ON DECK FOR MONDAY, APRIL 13th

KEY POINTS:

- Oil prices spike after US-Iran talks predictably fail

- Iranian blockade courts high risks

- Welcoming the defeat of Hungary’s Orbán

- Canada will have a majority government by tonight despite affordability failings

- Peru's first-round election continues after irregularities

- US bank earnings season kicks off

- US home resales expected to be little changed

- Global Week Ahead—Affordability Versus the Strongman (reminder here)

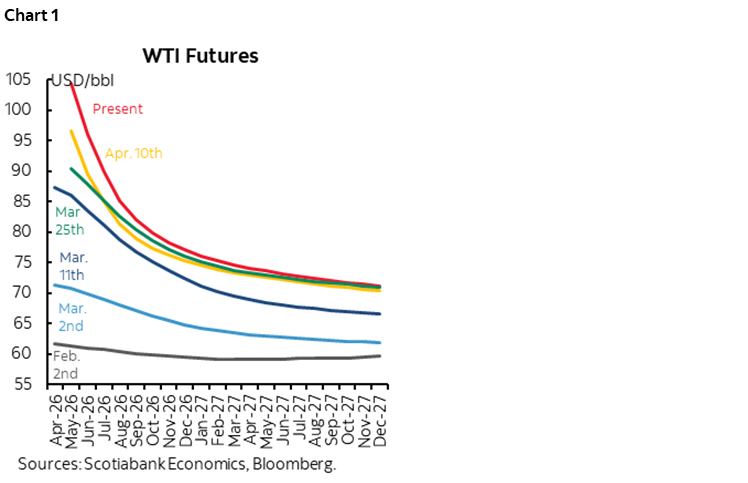

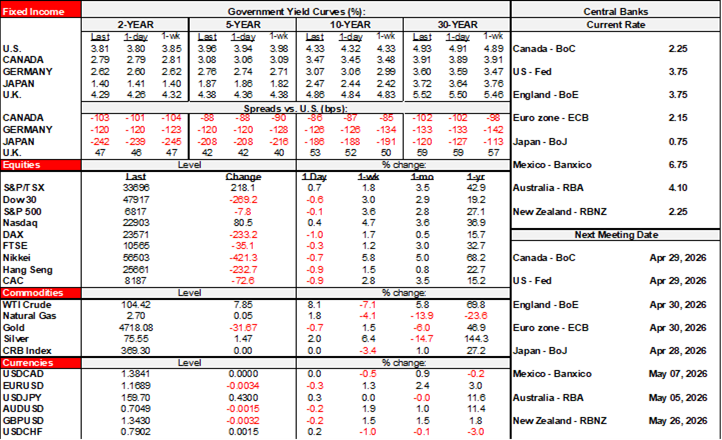

Global markets are on the backfoot to start the week given what was the largely predictable collapse of negotiations between Iran and the US. Oil prices are sharply higher with WTI and Brent futures gaining by about US$7–8/barrel and trickling into other maturities (chart 1) alongside increases in other commodity prices. Gold is off by about $40/oz but was down by about $100 early in the Asian session. The dollar is firmer against other majors but with the krone and ruble gaining while CAD holds firm, both of which are outperforming other crosses due to higher commodities. US and Canadian equity futures are off by about 1/2% which is fairly modest thus far, but European cash markets are faring a little worse. Sovereign bond yields are higher by a handful of basis points across major markets and maturities. OIS is leaning toward a half point of BoC hikes over H2 but you wouldn’t know the case if you only read Bloomberg.

RECAP OF US-IRAN DEVELOPMENTS

US-Iran talks failed this weekend. Trump has demanded that the Strait of Hormuz be opened and insisted that Iran cannot have nuclear weapons, both of which have been rejected by Iran. Plenty of other issues remain in place as serious impediments alongside Israel’s behaviour.

Oil is up partly because Trump and later clarifications by officials and the US navy have said that the US navy will blockade ships entering or leaving Iranian ports starting at 10amET today but qualified that by somewhat confusingly clarifying later in his post that only those ships that have paid a fee to Iran will be blockaded. That may imply they won’t block ships that don’t pay the fees, but this raises the issue of how to confirm and track the fees. Ships not entering and leaving Iranian ports will not be blockaded which may raise unintended effects such as ensuring your last port of call wasn’t Iranian but earlier ones may have been.

