ON DECK FOR MONDAY, SEPTEMBER 8

KEY POINTS:

- Risk appetite holding firm as political risk takes center stage

- Japan needs another PM; what else is new

- France’s PM is probably gone by this afternoon

- Japanese GDP revised up on consumption

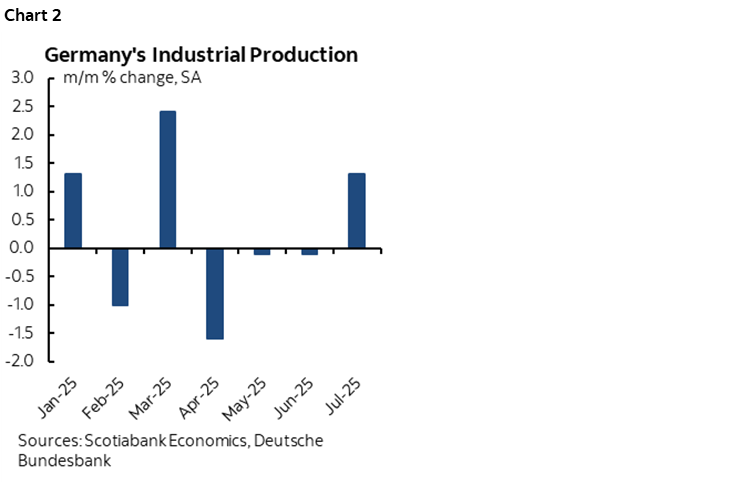

- Germany’s economy was still keeping it together in July

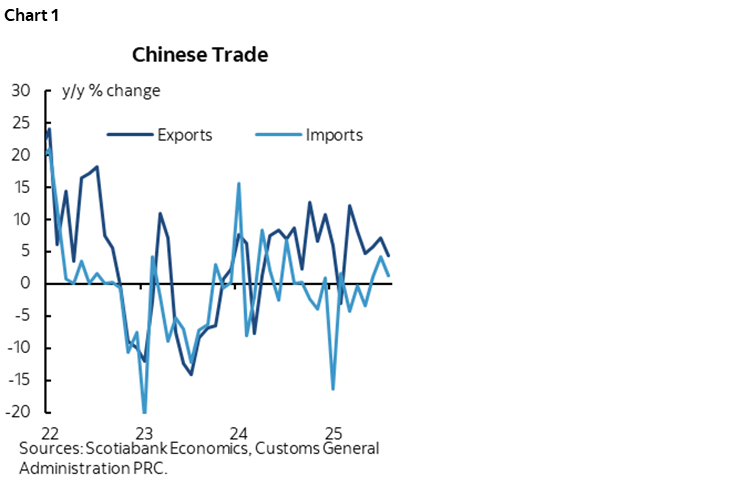

- Chinese export growth softened in August

- Quiet N.A. calendar

- Global Week Ahead—Will Inflation Cooperate (reminder here)

PMs are on the run this morning as politics continues to hang over markets. The yen is starting the week as the weakest cross to the dollar, but the Nikkei rallied by 1½% but also partly as catch up post-nonfarm. Eyes are on France’s confidence vote this afternoon with European equities broadly higher and France spreads over bunds a little tighter. Overnight releases were pluses for Germany and Japan, but not China. There is nothing on tap into the N.A. session. Gold is up another $30/oz to $3,617.

Japan’s Prime Minister Ishiba resigned over the weekend. There have been 39 prime ministers since the end of WWII; just as you memorize the name of one, in comes another. The average tenure is about two years. Ishiba was a weak PM. His LDP party’s ruling coalition was trounced in both lower and upper house elections. Ishiba negotiated a weak trade deal for Japan with the US. Divisions within the LDP didn’t help either.

France’s Prime Minister is likely to be given the boot this afternoon. The results of a confidence vote that he called are expected to be available by 2–3pmET (8–9pm Paris). The issue centers around reforming France’s public finances that are a mess. On the assumption that Francois Bayrou loses his own vote, either a new PM will be appointed by President Macron or Macron will dissolve the lower house and call elections. Macron has refused to resign. A new PM is the more likely scenario, but left hanging will be ongoing uncertainty over France’s fiscal position.

Chinese export growth softened in August. On a month-over-month seasonally unadjusted basis they landed at -0.1% in yuan terms and +0.1% in USD terms, both of which were weaker than a typical month of August except for the pandemic. That dragged the year-over-year growth rates down to 4.8% (8% prior) and 4.4% (7.2% prior) in yuan and USD terms respectively. Chart 1 shows exports and imports in USD.

Japanese Q2 GDP was revised up to 2.2% q/q SAAR from 1.0%. Consumption was revised higher and the inventory drag was revised away while exports were left unchanged but business spending was revised lower.

German exports fell -0.6% m/m SA in July (+0.1% consensus) partly because of upward revisions to June (1.1% m/m from 0.8%). Imports were little changed (-0.1% m/m) after a strong 4.1% m/m prior gain.

By contrast, German industrial output strongly beat expectations in July. It was up 1.3% m/m (1.0% consensus) but was revised up to nearly flat (-0.1%) from a previously estimated plunge of -1.9%. Still, it’s only the first solid month since March (chart 2).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.