ON DECK FOR TUESDAY, APRIL 14th

KEY POINTS:

- Stocks and bonds richen on cautious war optimism

- Mixed US bank earnings

- Why the Fed slowed balance sheet expansion

- Peru’s election results are still pending

- Implications of Canada’s majority

- US PPI to soar on commodity prices

- Lagarde to speak as central bankers huddle in Washington

US bank earnings—including solid earnings but various forms of weaker than expected guidance—and developments in the Middle East are dominating an otherwise dull set of calendar-based developments perhaps with the exception of Lagarde’s speech after the close. The implications of the Carney administration’s majority outcome will begin to become clearer right away this morning.

Stocks are sovereign bonds are richer across almost all major markets this morning as oil prices slip a touch while the dollar is broadly weaker.

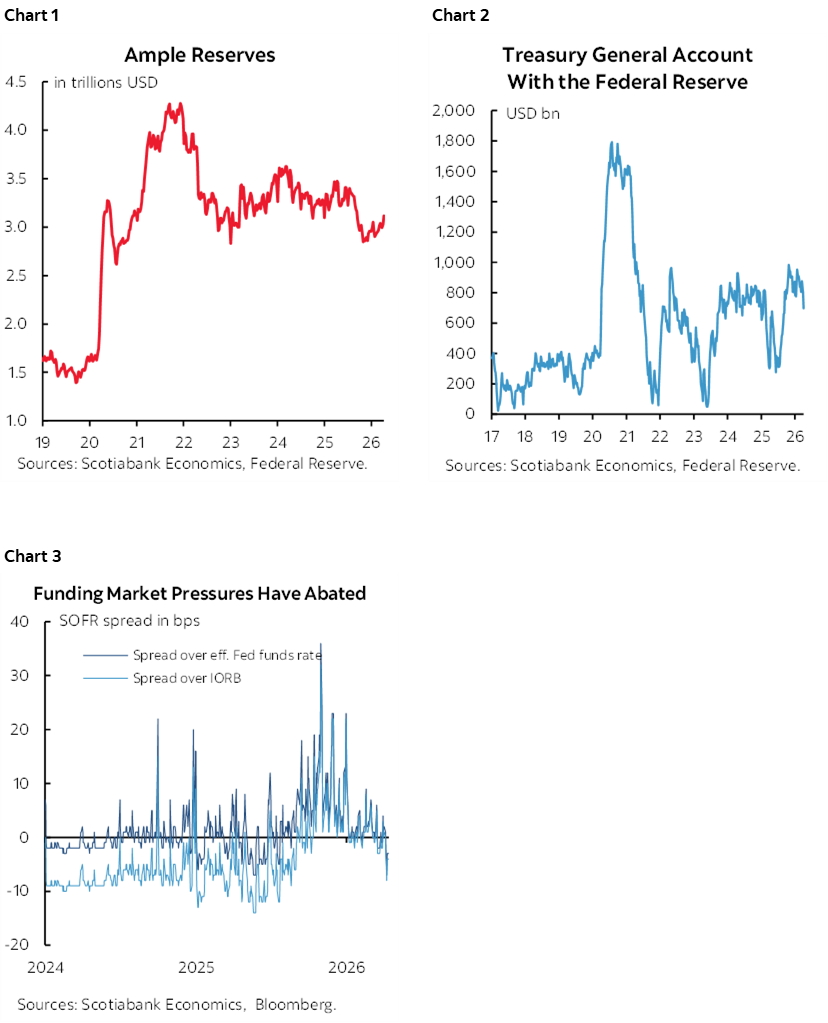

Fed Slows Balance Sheet Expansion

Markets are digesting the Fed’s significantly anticipated move to lower t-bill purchases from US$40B/month to $25B/month through May; the magnitude of the decline was bigger and more sudden than many anticipated, but the general reduction was telegraphed well in advance. It means that the Fed’s ample reserves framework will be padded by less each month than when they ramped up bill purchases and shifted toward expanding the balance sheet late last year (chart 1). The aim then was to counter persistent overshooting of money market rates relative to effective fed funds especially through the tax season. The Treasury General Account has held up as tax refunds have generally come in lower than the more optimistic scenarios (chart 2). Mission accomplished on funding pressures for now, perhaps until the next set of risks (chart 3).

Peru’s Election Results Are Still Pending

Peru’s first-round election results are still pending. Fujimori on June 7th—whether it’s a leftist or another right-leaning candidate. Two relatively right-wing candidates could be received more positively by local markets than a split.

