ON DECK FOR MONDAY, APRIL 20th

KEY POINTS:

- Risk off as Iran tensions flare again

- Canadian CPI: nothing hangs in the balance on an expected surge

- BoC surveys to be stale on arrival

- Global Week Ahead—The Equity ‘Puzzle’ (reminder here)

Risk appetite is on the run to start the fresh trading week. Oil is up by 5–6%. US equity futures are down by about -½% with European equities down by about double that amount. The dollar is slightly firmer against most majors except for CAD and NOK. Sovereign bond yields are up by around 2–6bps across regions and maturities with Europe underperforming US Ts.

As suspected, Trump grossly overstated progress toward an agreement with Iran on Friday; I wonder who profited. Iran said on Saturday that Trump was misrepresenting negotiations. Iran shut the Strait of Hormuz while stating that maintenance of the US embargo was a violation of the ceasefire. Iranian boats attacked a ship in the Strait. Yesterday, the US boarded and seized an Iranian tanker after firing on it following allegedly multiple warnings to turn around in the Strait. Trump has been attempting to talk up negotiations in Islamabad on Monday evening with the same amateurs that failed the first time; Vance, his son-in-law, and Witkoff. Iran says that they won’t be there but also that no decision has been made yet on whether to eventually rejoin. Trump resurrected his threat to bomb bridges and power plants if Iran doesn’t come around. Both sides face reasonable expectations of future war crime charges.

There was otherwise very light calendar-based risk through the overnight. German producer prices soared in March (+2.5% m/m, consensus 1.4%). China left the 1- and 5-year Loan Prime Rates unchanged at 3% and 3.5% respectively which surprised no one.

CANADIAN INFLATION — NOTHING HANGS ON THIS ONE

Canada updates CPI for March this morning and three hours before the BoC’s lagging and stale consumer and business surveys are released with Q1 results skewed toward February and hence pre-war. Detailed previews and views on both including a focus on the Bank of Canada are included in my weekly.

Consensus sits at 1.1% m/m seasonally unadjusted. I’m at 0.9%. The range is from 0.9–1.3%. Estimates for the year-over-year rate run from 2.4% (me) to 2.8% with a median of 2.6%. We’re all high with slight variations on a gasoline—and fuel-driven spike as the main driver of the month-over-month gain plus typical seasonality. The year-over-year rate is also buoyed by resetting the base effect from last April’s elimination of the consumer portion of the carbon tax.

