ON DECK FOR FRIDAY, APRIL 10th

KEY POINTS:

- Bland markets await US CPI, Cdn jobs, next week’s developments

- US CPI preview

- Canadian jobs preview

- BoK held but short rates exploded on guidance

- BCRP held with dovish guidance ahead of elections

- China’s CPI inflation ebbed

- US UofM, factory orders due out

Iran headlines will continue to dominate market action, but data might be worth a glimpse or two this morning. The market tone into US CPI and Canadian jobs is rather bland. US equity futures are flat, with TSX futures up a touch and European cash markets up by ¼% to ¾% that followed overnight gains across key Asia-Pacific benchmarks. Oil prices are little changed with Brent and WTI still hovering in the high-90s. Sovereign bond yields are up a few points across maturities and regions with EGBs and gilts underperforming US Ts and Canadas. Currencies are divided.

Previews of US CPI and Canadian jobs follow. Also note the context into forming expectations and positioning ahead of next week’s heavy line-up of developments I’ll delve into in my weekly. Open risk positions into heavy uncertainties might be covered.

US CPI—An Early Fade Worthy Glimpse at War’s Effects

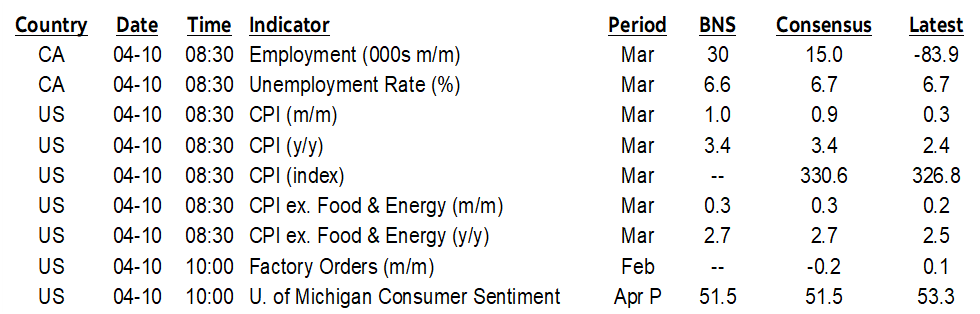

US CPI begins efforts to track the war’s effects (8:30amET). Headline is forecast to pop higher by 1% m/m with core relatively better behaved at this early stage for potential transmission effects. Gasoline’s surge (chart 1) and its 24% m/m NSA rise using last March’s SA factor equates to about a 20% m/m SA increase which at a 2.8% weight in the CPI basket adds about 0.6 ppts to CPI if the weight is steady (it will likely increase). The difference to my 1% m/m headline CPI increase is then made up largely on other energy (fuels) and food.

And it shouldn’t matter. The FOMC knows inflation is going to spike near-term. Markets know that inflation is going to spike near-term. You and I know that inflation is going to spike near-term. The key is persistence and pass through and how the full employment part of the dual mandate also evolves. Nothing will be settled by today’s CPI except for folks who must trade it.

Canadian Jobs—Rebound, with an Asterisk or Several

Canada delivers the March jobs report at the same time as US CPI (8:30amET) which might dirty the domestic waters somewhat. A rebound of some magnitude is generally expected. Consensus sits at +15k with most in the 10–40k range except one extreme outlier who’s playing mere noise over any narrative. The high end has 40k.

As for drivers, there have been nine times when the monthly jobs tally fell by 70k or more and the next month was up five of those times. So far that’s not so compelling. A weak base effect could drive a gain, but there is sampling persistence in the way the Labour Force Survey rotates panels over six months by dropping and replacing one at a time.

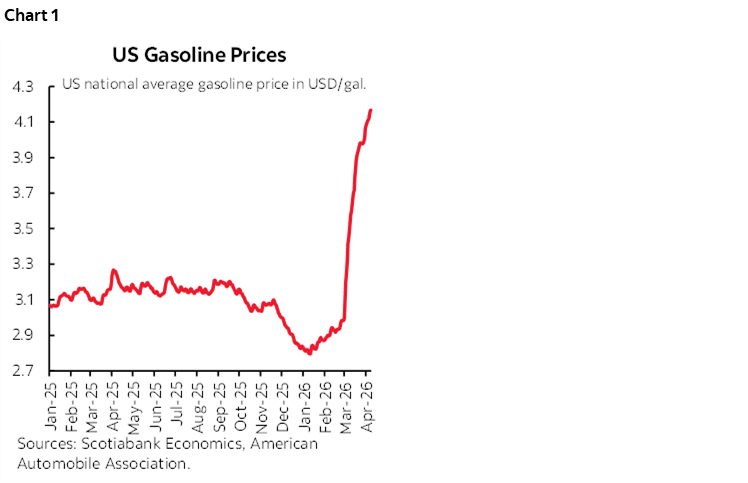

Sickies held back activity in February. Hours lost due to illness were elevated (chart 2). You don’t lose a job if you’re sick but it can prevent getting to interviews and hiring decisions. Ditto for weather that resulted in the third highest tally for lost hours attributable to weather of any February on record (chart 3).

