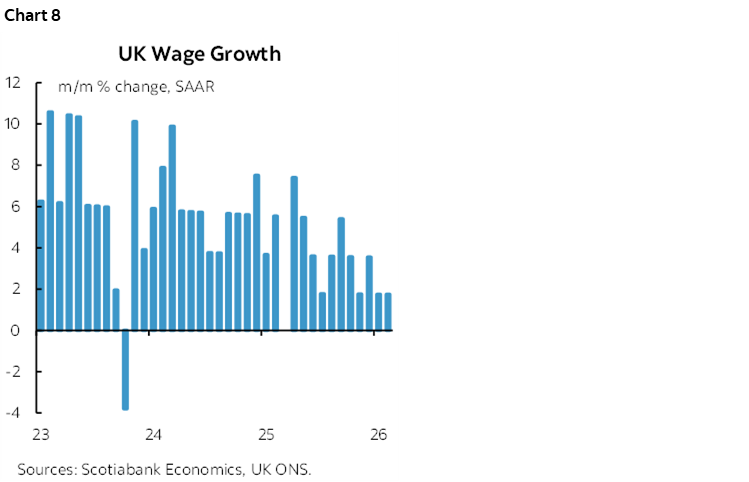

- Wages grew by 1.8% m/m SAAR for a second consecutive month which dropped the three-month moving average to 2.4% m/m SAAR. Wage growth is clearly on a decelerating path (chart 8).

It’s fair to note, however, that the ONS is facing low response rates and elevated revision risk around these estimates.

Kiwi Inflation Motivates Further RBNZ Tightening Expectations

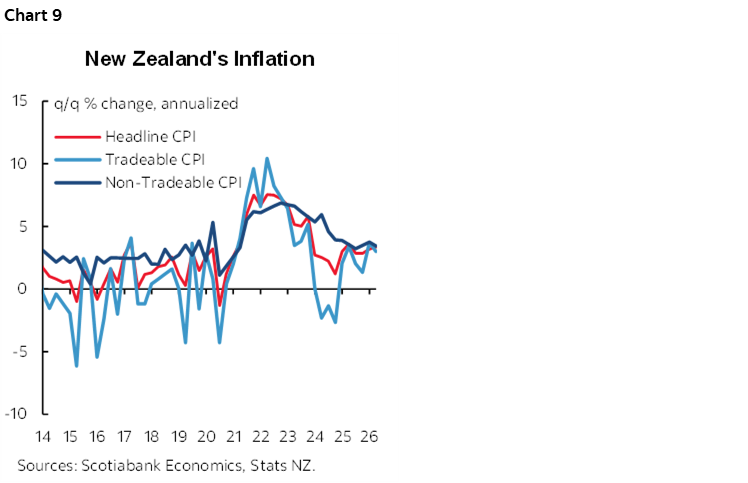

NZ CPI inflation accelerated to more than expected in Q1 which motivated more aggressive pricing for RBNZ policy tightening. CPI was up by 0.9% q/q SA nonannualized (0.8% consensus) and 3.1% y/y (2.9% consensus). Tradeable CPI increased by 0.7%, a tick above consensus, with non tradeable CPI up 1.1% (0.9% consensus). Annualized rates are shown in chart 9. Pricing for the May RBNZ meeting doubled to about 10bps of a quarter point hike with full-year pricing up by a few points to a cumulative hike of about 75bps.

German Investor Sentiment Hits Lowest Since ‘Liberation Day’

German ZEW investor sentiment fell to the lowest level of expectations since last April which included Trump’s disastrous ‘Liberation Day’ assault on common sense economic policies.

The Bank of (Central) Canada

Congratulations to the two new Deputy Governors at the Bank of Canada (here). Their appointments follow the sudden departure of Rhys Mendes on April 10th and the retirement of Sharon Kozicki with July 15th slated as her final day at the bank (here). The reason it only took a month to announce their replacements is because no public search was conducted as the BoC had guided that the spots would be filled by internal candidates.

And yet the Bank of (Central) Canada lacks regional representation. It’s entire Governing Council now hails from the three provinces of Quebec (3, Macklem, Vincent, Gosselin), Ontario (2 Gravelle, Alexopolous) and Manitoba (1, Rogers). Both of yesterday’s appointments are from Quebec with an election to be held in October. If western alienation is a concern in this country, then you couldn’t tell by the workings of the BoC.

I fully expect the two new appointees will do their jobs as professionals in setting monetary policy that is appropriately designed for the country as a whole. Besides, how Macklem steers the discussion and bias is the key. Yet the BoC is supposed to represent voices from across the land and could have someone from the four east coast provinces, but it’s western Canada’s omission that sticks out in terms of having two of the four biggest provincial economies in the country and with no representation on Governing Council. Perhaps at least the part-time external deputy governor should come from western Canada. Maybe that one should have some market experience as well in order to fill a void of external market savviness on the Council.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.