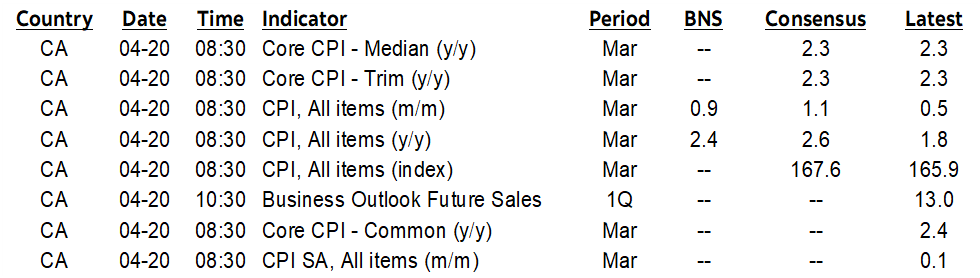

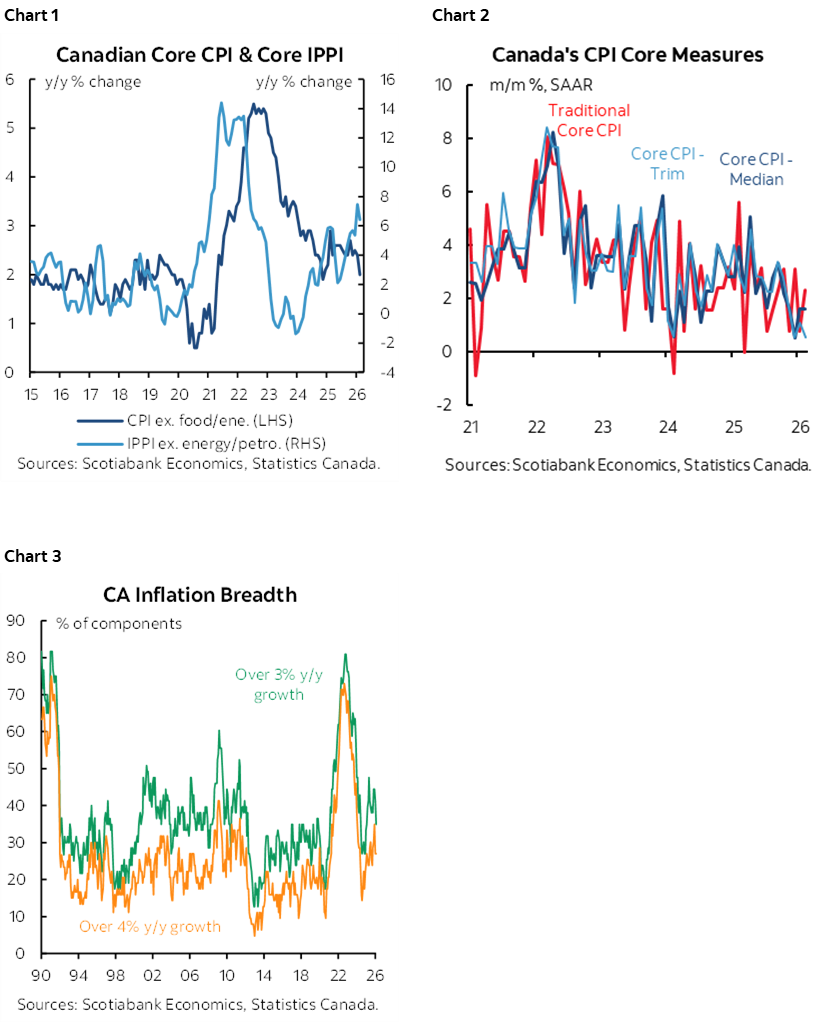

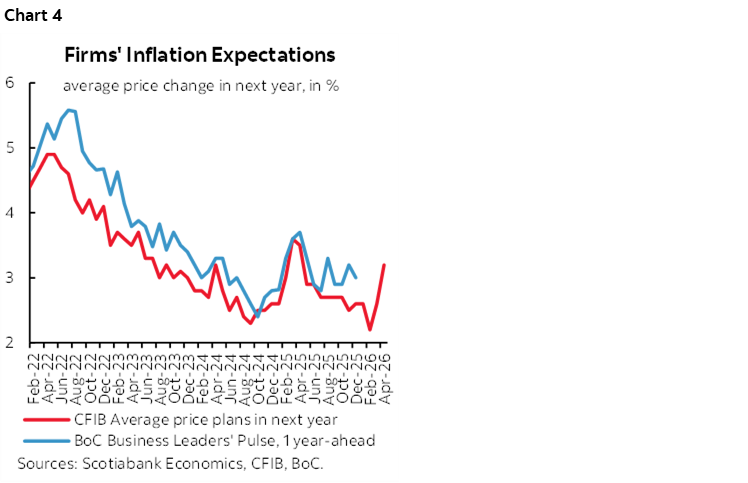

As argued in my weekly, the soft patch on core inflation measures was viewed as probably temporary even before the war and potential pass through of higher commodities entered the picture. Core industrial prices were already surging and lead core CPI inflation (chart 1). The dip in core measures over recent months is hardly unprecedented—early 2024 was another such period (chart 2); note that the measures are not all aligned as traditional core has often been warmer. Also monitor breadth of inflation (chart 3).

THE BOC’S SURVEYS WILL BE STALE ON ARRIVAL

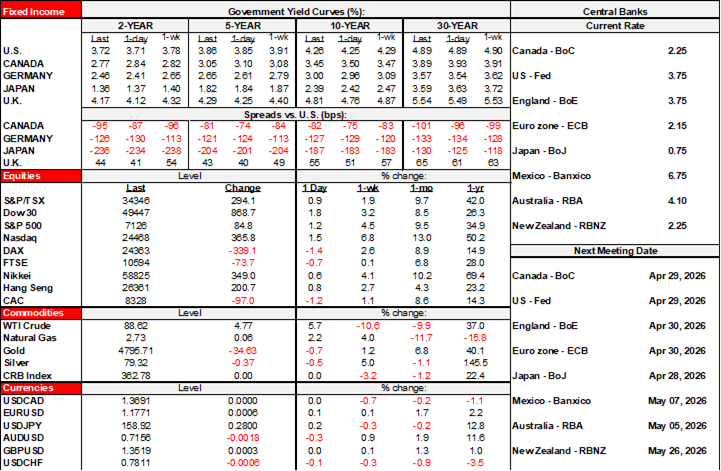

The Bank of Canada’s twin Business Outlook Survey and Survey of Consumer Expectations arrive three hours after CPI (11:30amET). Watch the measures of inflation expectations, but not too seriously since they lag with the responses skewed toward February and hence before the war. The CFIB—a small business association and lobby group—produces a timelier survey of inflation expectations for April and showed a sharp pick-up in one-year ahead expectations that tend to lead the BoC’s survey (chart 4).

In any event, no policy decisions hang in the balance on this report. Governor Macklem remarked on Friday that “We’re all feeling like you don’t want to jump too early and raise interest rates and lower growth, particularly when growth is already weak. On the other hand, you don’t want to be late and let inflation get a hold and get entrenched.”

What I heard in that was a clear bias toward hike risk with uncertain timing. April sounds out, but meetings thereafter have to be treated as ‘live’—pending further developments.

GLOBAL WEEK AHEAD—THE EQUITY 'PUZZLE'

As a reminder, please see my weekly that was sent out on Friday here. Key topics that are explored include the following list:

Possible explanations for the ‘puzzle’ of resilient equities

- An Iran deal — truth or dare

- Canadian inflation is set to soar…

- …and how behaviour and policy could reinforce the effects

- How the BoC could respond

- BoC surveys to be stale on arrival as more timely gauges rise

- Warsh’s Senate hearing will be a raucous affair

- Canadian consumer spending is tracking strongly

- So are US retail sales

- BI to hold

- BSP may hike

- So might Turkey’s central bank

- Russia’s central bank shouldn’t cut, but might

- UK: Jobs, wages, CPI and retail to inform BoE’s next move

- Global PMIs to offer fresh insights into shock effects

- US earnings season continues

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.