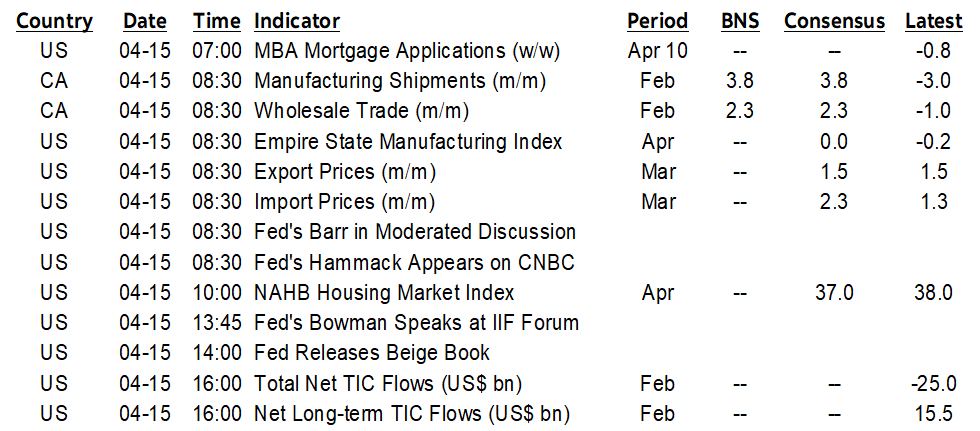

ON DECK FOR WEDNESDAY, APRIL 15th

KEY POINTS:

- Stocks and bonds treading carefully…

- ...as the core issue of who to trust concerning Iran remains very much uncertain

- US bank earnings continue

- IMF-World Bank Spring meetings are bringing out the herd of central bankers

- US: Empire, import prices, NAHB, Beige Book

- Canada to post strong gains in manufacturing, wholesale

- Canada’s fuel tax cut to offer minimal, temporary effect on CPI

Who to trust? Shall it be Trump, or Iran? That remains the dominant debate hanging over global markets as Trump says the war is almost over, talks may begin in a couple of days, and that oil will fall back to pre-war levels and ‘maybe lower’. Iran, meanwhile, threatens to block Red Sea shipping lanes presumably with help from the Houthis should the US blockade continue. A headline hit a short time ago that the two sides have reached an agreement in principle to extend the truce that was to expire one week from today.

So, in waltz doe-eyed markets this morning only to add a buck or two to near-term oil futures prices, while equities and sovereign bonds are generally little changed with a slight cheapening bias across global benchmarks and the dollar is slightly firmer against most major crosses except for the A$ and krone.

Yet trust was broken so, so long ago on so many matters. Nobody knows where Iran is storing its uranium stockpiles. Iran still controls the Strait. Iran still wants Israel to stop attacking Hezbollah as the bilateral attacks continue. The Iranian regime still essentially remains in place and is arguably more dangerous than before. Iran still has a long list of other demands. The Arab world is more divided by the hostilities than previously. If the war were to end tomorrow and US forces withdraw, then the US and Israel will have been beaten without accomplishing the top goals and arguably making things worse with a total mess left behind. The long-run risks remain elevated along a similar path of risks to those that were courted after the Gulf War of 1990 and the two decades that followed.

The issues of duration and magnitude of the conflict and its impact upon commodities, passthrough into core measures of inflation and persistence will loom large over the Spring IMF-World Bank meetings that began on Monday and last until Saturday. Those meetings will bring out comments from several central bankers both formally and informally. Bailey (11:50amET, 2pmET) and Lagarde (3:30pmET) are on today’s formal line-up after the latter just said last evening that looking through the shock effects would be “a serious mistake” but that it’s too early to say.

Any central banker may speak from the sidelines at any point and that includes the BoC’s Macklem who usually holds a closed door meeting with journalists later in the proceedings who then report on the contents with their own filter applied to what was indicated.

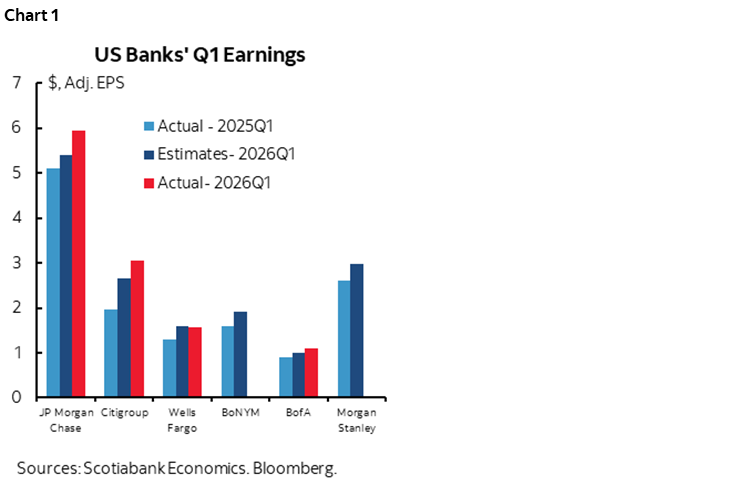

US bank earnings season continues with BofA and Morgan Stanley releasing this morning. BofA beat EPS expectations (US$1.11, consensus $1.01) while beating expectations for equities trading but falling short on FICC trading. Morgan Stanley releases at 7:30amET. Chart 1 summarizes EPS tracking so far.

US data risk will be modest including surging US import prices in March (8:30amET). The Empire gauge of manufacturing activity around the NY Fed’s district kicks off the march to the next ISM-manufacturing print (8:30amET). NAHB homebuilder confidence including model home foot traffic that used to serve as a guide to new home sales before investors took over will be updated (10amET). The Fed’s Beige Book of regional conditions (2pmET) used to matter more before regional Presidents began talking so often.

Also on tap is strong Canadian data including large, expected gains in manufacturing and wholesale trade during pre-war February (8:30amET).

This follows yesterday’s announcement to expect a Spring fiscal update on April 28th and the gas tax cut announcement that offers minimal effects. The cut will knock about 0.1% off of m/m April CPI when prorated and probably another 0.1 off May when the full month is affected. Then the cut shakes out from June until September, after which its reversal would add back around two-tenths to October CPI. Key are whether its just a cut for the Summer driving season, whether margins across refiners and retailers crowd in the space, and whether it gets passed on or absorbed in profit margins of businesses that use a lot of fuel. The BoC’s preferred core measures of inflation—trimmed mean and weighted median CPI—exclude the direct effects of changes in taxes and the indirect effects are likely to be very small.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.