IMPLICATIONS OF CANADA’S MAJORITY

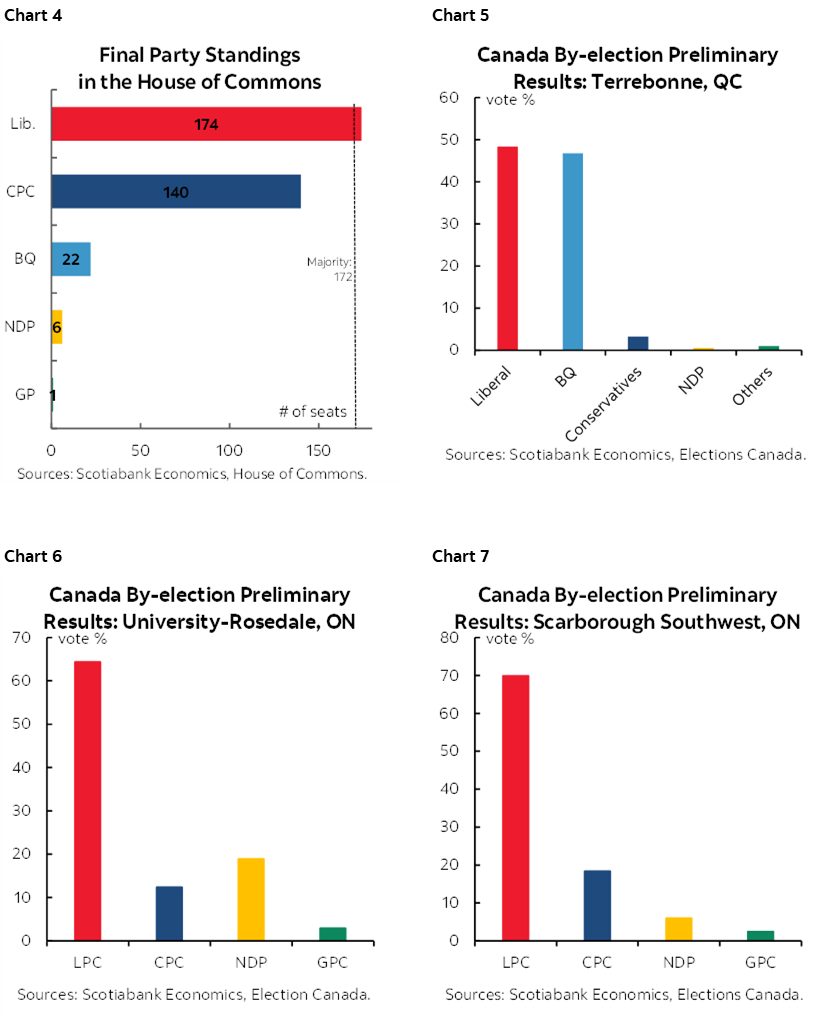

The federal Liberals secured their long sought after majority by winning all three by-elections last evening. You could have run two gerbils in red sweaters and they would have won the two Toronto ridings, but the Quebec riding win was achieved with a wide enough margin to put to rest the contest against the regional BQ. The result gives the Libs 174 seats in Parliament, or two more than needed for a majority. See charts 4–7 for results.

Markets are ignoring the outcome as CAD and bonds are snoozing throughout it all because a) the majority outcome was generally expected well in advance in the wake of floor crossings and by-election calls, and b) because the real test for the economy, fiscal policy, monetary policy and markets will come in the form of how the Carney administration uses its majority.

Anonymous Liberal party members have remarked in the press that they continue to explicitly target up to eight more opposition MPs to cross the floor. So, which narrative is correct here: the disaffected are tripping over themselves to voluntarily cross the floor to the innocent Liberals who are merely standing with open arms to welcome them? Or you are deliberately poaching them with backroom deals that lack needed transparency to maintain faith in a democracy? Seems like primarily the latter with a touch of the former to me. I wouldn’t care which party was doing this in judging the outcome to be a blow to democracy.

Even more turncoats could conceivably strengthen the majority further, which could offer some padding if any of them turn out to be disloyal to future initiatives, not like they’ve ever demonstrated such a tendency! Some are doing so by sacrificing long-held beliefs which further raise suspicions about what has been offered. Bear in mind, however, that without five turncoats, the Libs would still have a minority which is what voters chose last April. Voters did not choose to give the Libs a majority; that was accomplished through backroom dealings. I wouldn’t be surprised if one day Trump says Canada’s election was stolen which is a fairer debate than his ridiculous charges about his own country. He could turn this knife in trade negotiations simply because it would suit his own domestic political agenda.