One other issue involves what tension might arise if the US navy blockaded, say, a Russian, or Chinese ship. At some point there may be a test. The US does not have the right to do so in international waters. Another point is that a naval blockade wouldn’t mean Iran is starved of imports as in the case of other forms of blockades in history. It has multiple modes of transport from other regions including air, land, and via the Caspian Sea and its canal link to the Black Sea and Russia.

Iran has vowed to respond to any military vessels in the strait. The Trump administration is contemplating limited strikes.

HUNGARIAN ELECTION STRENGTHENS EUROPE

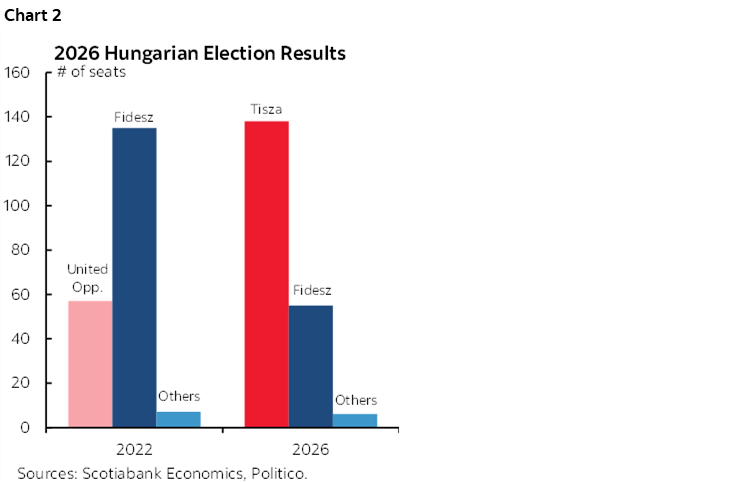

Other than NOK and CAD, a small exception to broad dollar strength is the Hungarian forint after Orbán was smoked in yesterday's election as the opposition won a two-thirds majority (chart 2). The forint is up by 2% to the dollar this morning. Markets love Hungarian bonds this morning with the 10-year yield down by about 40bps. Naturally I look to the economics behind it and a core issue was affordability as CPI skyrocketed while the forint fell by 50% to the dollar and the euro since he came back to power in 2010. Ergo, it’s a clear warning to Trump where tariffs and war alongside broader uncertainty and falling investment outside of AI are adding affordability pressures against his election pledges, hence why he and Vance were interfering in Hungary’s election which may well have done more harm to Orbán. It remains to be seen if Orbán’s opposition to EU initiatives—like a cohesive plan about what to do with Russia and the Ukraine war—will benefit accordingly among other matters.

CANADA TO GET A MAJORITY GOVERNMENT BY TONIGHT

Polls close at 8:30pmET on three by-elections today. The Liberals need to win just one of them to secure 172 seats and hence a majority in parliament. They are very likely to win two of them and quite possibly all three. The goalie in PM Carney may call that a hat trick. See the section on this topic in my weekly for more.

Yet Canada is looking somewhat anomalous to the narrative that failure to address affordability issues costs governments. Carney has been PM for just a year while much of his cabinet is made up of carryovers from prior Liberal governments. They'll be untouchable by voters until 2029—outlasting Trump and likely securing an even bigger majority as the Liberals continue to undemocratically poach turncoat members of other parties.

PERU'S ELECTION CONTINUES

Peru's election continues today because of election irregularities focused upon missing ballots. So far, we know that Keiko Fujimori will advance to the second round on June 7th. The highly divided field is still contesting for the second and final spot to reach the final run off and key to markets may be whether that second spot goes left or right.

US BANK EARNINGS AND HOUSING

The US bank earnings season kicks off with Goldman due out before the open (consensus EPS US$16.34).

US home resales during March (10amET) are expected to be little changed from the prior month’s 4.09 million annualized rate.

GLOBAL WEEK AHEAD—AFFORDABILITY VERSUS THE STRONGMAN

And as a reminder, please see the Global Week Ahead—Affordability Versus the Strongman (here). Key topics include:

- US-Iran negotiations kick off amid widespread disagreement, elevated risk

- The Q1 US earnings season starts with financials

- US financial regs & the cycle—right time for a lighter touch?

- Canada is very likely to have a majority government this week

- Orbán out? Hungarians paid a steep price during his tenure. Literally.

- Warsh’s delayed confirmation process is rather complicated

- Peru’s first round Presidential election unlikely to reveal a winner

- Aussie jobs report to segue into the next RBA decision

- Strong data due in Canada

- US producer and import prices likely surged

- China’s economy is still looking resilient

- Global macro

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.