ON DECK FOR TUESDAY, SEPTEMBER 9

KEY POINTS:

- Markets await revisions to US jobs

- Downward annual nonfarm revisions are likely to be large…

- ...but forecasting how large is futile…

- ...while informing nothing about recent momentum

- A fresh BLS assault is underway by the Trump administration

- BCCh will probably hold, but CPI gives cover for a surprise

- Indonesian market turmoil intensified

- Mexico to refresh CPI

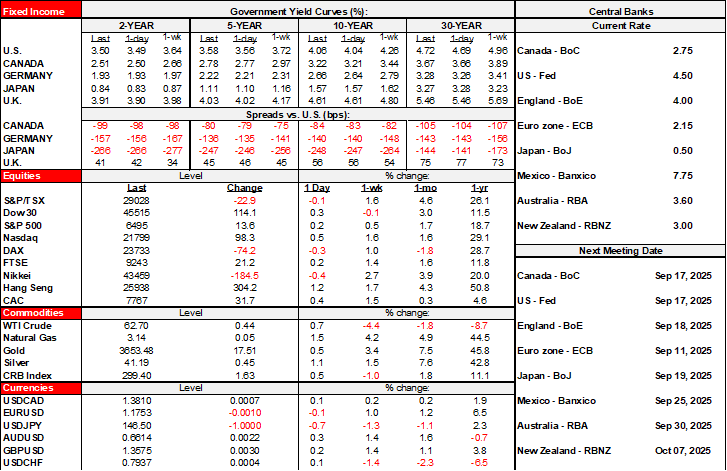

Global markets are mixed to start the day. Sovereign bonds have a slight cheapening bias. Stocks are little changed across a mixture of small gains and losses. The dollar is broadly softer. And gold is up again. BoJ rumours about a willingness to hike this year didn’t appear to be a market catalyst when the headlines hit. Revisions to US payrolls, Chile’s rate decision, Mexican CPI and a test of front-end Treasury demand with the 3s auction at 1pmET will be the main focal points.

THE FUTILITY OF FORECASTING NONFARM REVISIONS

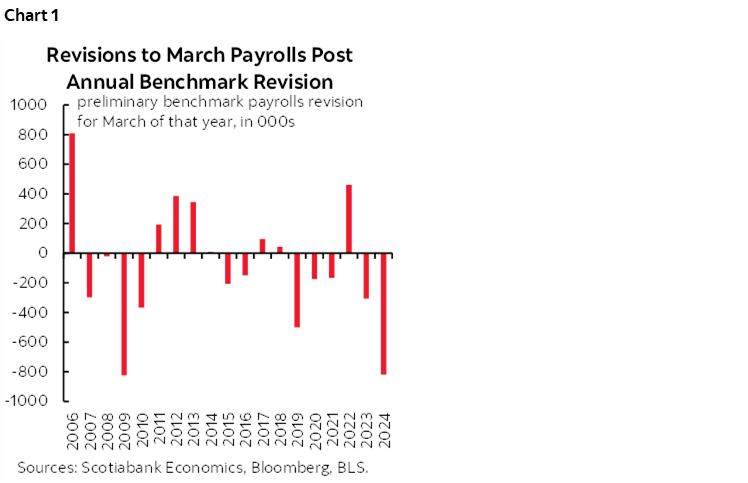

Preliminary revisions to US nonfarm payrolls up to March of this year arrive in tomorrow’s annual benchmarking exercise. They are based on the Quarterly Census of Employment and Wages that captures state and local data from unemployment insurance records. One aim is to restore a link between hard data and payrolls that doesn’t rely on birth-death model adjustments to firm openings and closings. Revisions can be huge (chart 1).

The exercise doesn’t provide revisions from April 2025 onward and so we don’t really learn anything new by way of fresh momentum or direction in the US job market. That’s where the rolling two-month revisions with each payrolls report comes in until we get the annual revisions. This point limits the usefulness of the annual revisions to policymakers relative to Friday’s nonfarm weakness that was driven by my expectation the seasonally unadjusted reading would be low.

All we get are revisions to the period from March 2024 to March 2025. Now, what some shops do is to take the first 3 of the 4 quarters over that period for which we have state level data and then tack on an inference for the final quarter (in this case 2025Q1) in order to get at the full year’s revision to payrolls over that stretch. There are two tenuous assumptions being made here that make everyone’s estimate largely just guesswork.

One is obviously what happened in the QCEWS data in 2025Q1 which is a guess until we see the actual preliminary estimate. Two is that the prior quarters won’t be revised.

Well guess what. I’ve tried to nail estimates of the annual revisions in past years and it’s usually an entirely futile, time-sucking exercise for folks with time to waste. That’s because the prior quarters of data in the QCEWS can themselves be heavily revised.

Ergo, you’re left making a random guess on Q1 and trying to guess at revisions to QCEWS over the prior three quarters.

So, let’s just see the numbers. It’s reasonable to expect large negative revisions based on what we know so far, but don’t waste your time trying to guess at how much. Oh, and if that’s not enough, then the final revisions to these revisions will arrive with the final benchmark estimates early next year!

A BROADER BLS ASSAULT IS UNDERWAY

An arguably much greater concern about US jobs numbers is this exclusive WSJ piece. The US administration is preparing a report that aims to attack the Bureau of Labour Statistics’ data and methodology. That can only mean one thing in my view: lower jobs numbers. Kidding. The Trump administration’s bias is clearly toward rejecting anything that leans against its performance as “fake news.” Incoming BLS head—the unqualified E.J. Antoni—will be under thumb of financial markets concerned about what is happening to potentially politicized data agencies. If he blows it, then maybe there’s a man in Trump’s cabinet waiting to punch his lights out.

CHILE’S CENTRAL BANK TO HOLD

Chile’s central bank is widely expected to stay on hold tomorrow. This morning’s inflation update (4.0% y/y from 4.3% prior, 4.2% consensus) brought inflation right into the top end of the central bank’s 2–4% target range. Core was 3.4%, down from 3.8% and further inside the headline target range. BCCh had cut at its last decision on July 28th and the latest CPI reading might throw fresh uncertainty into the call.

MEXICO CPI

Mexico updates the last CPI reading before Banxico’s next decision on September 25th. Mexico updates inflation on a bi-weekly basis and so there is usually little scope for surprises. A reading of 0.1% m/m NSA is expected with core up 0.2%.

INDONESIAN TURMOIL

The rupiah is among the weakest currencies this morning. The local stock market fell by 1¾% overnight. The catalyst was the firing of Indonesia’s finance minister in the wake of social unrest caused by long simmering inequality concerns. President Subianto’s government planned a 50 million rupiah (about US$3k) monthly housing allowance for lawmakers. Various other high profile controversies have fed rising protests for some time, culminating in a policy pivot by appointing a new finance minister to seek faster growth. Indonesia’s rates curve didn’t like that so much and so most portions of its yield curve rose a touch overnight.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.