Nevertheless, PM Carney is wasting no time with his newfound majority government. He plans to announce new affordability measures at a press event this morning (10amET). They are reportedly focused upon gasoline and diesel prices. With any luck he won’t blow it by returning to the never-ending handouts that characterized his predecessor’s government and its endless ‘fairness’ mantra that ignored the need to foster more rapid growth which was the greatest fairness sin of all. Address the bottom earners’ challenges through growth. My hope is that whatever is announced is very limited and very targeted while sticking to the plan of extending the average duration of the government’s spending plans to address underperformance in areas like resource development, infrastructure and defence. Those areas, however, carry high uncertainty in terms of deficit projections given they are globally notorious for cost overruns and delays.

Watch for the date of a Spring fiscal update after FinMin Champagne held consultations with private sector economists in Toronto last month on a day when key ones were tied up with the BoC and Fed communications. Today’s presser may start the advance announcements on the path to a mini budget of sorts.

It’s widely understood that the federal deficit is coming in lower than anticipated for FY25–26. That may be a combination of decent growth in the domestic economy as a subset of soft GDP figures, plus surging revenues from taxing coating commodity prices, plus perhaps slow roll out of some initiatives.

As deficit tracking looks more favourable, the temptation may be to spend the surprise and book a bunch of last-minute initiatives. That would extend past practices at the expense of the deficit if it happens.

And it’s not just the Feds we’re talking about. Quebec’s newly minted Premier, Christine Fréchette, has pledged to introduce new measures to address affordability challenges in the coming days after being sworn into office tomorrow. Quebec faces an election in October. The pressure amid current polling is clearly to offer more goodies to voters. Again, the hope is that these are limited and targeted measures.

Absent ‘limited and targeted’, or if there are too many of them across all levels of governments, the cost could be to further strengthen the case for monetary policy tightening as the country imports a massive positive income shock through soaring commodity prices.

US BANK EARNINGS

The US bank earnings season intensified this morning. The results were not particularly impressive to share prices. BlackRock beat expectations (Q1 EPS $12.53, consensus $11.48). JP Morgan Q1 EPS beat consensus expectations for EPS of US$5.43 by about fifty cents, but shares fell in the pre-market on weaker than expected forward guidance for revenues including net interest income. Wells Fargo shares also fell in the pre-market after Q1 earnings that posted soft details. Citigroup posted EPS of US$3.06 (consensus $2.63) with solid revenues.

Other Stuff

The US releases producer prices during March this morning (8:30amET). It’s a done deal that headline prices will soar on the back of higher energy and other commodities, but watch for core prices ex-food and energy that have been rising at an accelerated pace over the past three months.

ECB President Lagarde speaks after the close this evening (5pmET) as she’s in Washington for the annual IMF/World Bank meetings with markets pricing just over a 40% chance at a hike on April 30th. Chair Powell will attend his last meeting as Chair. Watch for signs of narrative shifts across the herd whenever central bankers coalesce in one spot.

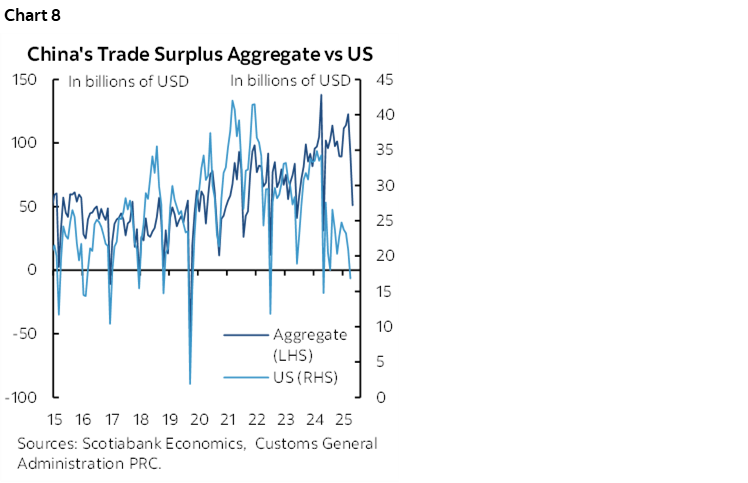

China’s trade figures for March posted weaker than expected exports and stronger than expected imports. The result narrowed the trade surplus both in aggregate and in relation to the US (chart 8). Commodity price effects were a major driver of the import side which in my opinion doesn’t alter the other part of the narrative that posits China’s trade position has generally held up better than feared as trade found ways to worked around US tariffs.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.