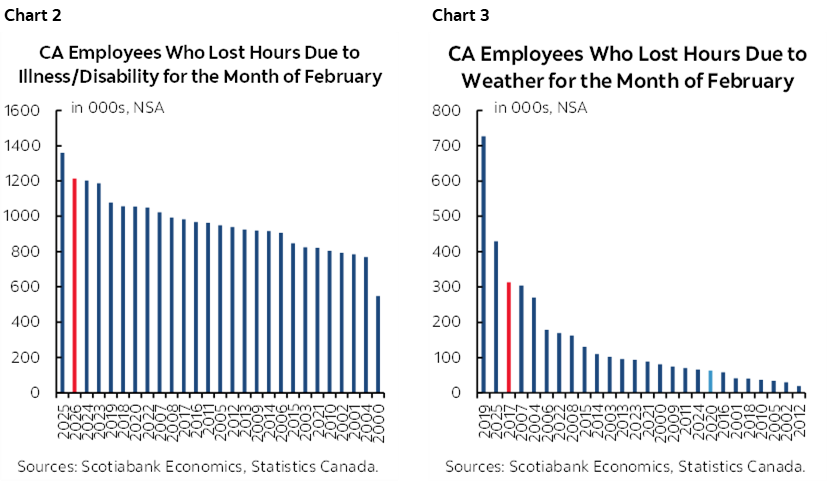

March is usually decent up month in seasonally unadjusted terms and the SA factor is additive (ie: over 1) but less so in recent years. Charts 4 and 5.

Small business hiring intentions point to hiring. So do Indeed job postings.

All that said, the 95% confidence interval on monthly changes in Canadian employment is about +/-57k. For a numbers crowd, that means that a very high degree of survey noise could drive a whole range of possible outcomes. This is Canada’s equivalent to the very noise household survey in the US that serves as a companion to the establishment survey. But good luck!

THE REST!

After the dust settles from US CPI the US will then update the UofM sentiment gauge for April (10amET) and factory orders during February (10amET). UofM is expected to slip and watch both the inflation expectations and expected unemployment readings. Factory orders will be held back by the already known 1.4% drop in durables with just revisions to that plus nondurables to be added.

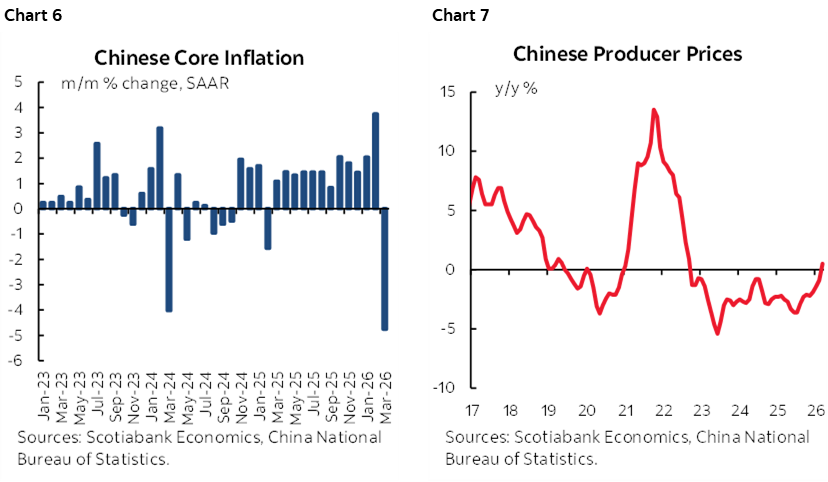

China’s CPI inflation rate ebbed in March to 1% y/y (1.3% prior, 1.1% consensus) as seasonally unadjusted prices fell by -0.7% m/m. Core CPI landed at 1.1% y/y, down from 1.8% previously as seasonally unadjusted prices fell by -0.7% m/m with the annualized decline shown in chart 6. Producer prices increased for the first time in y/y terms since 2022 (chart 7).

The Bank of Korea unanimously held its policy rate unchanged at 2.5% as widely expected. Being a commodity importer, it walked the line between risks to inflation and growth. Governor Rhee said in his final press conference at the end of his term that “the supply shock could be greater” this time than from the Russia-Ukraine war given the impact on oil and Asia’s dependence on imported energy. He went on to say that they will look through the war’s effects for a time but if they persist then there would have to be a policy response. The 2-year yield spiked 37bps higher overnight with markets pricing a hike by late summer.

Peru’s central bank held its reference rate unchanged at 4.25% last evening as widely anticipated. The bias had a dovish tinge to it as the statement said “It is projected that both year-on-year inflation and inflation excluding food and energy will return to the target range toward the end of the year and settle around 2% in 2017, as the effects of supply shocks gradually dissipate.” That may be a bold bet and note that the guidance preceded Peruvians heading to the polls this weekend to elect a new government amid the country’s ongoing political uncertainty.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.